I first learned about CAZ Investments due to Tony Robbins’ promotion of the firm in his new book The Holy Grail of Investing. CAZ founder Christopher Zook co-wrote the book and advocates investing in alternative asset classes through CAZ’s offerings.

Curious to learn more, I took a deep dive into the firm’s investment strategies, fee structure, risks, and other considerations that potential investors should be aware of.

11 Things to Know About CAZ Investments

Here are key facts to know about the firm based on my review of the CAZ SEC disclosure brochure, as well as the filings around the CAZ Strategic Opportunities Fund (such as the prospectus):

- CAZ Investments offers investment advisory services to accredited investors and institutions through separately managed accounts and private funds. As of December 2023, they manage over $6 billion in assets.

- Accredited investors can access the CAZ Strategic Opportunities Fund. Qualified purchasers (i.e., those with more than $5 million in investments) can access additional funds and services.

- You can invest in a taxable fund, or purchase through an IRA or 401(k) rollover.

- The CAZ Strategic Opportunities Fund aims to give investors access to various private investments in an all-in-one vehicle that includes 8 to 15 different uncorrelated asset types. It’s also the fund that’s promoted throughout the book.

- The CAZ Strategic Opportunities Fund is a new offering and doesn’t have a performance history.

- The minimum investment required to access CAZ’s Strategic Opportunities Fund is $25,000.

- Fees vary depending on share class, and can change going forward based on how much the fund raises.

- For investments under $99,999, the public offering price involves a 3% upfront sales charge.

- The management fee is flat at 1.25%, with no performance fee. However, other associated fees increase the annual costs from 2.7% to 3.6%, depending on the share class. The more you invest, the lower your expected costs.

- Investors can sell up to 100% of their shares to the fund on a quarterly basis. But the fund limits how much they’ll buy back to just 5% of its total assets each quarter, meaning you could face liquidity issues. Additionally, there’s a 2% fee for selling back shares within the first year.

- The fund will distribute capital gains and investment income at least annually.

About CAZ Investments

CAZ Investments is an SEC-registered investment adviser founded in 2001 by Christopher Zook. The firm has traditionally provided ultra-high-net-worth investors and institutions with access to private market offerings like private equity, credit and real estate, with investment minimums over $250,000.

However, CAZ recently launched a more accessible fund, called the CAZ Strategic Opportunities Fund, which has a much lower minimum investment of just $25,000.

CAZ Performance and Private Market History

Evaluating the historical performance of CAZ Investments is difficult, given their suite of more than 80 private market funds, which are tailored to the needs of ultra-high-net-worth individuals and institutions.

In other words, there’s no clear rate of return since the fund’s inception, such as you’d find with publicly traded mutual funds.

If you’re thinking about investing with CAZ, you can find their quarterly letters on their website. Although they do not mention how individual funds performed against their benchmarks, the letters provide a trove of information pertaining to the firm’s perspective on the current economic situation.

Furthermore, unlike publicly traded funds with readily observable price histories, private investments rely on internal and periodic third-party valuations of the underlying illiquid assets. Since this subjective process occurs infrequently, exact historical returns get recorded with a lag.

CAZ’s website refers to how private equity investment has performed overall as a sector, relying on research by Cambridge Associates (a well-respected market research firm in the space).

For additional context, here’s a relevant quote from a New York Times article titled “Is Private Equity Overrated”:

“As of September 2020, private equity funds had produced a 14.2 percent median annualized return, net of fees, over the previous 10 years, compared with 13.7 percent for the S&P 500, according to an analysis of indexes by the American Investment Council, a lobbying group for the industry, using the latest numbers offered. Public pension funds invested in private equity actually had worse returns than from the S&P 500 — 12.8 percent, net of fees. (These returns, and others quoted in this article, do not include venture capital, which is typically viewed as a separate asset class.)”

Further, a paper published by Ludovic Phalippou of the University of Oxford’s Said Business School found that private equity returns have equaled the returns of public equities since 2006. At the same time, general partners have retained far higher compensation, revealing questionable value relative to liquid index funds when risk-adjusting outcomes.

While we’ll touch on this more below, it’s fair to say that while retail investors can benefit from the increased diversification of private markets, there’s no guarantee private equity investments will outperform a basic equity index fund approach, which is often the benchmark in the space (although private equity typically involves greater investment and liquidity risk).

What Fees Can You Expect to Pay With CAZ Investments?

The CAZ Strategic Opportunities Fund offers multiple share classes based on individual investor eligibility and minimum investment size. Each share class has its own upfront sales charges and ongoing expense ratios, as noted in the table below:

| Share Class | Minimum Investment | Upfront Sales Charge | Average Annual Fees |

| Class A | $25,000 | Up to 3% | 3.6% |

| Class D | $25,000 | None | 3.6% |

| Class F | $100,000 | None | 2.7% |

| Class I | $500,000 | None | 3.0% |

| Class R | $25,000 | None | 3.25% |

Class A shares are accessible to accredited investors with a $25,000 investment. These shares have up to 3% in front-end sales charges, with that amount decreasing incrementally for investments above $100,000. Ongoing fees average around 3.6%, including a 1.25% management fee.

Class D shares also require a $25,000 minimum initial investment but have no upfront sales fees. Total annual operating expenses run approximately 3.6%, consisting of the 1.25% base management fee plus other fund costs.

What’s the difference between Class A shares and Class D shares? Unfortunately, CAZ does not offer much clarity about this.

The prospectus mentions that Class A shares are offered through financial channels such as registered broker-dealers, banks, advisers and other financial institutions, but it does not specify how one might purchase Class D shares (which have no upfront sales charge).

For those able to make at least a $100,000 initial investment, Class F shares provide the next least expensive share class with no sales loads and average annual fees of 2.7%. You can only buy Class F shares through an approved financial intermediary.

Class I shares carry a higher $500,000 minimum investment but have the lowest overall cost structure, averaging 3% annually. These shares can only be purchased by approved institutional investors and individuals with very high net worth.

Finally, Class R shares strike a middle ground thanks to a minimum initial investment of $25,000, average yearly fees of around 3.25%, and no front-end sales charge. However, this class is only available to wealth management firms to represent underlying client investments.

What Assets Does CAZ Invest In?

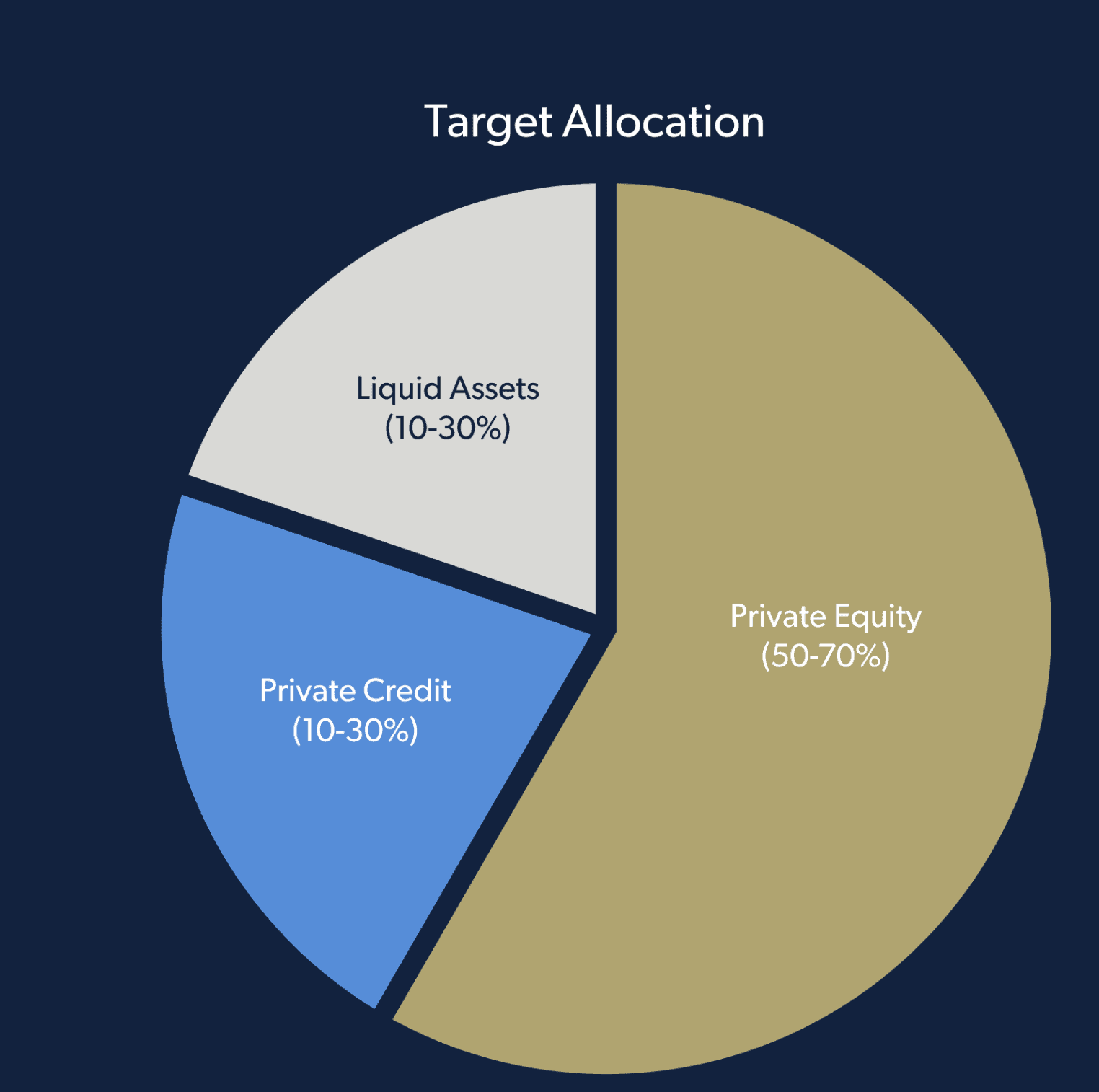

According to the Strategic Opportunities Fund documents, CAZ aims to invest across a diversified range of alternative asset classes and strategies, including:

- Private equity: Buyout, growth capital, and venture capital funds.

- Private credit: Investments in senior secured bank loans and subordinated debt.

- Real assets: Exposure to real estate, infrastructure and natural resources.

- Special situations: Restructuring and turnaround equity positions.

- Co-investments: Private deal flow alongside sponsor funds.

- Secondary funds: Buying existing interests in private investments and funds.

- Primary funds: Investing in newly launched private investment vehicles.

- Liquid investments: Cash, fixed income, ETFs and listed securities.

The fund intends to allocate its capital broadly within 8 to 15 uncorrelated private market asset classes to diversify risk and return drivers.

Here’s a pie chart showing the target allocation:

My First Impressions of CAZ Investments

While I’m a big proponent of low-cost equity index investing (see our guide on how to start investing) and think that should make up a large percentage of your portfolio, it can make sense to diversify beyond that, especially for experienced investors who understand how to evaluate specific opportunities.

The CAZ Strategic Opportunities Fund is new, so there’s not much we know yet.

Their fees are about what I would expect

For comparison’s sake, Fundrise’s Innovation Fund, which also invests in private markets, aims to keep the fund’s annual fees around 3% (although there’s no sales load).

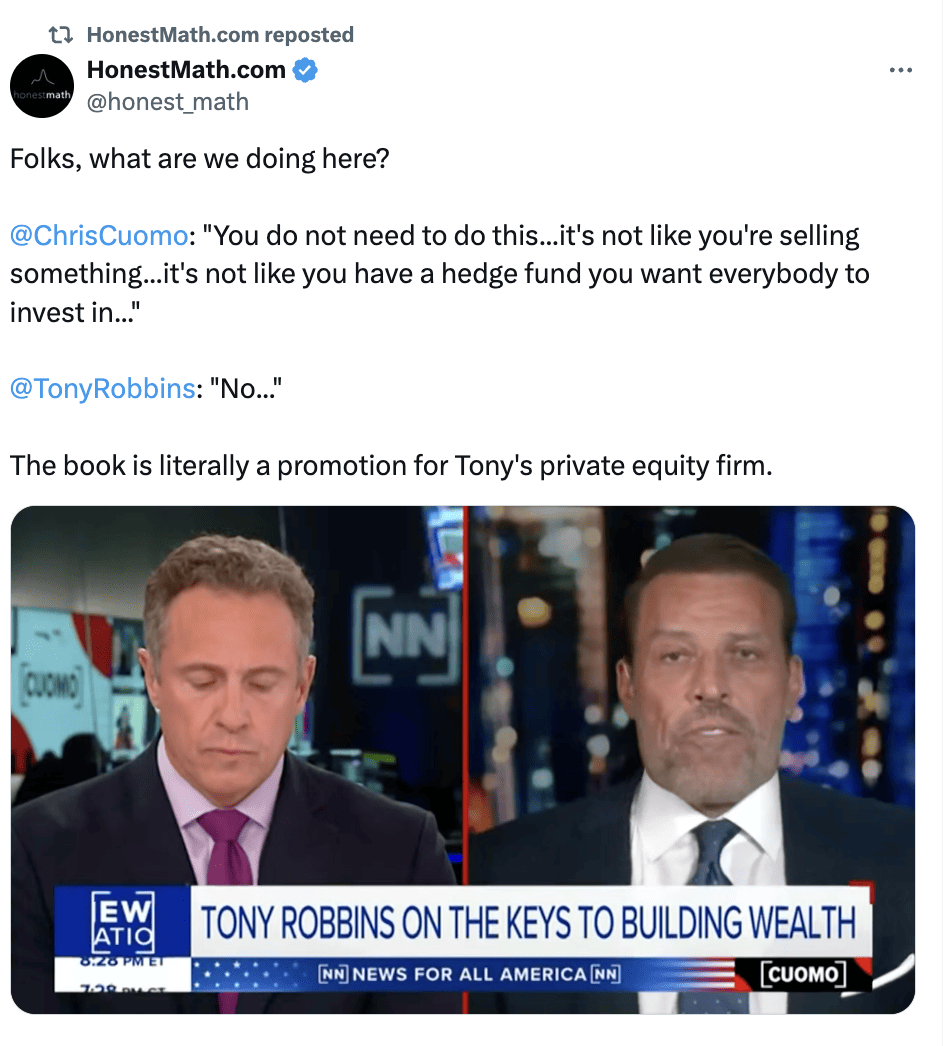

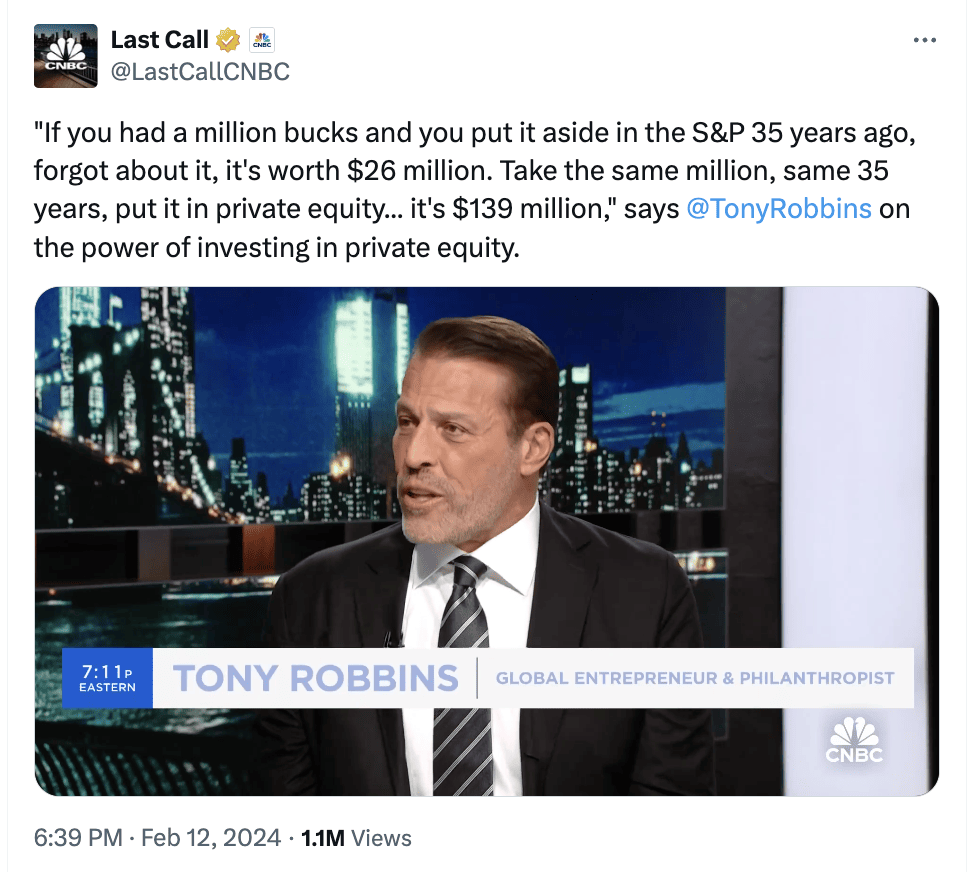

At the same time, Tony Robbins has made a handful of comments about CAZ in media appearances that have stood out to me, and I’m concerned that some people may be looking to invest in this new fund thinking that — as the name of Robbins’ new book suggests — it’s something like the Holy Grail of investing.

No such Holy Grail exists.

The book contains a disclaimer upfront and does not try to hide the fact that there’s a conflict of interest at play:

“Tony Robbins is a minority passive shareholder of CAZ Investments, an SEC-registered investment advisor (RIA). Mr. Robbins does not have an active role in the company. However, as shareholders, Mr. Robbins and Mr. Zook have a financial incentive to promote and direct business to CAZ investments.”

— The Holy Grail of Investing

But you then see things like this:

And this:

Conflicts of interest aside, the issue with the latter statement is that it makes the following assumptions:

- A compounded annual rate of return over 15%, net of fees.

- That the tax efficiency of private equity is similar to that of an S&P 500 index fund (it’s not).

Plus, it doesn’t account for survivorship bias, a term that describes the fact that funds with poor returns often stop reporting their performance and thus drop out of databases, skewing the remaining funds’ returns upward.

By not considering failed investments, the historical performance of surviving private equity funds overstates, to at least some degree, the likely future outcomes. In Cambridge Associates’ documentation, they even mention that survivorship bias impacts their analysis.

Regarding tax efficiency, funds tend to have a lot of turnover. Some of the investments within a fund can also have a short lifecycle. These costs related to switching funds and the asset churning can generate significant capital gains tax for investors that may diminish net after-tax returns compared to simply buying and holding index funds.

On the topic of future performance, while Robbins doesn’t explicitly state that you shouldn’t have exposure to an index fund like the S&P 500, the statement above seems to imply that better historical returns would have been garnered by ditching the public markets and putting all your investments in private equity.

Of course, this is no guarantee about that, and it’s a strategy that carries significant risk.

Although these statements are not specifically related to CAZ Investments, I believe it’s important to mention them in the article to offer a balanced view of private markets.

Private markets can be a valuable addition to a well-diversified portfolio, but they are not a “Holy Grail.” They come with different risks than public markets, and for inventors who understand those risks, private markets can offer meaningful portfolio diversification.

I very much appreciate your thoughts and explainations regarding CAZ investments. Very informative, insightful and unbiased. Good information. Thank you.

Glad you found it helpful!

This is very helpful and balanced context. I did feel that the Grail book was a sales tool, and though I don’t doubt the sincerity and integrity of CAZ, it’s good to have alternative perspectives. Thank you.

Thanks Doug. And, good thoughts as well. Most funds and professionals in the space act with high-integrity. The bigger point is that it’s just really hard to beat the market, especially with high-fees!