The 50/30/20 budget is a financial rule of thumb that separates expenses into three main categories — needs, wants and savings — based on take-home pay.

Like most financial rules of thumb, it’s a solid starting point for many people. But as we’ll discuss in this article, there are some notable downsides to this approach.

Keep reading to find out whether this budgeting method is right for you.

50/30/20 Budget: Three Things To Know

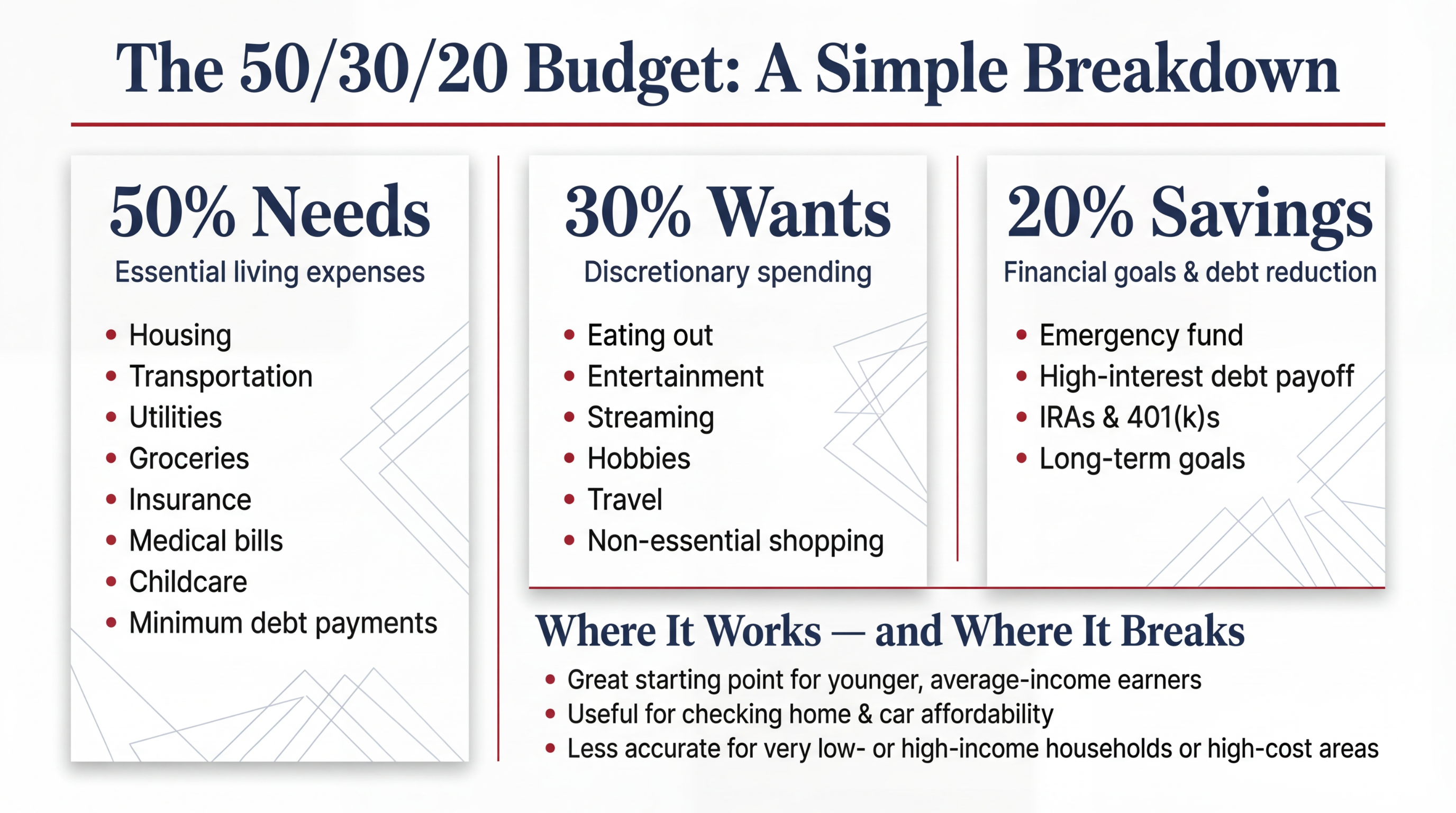

- The 50/30/20 budget divides your after-tax income into three separate categories: 50% for needs, 30% for wants and 20% for savings/financial goals.

- This approach is best for younger, average-income earners who have paid off their high-interest debt. Things get out of whack quickly for both low-income and high-income individuals and families, because your needs neither double when your income doubles nor shrink by 50% when your income declines.

- There’s a lot of value in measuring yourself with the 50/30/20 budget. Even if you choose not to actually use the formula for your budget, it’s a helpful framework for determining whether you can afford larger purchases like a house or a car.

50/30/20 Budget Plan Explained

Here’s a quick breakdown of how a few common expenses are divided up among each of the three categories.

50% Towards Needs

This budget approach states that you should spend 50% of the money you earn on necessary items, such as housing, transportation and other bills.

Here are the most common “needs” that get folded into this category:

- Housing.

- Transportation, including car payments and gas.

- Utilities, like your cell phone, heat, water, gas and trash.

- Groceries (but not eating out in restaurants).

- Insurance premiums, such as life insurance, health insurance and auto insurance.

- Medical bills.

- Childcare.

- Basic clothing.

- Minimum payments on your debt, such as credit cards, student loans, etc.

The items in this category cover the basics of life. They’re the things you need to survive at your current standard of living.

30% Towards Wants

This is what some people think of as the “fun” category. It includes things you want but could certainly live without.

Here are some of the common expenses that get classified as “wants”:

- Date nights.

- Eating out.

- Entertainment (concerts, plays, sporting events, etc.).

- Gym membership.

- Hobbies.

- Premium and streaming TV (like HBO and Netflix).

- Non-essential shopping (new golf clubs, a new Kate Spade purse, etc.).

- Travel.

20% Towards Savings

The next number to think about in this budget formula is 20%. This is the money that goes towards achieving your financial goals, which may include:

- Building an emergency fund.

- Paying off high-interest debt.

- Contributing to IRAs, 401(k)s and other retirement accounts.

You can use the baby steps framework for figuring out which goals you should be focusing on. For example, if you have high-interest debt, you’d want to devote this entire 20% towards getting rid of it.

Benefits Of The 50/30/20 Budget

Here are some of the reasons why this type of budget might make sense.

Benefit #1: It’s a solid starting point.

No matter where your finances are right now, measuring your current expenses against the 50/30/20 budget is a helpful exercise.

When you look at your current income and spending, do you find that one budgeting category is far above or below the recommended guideline?

If so, that could be an area in which you need to focus on changing your habits — whether that means saving more money or cutting back on your spending.

Benefit #2: It keeps your home and transportation expenses in check.

Another good use of the 50/30/20 budget is to help determine whether you can really afford big purchases such as a home or a car.

As I’ve noted frequently on this website, lender guidelines — such as how much house you can “afford” — are designed to maximize the lender’s profit. They’re not based on your financial best interests, and therefore they shouldn’t be used to calculate whether you can actually afford something.

A much better way to determine whether you can afford a house or a car is to insert the payment and other associated costs into a hypothetical 50/30/20 budget.

If the final number comes in way above the guidelines, it’s likely to put a significant strain on your finances.

See Also: How much house can I afford?

Benefit #3: It lets you treat yourself.

Sometimes it can be hard to give yourself permission to buy something nice, even when you can afford it.

What many people like about the 50/30/20 budget is that, as long as your needs and savings remain in check, you can go out and spend the remaining 30% of your income however you want.

Problems With The 50/30/20 Budget

Here are a few of the potential issues you should be aware of.

Problem #1: It uses percentages of income.

Rules of thumb are designed for the “average” person — someone who earns an average income (in the U.S., average household income is around $60,000), who lives in an average cost of living area, and who has average expenditures.

But once you start getting away from averages — whether that’s in income, expenses or geography (more on this below) — the 50/30/20 rule makes less and less sense.

For example, let’s say you’re a dual-income household earning $120,000. You have no kids, live in an urban area, don’t own a car, and have a fully-paid company health insurance plan.

And before you start a family, you want to do a lot of traveling.

In a case like that, there would be nothing wrong with the following breakdown:

- 30% to needs.

- 50% to wants (mostly travel).

- 20% to savings.

On the other side of the coin, if you look at the U.S. Bureau of Labor Statistics’ Consumer Expenditures Report, you’ll find that the bottom quarter of income earners in the United States spend 100% or more of their income on needs.

These are some of the problems you start running into when using percentages. Unfortunately, using fixed dollar amounts (e.g., “spend $2,000 on needs”) doesn’t make things any easier.

So the key takeaway here is that you need to think through your own individual situation to understand when and if a rule makes sense.

Problem #2: It doesn’t account for geography.

Every few years, the U.S. Bureau of Economic Analysis releases its state-by-state regional price parities report, which evaluates how expensive it is to live in one state compared to another, based on the prices of goods and services.

In the most recent report, California has a price parity of 115%. That means, overall, it costs about 15% more to live in that state than the national average. Conversely, Arkansas had the lowest price parity at 85.3% — meaning it costs about 15% less to live in Arkansas than the national average.

While these cost of living figures are not all that surprising, they can’t be ignored. Or better said, it’s important to take them into account.

Unfortunately, most people “account” for them by eliminating the savings aspect of the budget.

In some cases, the cost of living in a relatively expensive area is mitigated by higher earnings. But that’s not always true. When it’s not, achieving certain financial goals will be more difficult — and you may need to make tradeoffs within your budget.

Problem #3: It doesn’t focus on your highest-leverage goals.

Saving 20% of your income over the course of your life is certainly a lot better than the alternative. But life can change pretty fast, which means your financial goals can as well.

Are you close to retirement? Instead of saving 20% of your income, it’s at this stage where you’ll want to understand the exact amounts you need to save (rather than assuming 20% will get you there).

Want to pay off your high-interest debt? For a short while, it’s probably best to commit as much of your income as possible towards that goal, not limiting it to 20% of your income.

The point is this: your goals change often, depending on a variety of factors. Therefore, your percentages will also change — which calls into question their value in the first place.

50/30/20 Budget vs. 70/20/10 Budget

The 70/20/10 budget is a similar method for managing your money, but it gives you a bit more flexibility regarding how you spend on your needs and wants. In this budget, you allocate 70% of your income to cover all your living expenses, including both needs and wants.

This is helpful for those in high-cost-of-living areas who find it difficult to keep their needs within the 50% limit.

The next 20% goes toward long-term savings and paying off high-interest debt. The remaining 10% is dedicated to paying off non-credit card debt, such as car or student loans, or charitable giving.

The 70/20/10 budget’s flexibility is great for those struggling to cover their needs with just half of their income. It also does a good job of balancing long-term investing and debt payoff. That’s because once your high-interest credit card is paid off, you can save 20% for the future and use 10% to pay off lower-interest debts.

While you get more flexibility with the 70/20/10 budget, there is a benefit to having the structure offered by the 50/30/20 budget. With a strict 50% limit on needs, this budget provides clear benchmarks that are very useful when you’re doing things like budgeting for an apartment, saving for a car, or choosing how much house you can afford.

Final Thoughts On The 50/30/20 Budget

It’s important to make personal finance personal, in the sense that you set your own priorities and goals. For this reason, general guidelines like the 50/30/20 budget need to be treated with caution.

Yes, they can be helpful. But if they don’t align with your financial goals — the goals that are going to move your life forward in a meaningful way — they don’t have much value to you.

So go ahead and use the 50/30/20 rule and other financial rules of thumb as good frameworks to base financial decisions on. Just avoid thinking of them as hard-and-fast rules. Instead, think about what’s important to you and how the money you make can help you achieve that.

Do you have suggestions for people who make under $60,000/year?

We roughly try to stick to this, but we’ve been doing our grocery shopping out of the “30” part of the budget and are always out of that money before the next paycheck (but the “50” part is never empty).

I’m nervous to take food out of that, but maybe I should just sit down and average out my bills and how much we put in there per month (it changes because of being hourly) and see if we could realistically get our groceries or at least the first $X of them from this.

Hi Hardy.

Thanks for the comment. It’s a great question and one that many people have.

Your question gets to the core of “Problem #1: Uses Percentages Of Income.”

There’s no question that you’ve got your act together in terms of where your money is going. However, with an income 33% less than the average household income, I’d stay away from using the 50/30/20 budget as a way to manage your expenses.

Instead, I’d go with something that offers more control and flexibility.

If you like apps, check out YNAB (it costs a few dollars per month).

The envelope system works, it’s just a bit of work: https://www.thewaystowealth.com/dave-ramsey-envelope-system/

Another alternative is zero-based budgeting: https://www.thewaystowealth.com/dave-ramsey-allocated-spending-plan/

P.S. — Congrats on #4!