Pros

- No hard credit check.

- No income requirements.

- Reports to all three major credit bureaus.

Cons

- Prices are higher than similar products offered by local credit unions.

- Does not allow you to transition to no-fee products once your credit score improves.

Note: While Credit Strong serves businesses, this review is focused on their products for individuals.

How Credit Strong Works

To understand how Credit Strong works, it's important to understand the factors that impact your credit score and the difference between revolving and installment credit.

First, the factors that impact your credit score are:

- Payment history (35%). Your record of making on-time payments.

- Credit utilization (30%). The amount of credit used compared to your credit limit.

- Credit history (15%). The longer you've been using credit responsibly, the better your score will be.

- Credit mix (10%). The mix of different types of credit you have. Ideally, it's best to have a variety of credit types on your account.

- Credit inquiries (10%). New credit inquiries can temporarily lower your credit score.

Regarding the credit mix factor, understand that there are two general types of credit: revolving credit and installment credit.

Revolving credit is credit that can be used repeatedly, up to a certain limit. The credit limit is determined by the credit issuer, based on factors like credit score and income. Credit cards are the most common type of revolving credit.

Installment credit is credit that must be repaid in fixed payments over a set period of time. Two common examples of installment credit are mortgages and auto loans.

With this information, you can evaluate different strategies to improve your score, depending on your particular situation.

For example:

- If your credit utilization is on the high side, one of the quickest ways to increase your score is to increase the amount of revolving credit available.

- If you only have installment credit on your credit profile — e.g., a car payment but no credit cards — you may be able to increase your credit score by taking out a revolving credit line.

Tip: If you want to see how various strategies may impact your credit score — such as adding $500 in revolving credit — we recommend Credit Karma, which allows you to track your credit score for free, see credit report cards for each credit bureau, and get personalized recommendations for increasing your score. (Learn more in our Credit Karma review.)

With that in mind, here’s an overview of Credit Strong’s three products.

| Product | Revolv | Instal | Magnum |

| What it is: | A revolving credit account that builds up to $3,000 of credit history, reported to the three major credit bureaus. | An installment account that builds up to $1,100 of credit history, reported to the three major credit bureaus. | A $2,000 to $30,000 installment account that builds credit history, reported to the three major credit bureaus. |

Revolv

| Product: | Revolv. |

| Credit limit reported: | $500 to $1,000 (base plan), up to $3,000 (with savings). |

| Fees: | $99 per year. |

| Type of credit: | Revolving line. |

| Best for: | Those with no credit history, or those who can benefit from adding a revolving line credit mix to their credit history. |

With the Revolv product, Credit Strong essentially opens a secured credit card under your name. But you don't have access to this card; while your credit limit starts at $500, you cannot spend against this amount.

The product comes in two options:

Revolv (without savings)

- Just pay the $99 annual fee.

- Get a $500 revolving credit line that can grow to $1,000.

- No monthly payments required.

- Reports to all three major credit bureaus.

Revolv + Savings

- Same $99 annual fee, plus optional monthly savings deposits.

- Start with a $500 credit line.

- Make monthly savings "commitments" (you choose the amount).

- Each three consecutive on-time payments increases your credit limit by $100.

- Can build up to $3,000 in revolving credit through regular payments.

- 100% of your savings are returned when you close the account (no interest is earned).

- Helps establish payment history while building savings.

- Reports monthly payments to credit bureaus.

My take: While this might be worth it if you need quick credit improvement for a specific goal, like an apartment approval, traditional secured credit cards typically offer the same credit-building benefits with no annual fee plus actual spending capability. Plus, there is the option to upgrade to an unsecured card later on. The savings feature is essentially an expensive version of credit-builder loans that many credit unions offer at much lower costs.

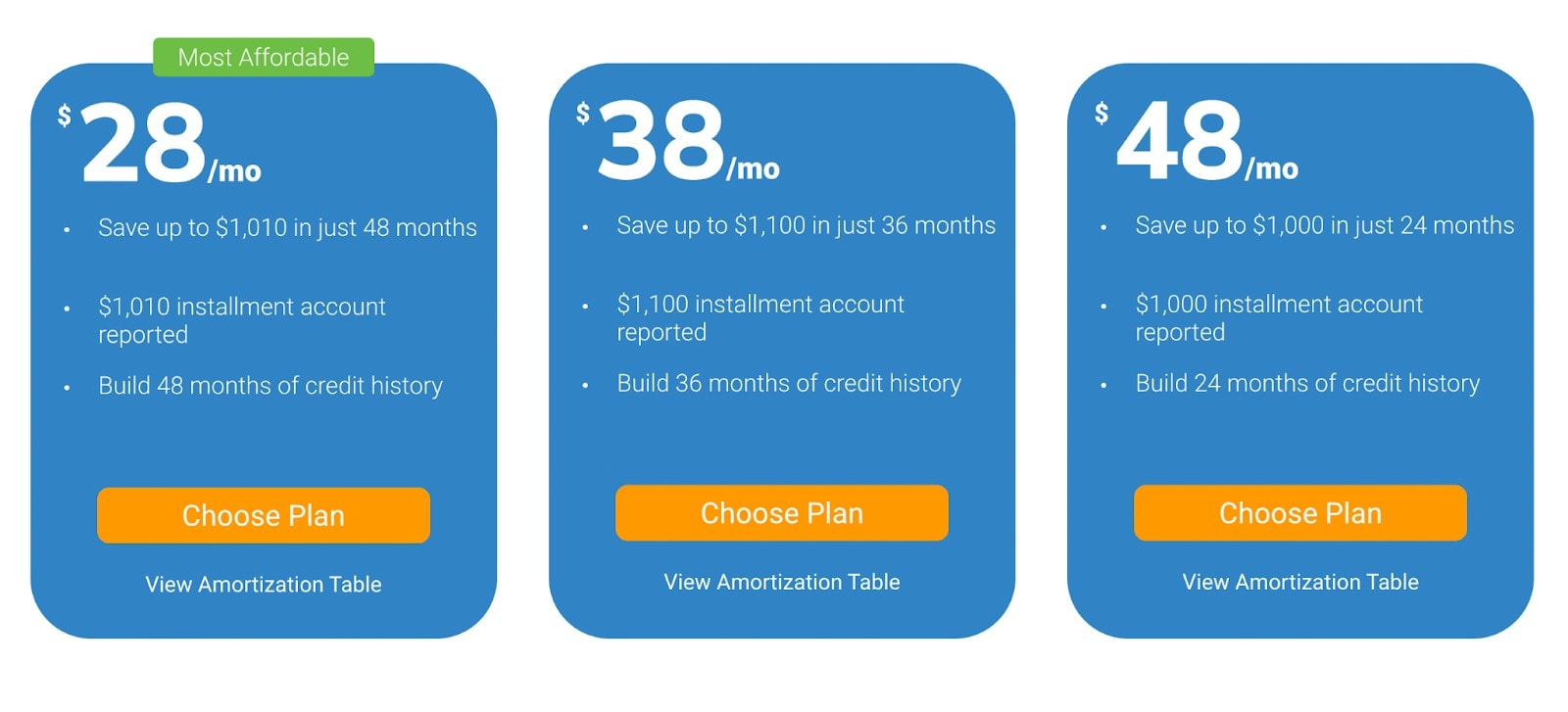

Instal

| Product: | Instal. |

| Credit limit reported: | $1,000 to $1,100. |

| Fees: | $28 to $48 per month. |

| Type of credit: | Installment line. |

| Best for: | Those who would benefit from adding an installment loan to their credit mix. |

Instal reports $1,000 to $1,100 of installment credit to your credit profile. Their cheapest plan reports a $1,010 installment line to all three credit reporting agencies for up to 48 months. Their most expensive plan, at $48 per month, reports a $1,000 installment line to all three credit reporting agencies for up to 24 months.

What's happening here is that Credit Strong is loaning you money deposited into a savings account you don't have access to. You then make monthly payments, which include interest, back to Credit Strong.

You are not required to pay the entire balance in full. You can cancel at any time, and you'll receive the amount accrued in your savings account back.

Remember that when you pay $28, $38 or $48 per month to Credit Strong, some of that goes towards paying off the interest on the loan. So, if you're making $28 monthly payments, much of that money is going towards interest and not accruing in a savings account.

So how much is this actually costing you? Let's look at the $28 per month, 48-month term plan. Here's how it breaks down:

- After 12 months, you’ll have paid $336 total. Of this, $199.83 will be returned to you as savings.

- After 24 months, you’ll have paid $672 total, with $435.33 in savings available.

- After 36 months, you’ll have paid $1,008 total, and $713.87 of this will be your savings.

- After 48 months (end of term), you’ll have paid $1,344 total, with $1,010 returned as your savings.

With the shorter-term but more expensive plans (e.g., $48 per month for 24 months), a larger proportion of your payments goes toward your savings, and less goes toward interest. This is because you're paying off the loan faster, so there’s less time for interest to accumulate. However, the tradeoff is that your monthly payment is higher, which may impact your budget.

Your payments are reported to all three major credit bureaus during the repayment period. This allows you to positively impact your payment history and utilization, and if you don't have an installment line on your credit report, it will improve your credit mix.

My take: A Credit Strong plan may be helpful for those with no credit history or very poor credit and limited options. However, if improving your credit score quickly is the goal, more effective strategies include lowering your credit utilization and becoming an authorized user on a trusted account. These methods typically yield faster results and minimize costs. If those options are exhausted, and the potential savings from a higher credit score outweigh the interest costs of the plan, it can make sense — but it’s important to understand precisely what you’ll pay in fees and interest.

CS Max and MAGNUM

CS Max and MAGNUM are Credit Strong’s premium credit builder products, designed for individuals who want to build large installment credit limits quickly.

These plans focus on maximizing the credit limits reported to credit bureaus, making them suitable for those with cash on hand but limited or poor credit history.

While CS Max has a maximum installment credit of $10,000, MAGNUM takes it a step further, offering up to $30,000 of installment credit with longer repayment terms of up to 10 years.

Here are the different types of plans:

CS Max

- $49 per month for $2,500 installment credit (60 months).

- $99 per month for $5,000 installment credit (60 months).

- $199 per month for $10,000 installment credit (60 months).

MAGNUM

- $30 per month for $2,000 installment credit (up to 120 months).

- $60 per month for $5,000 installment credit (up to 120 months).

- $125 per month for $10,000 installment credit (up to 120 months).

MAGNUM XL

- $175 per month for $15,000 installment credit (up to 120 months).

Someone who could afford these monthly payments comfortably would rarely need such a high credit limit so quickly. However, some situations that can come up where Magnum might help are:

- A successful business owner with little to no credit history is looking to establish high credit limits quickly to improve their credit score before applying for a business loan.

- A person with a high income is applying for a large loan in the next few months and could benefit from a temporary boost.

Remember that these credit builder loans impact your debt-to-income ratio. Lenders — especially mortgage lenders — have standards to limit the amount of your monthly income that goes towards debt.

The classic example is the 28/36 rule, which dictates that no more than 28% of your monthly gross income should go towards housing expenses (principal, interest, taxes, and insurance), and no more than 36% of your monthly gross income should go towards your debt.

So, with a product like CS Max or Magnum, your income must be high enough to comfortably absorb the monthly payment.

My take: The only strong case for using CS Max or MAGNUM is if you have a high income, need a quick credit profile boost to secure a large loan (such as a mortgage or business loan), and the high monthly payments won’t negatively impact your debt-to-income ratio.

Credit Strong Alternatives

If I had no credit history or a poor credit score, one of my first steps would be to see if I could get added as an authorized user on the credit accounts of family members. This is usually free, and it can have similar positive impacts to your score. Of course, whoever adds you as an authorized user must have a good credit score and history themselves.

Another option, which I tend to prefer over credit builder loans, is a secured credit card.

A secured credit card is backed by a deposit you make with the issuer. Many products on the market have no monthly fees and pay cash-back.

What I like most about secured credit cards, however, is that card issuers usually allow you to transition into a standard credit card after you establish a history of on-time payments. This allows you to keep your credit history intact once you're ready to move on from the secured product.

This way, you’re not stuck for years paying an unnecessary monthly fee just to keep the oldest credit line you have on your report active.

Out of all the cards on the market right now, I like the Capital One Quicksilver Secured Cash Rewards Credit Card, which gets you 1.5% cash-back.

When it comes to evaluating different credit builder products, options that may be of interest include:

- Cred.ai. A deposit account linked to a credit card (Unicorn Card) that reports to credit bureaus.. How much you can spend is based on what’s in your savings account. Cred.ai’s best trait is that it has a no-fee option, which makes it a solid choice for someone with no credit history who is not in a rush to increase their credit score. Read our cred.ai review to learn more.

- Extra Debit Card. A credit-building debit card that costs $149/year for basic credit building or $199/year with rewards ($12.42 or $16.58 monthly). It monitors your bank balance to prevent overspending and reports your activity to credit bureaus. The reported credit limit reflects your bank account balance, making it ideal for those with steady income looking to build credit safely.. Read our Extra Debit Card review to learn more.

- Self. A credit-building service offering secured loans and a secured credit card. No hard credit check is required. Monthly payments range from $25 to $150 with 24-month terms and 15.51-15.92% APRs. Designed for those with poor to fair credit looking to establish payment history. Read our Self Review to learn more.

Finally, understand that these strategies are not mutually exclusive. In fact, being added as an authorized user on an account with a high credit score, taking out a secured card, and then taking out an installment loan with Credit Strong, can all be done together to improve your score.

Credit Strong FAQ

There's no early termination fee for closing an account. Funds that went towards the saving aspect of your monthly payment are returned.

No, you can't make payments with a credit card. You can have payments deducted automatically from a checking account or use a debit card. Payments made via a debit card will incur a convenience fee from Credit Strong.

Opening a new line of credit, whether installment or revolving, can temporarily lower the average age of credit lines on your account. As a general rule, this impact fades after six months. Remember, during this time, you're also benefiting from the positive impact that Credit Strong provides. Overall, these factors should outweigh the temporary and small decrease, though every situation is different.

Yes. Credit Strong is a division of Austin Capital Bank, a member of the FDIC.

My Credit Strong Analysis

Credit Strong works best as a short-term solution. Your long-term goal should be to build a solid credit history where you no longer need these products. After all, the longer you rely on credit builder products to maintain a healthy score, the more you’ll pay. But beyond that, relying on these products comes with risks.

For example, part of your credit score is the age of your accounts, and another part is your credit utilization ratio. When you close your account, you lose what may be your oldest account and also suffer from a reduction in available credit — both things that can hurt your credit score.

If you haven’t built sufficient credit outside of these products, you may find yourself right back where you started: looking for credit builder products to help improve your credit score.

The best scenario is to use a service like Credit Strong for three to six months, benefit from a temporary credit score increase, and then — near the end of that period — apply for a more traditional line of credit, such as a no-annual-fee credit card from a major bank.

If you feel like you fit in this camp, then Credit Strong does have a lot to offer.