At a Glance

- Money management starts with knowing what you want. Set clear goals and build a plan around the life you want, not just the bills you have.

- The core of personal finance is growing the gap between what you earn and what you spend. Nothing works unless you spend less than you make, and building that gap gives you the room to save, invest, and make progress.

- Systems beat willpower. Automate savings, debt payments, and investing so your goals happen on autopilot—research shows this is the most reliable way to get results.

How does someone go from feeling stressed about money management to feeling confident and capable?

Studies show that people with a financial plan are twice as likely to report no anxiety or depression regardless of income.

Money management works best when you follow a process, and the process starts with knowing what you want your money to do for you. Once you are clear on your goals, every other step becomes easier to put in place.

In this guide, I will walk you through the four steps of money management so you have a clear plan regardless of where you are today.

The Basics of Money Management

To become good at managing your money, there are four different steps you’ll need to go through.

- Define Your Values and Set Your Financial Goals

- Understand Your Starting Point

- Plan and Automate Your Cash Flow

- Track Your Progress and Adjust

Step 1: Define Your Values and Set Your Financial Goals

Money management works best when your goals reflect what matters most to you. Step 1 brings these ideas together by having you define your values first and then turn those values into clear financial goals.

Part 1: Define Your Values

Your values act as the foundation for every decision you make with money.

Values are the two to three core ideas that guide your decisions. They help you understand what matters most so your goals have meaning and direction.

Values will differ from person to person, but most fall into one of these categories:

- Security. Wanting a stable and predictable financial future.

- Accumulation. Focusing on growing your net worth over time.

- Freedom. Prioritizing the ability to make life choices without financial pressure.

- Generosity. Wanting to give back and support others.

- Enjoyment. Choosing to spend on experiences and items that bring joy.

- Family. Ensuring the well-being and stability of loved ones.

My favorite question to ask people when they are working on value setting is this:

“When I look back on my life many years from now, which values will I regret not prioritizing?”

Use that question to identify the values that feel most important to you, and write them down. The categories above can help you get started, but feel free to define your values in your own words. They belong to you.

Part 2: Set Your Financial Goals

Once you have defined your values, the next step is to outline the big goals you want your money to support.

You do not need to worry about exact numbers yet. That will come later when you understand your income, expenses and cash flow.

For now, focus on the bigger picture.

Here are three questions that can help you get started:

- If you woke up tomorrow with no money stress, what would be different?

- What do you want to be able to do, have, or experience in the future?

- Which goals feel most connected to your values?

Write down the goals that come to mind, even if they feel big or far away. You will refine and prioritize them later once you understand your full financial picture.

If you want more support with this part of the process, I have two helpful guides you can use: one on creating a financial plan that includes a one-page template, and another that walks you through how to set clear financial goals.

Step 2: Understand Your Financial Starting Point

You have set your values and goals, and now it is time to assess where you are today.

Think of this step like getting your blood work done at an annual checkup. The goal is not to judge the numbers but to understand what is going on so you know what to work on moving forward.

There are two parts to this step.

Part 1: Calculate Your Net Worth

First, you need a clear snapshot of your overall financial picture. This gives you a starting benchmark you can measure against in the future.

Your net worth is the simplest way to do this. It is your total assets minus your liabilities.

Net worth gives you a clear, black and white picture of how you are doing. Over time, you can quickly see whether that number is moving up or down and whether you are making progress toward your goals.

Resource: Free Net Worth Spreadsheet Template.

Part 2: Measure Your Cash Flow

Second, you need a good handle on your income and expenses. If you want to put money toward your goals, you need money left over each month, and the only way to know that is to understand your cash flow.

Start by looking at what you earn and spend today.

This gives you a sense of your past patterns. Then get clear on what your fixed expenses are going forward, such as rent, insurance, transportation and essential food costs, and what is truly discretionary.

This matters because if your fixed expenses take up most of your income, it becomes very difficult to save or pay off debt.

Once you know how much of your spending is flexible, you can decide where to make changes and how much you can realistically put toward your goals each month.

You have a few options for tracking your income and expenses.

Budgeting apps can sync your accounts and make it easy to review and categorize your spending, and I cover the top choices in my guide to the best budgeting apps.

If you prefer something simple and do not want to link accounts, a free budgeting template is a good alternative and keeps the process lightweight.

Step 3: Plan and Automate Your Cash Flow

In our post on creating a financial plan, we discussed how cash flow planning is the most important aspect of financial planning.

Most people equate financial planning with managing an investment portfolio. But it’s far more important for most households to focus on cash flow planning — i.e., on deciding what to do with your income.

The Ways To Wealth

At its core, cash flow planning is about answering one question:

How much of your monthly income can you put toward your goals?

For example, if your take-home pay is $10,000 and your average expenses are $8,000, you have $2,000 left to allocate. Your job in this step is to decide where that money goes first and then build systems to make it happen automatically.

Part 1: Choose What to Focus on First

This is where many people get stuck. They have a vision for the future but do not know which steps come first or how to build momentum.

A helpful way to think about priorities is to follow a simple framework.

Dave Ramsey’s Baby Steps are a popular example. I do not agree with every detail, but the structure is useful because it teaches the idea of building a foundation before you try to build wealth.

In simple terms, most people will make progress faster when they follow this general order:

- Save a small emergency fund

- Pay off high-interest debt

- Build a larger emergency fund

- Begin investing and working toward long-term goals

This framework keeps you focused on one thing at a time.

It also prevents you from skipping ahead too early.

For example, someone whose long-term value is wealth accumulation might be tempted to open a brokerage account before they have savings or a safety net. That sounds productive but usually backfires. You need a stable foundation before you can grow.

Use your values to guide your vision, and use this type of priority list to decide what to work on next. Pick a small number of goals, stay focused, and let the foundation support everything that comes after it.

Part 2: Pay Your Goals First

Let’s say your goal is to start saving more money for retirement.

The two options you’re considering are:

- Have your employer automatically deduct money from your paycheck.

- Wait until the end of the month to see how much extra money you have left over and then invest that.

If I was to place a bet on which of these strategies would lead to more money saved over time, I would go with the first option every time.

Money without a purpose tends to get spent. On the other hand, when we allocate money to our most important financial goals up-front, the small stuff always seems to work itself out.

In practice, this idea is referred to as reverse budgeting.

Specifically, that means that instead of waiting until the end of the month to fund your financial goals, you pay these goals first.

And for even better results, you’ll want to automate the process.

What this automation looks like depends on what you’re trying to do. However, here are some best practices based on common financial goals.

- Building an emergency fund: Schedule an automatic transfer from your checking account to a savings account for the day after your paycheck hits the bank. For best results, keep your savings account at a different bank than your checking account, so that it’s harder to withdraw the money.

- Paying off debt: Create a debt snowball. For the debt with the smallest balance (not the one with the highest interest rate), set up an automatic payment that’s higher than the minimum.

- Achieving short-term saving goals (car, house, wedding, etc.): As with your emergency fund, set up a recurring transfer from your checking account to your savings account. If your bank allows you to have sub-savings accounts, you can even go as far as naming your accounts after your goals.

- Investing. Utilize a 401(K) or other employer-sponsored plan to make automatic contributions. For IRA contributions, set up a recurring transfer that goes from your checking account to your investment brokerage soon after each paycheck hits.

Part 3: Automate Everything Else

The vast majority of monthly bills, including credit card, cable, internet, cell phone, utilities and other subscriptions, should ideally be set to auto-pay.

This is a big time saver. But even more importantly, it helps you avoid late payments. And since one of the most influential factors in your credit score is on-time payments, this habit can boost your credit score significantly over time.

At the same time, this can be tricky for those living paycheck-to-paycheck. If that’s the case, here are a few tips:

- Use auto-pay to make only the minimum monthly payment. This can help you at least avoid late fees for missing payments. Ideally, you can then go in and make a bigger payment on your own.

- Sign up for a bank account that doesn’t nickel and dime you for overdraft fees. If you’re with a bank that has numerous fees, consider switching. One of my favorites, Chime, allows account holders to overdraft up to $100 without a penalty.

- Utilize notifications. Use text or email notifications to stay on top of when bills are due throughout the month, as well as when your bank account balance gets low.

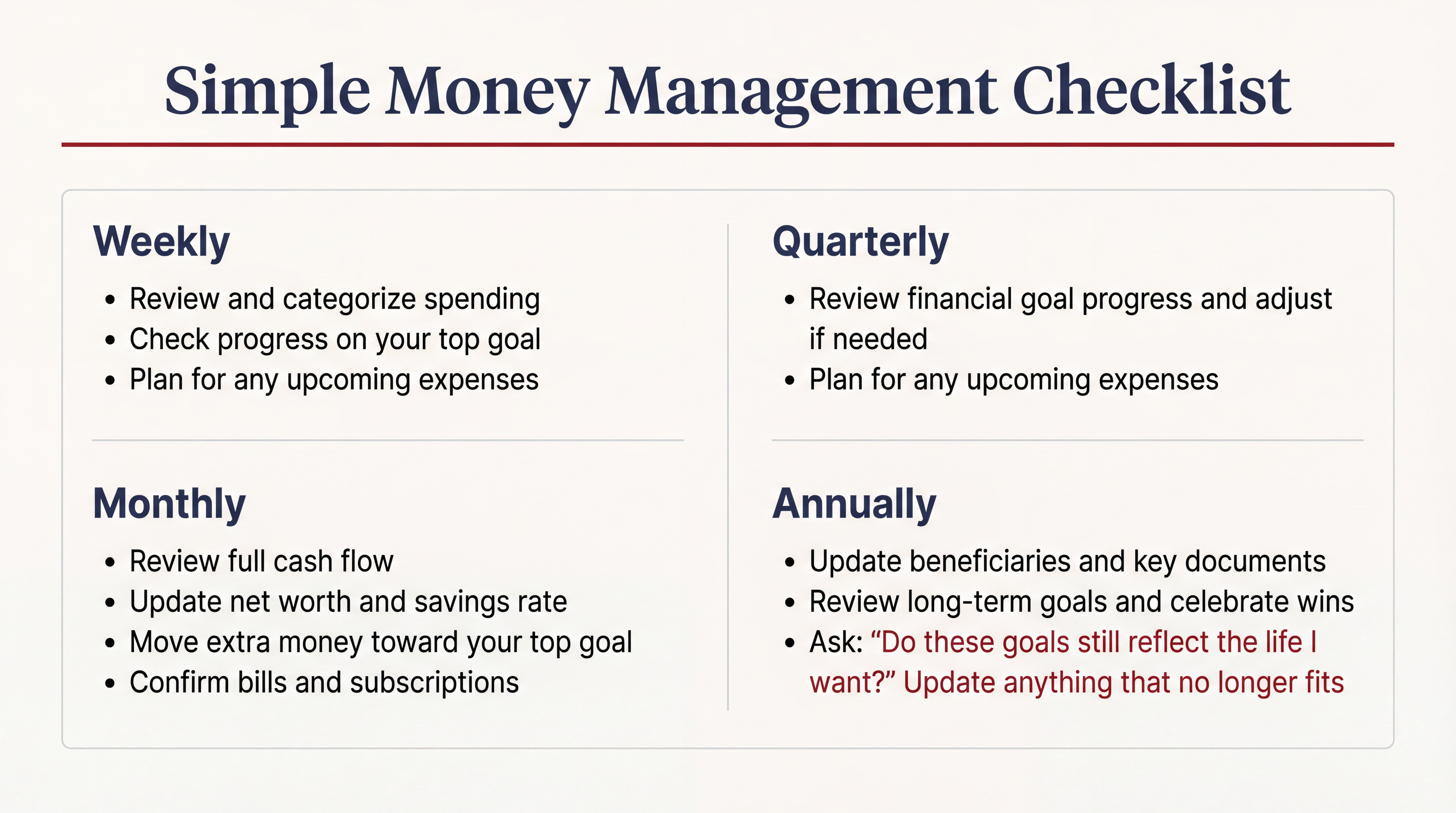

Step 4: Track What’s Important and Adjust If Necessary

Money management is not something you set up once and forget about. The goal here is to build simple systems that help you stay on course over time.

Pearson’s Law highlights why this matters

“When performance is measured, performance improves. When performance is measured and reported, the rate of improvement accelerates.”

A helpful way to think about this is to imagine using a GPS. If you miss a turn, it does not tell you that you failed. It simply recalculates and gets you back on track.

Money management works the same way. Tracking your progress gives you the information you need to make small adjustments and keep moving toward your goals.

The exact systems you use will depend on your goals, but the principle is the same.

Track the numbers that matter, check in on your goals regularly, and make small adjustments as needed. These habits compound over time and help you maintain the momentum you built in the earlier steps.

Below is a sample checklist you can use to get you on track.

Final Thoughts on Managing Your Money Better

Learning how to manage money is a skill. Don’t expect all systems to fire perfectly each and every week. However, if you commit to the process, you can expect to get better and better over time.

Things may be difficult at first. It doesn’t always go as planned.

When things do go wrong, stick with the fundamentals of:

- Knowing where you are today so that you can make intelligent decisions about how to improve.

- Managing your cash flow to help you accomplish your goals.

- Prioritizing your most important financial goals by paying yourself first.

- Automating as much as possible.

- Tracking what’s important so you know whether you’re making progress.

These fundamentals will help you take control of your finances and lay the foundation for a solid financial future. They can even help you live without a job, if your goal is full financial independence.