Point and Unlock both let you access your home’s equity without taking on a traditional loan.

In this side-by-side comparison, I’ll cover how each program works, key differences, costs, risks, and who they’re best for.

Key Differences Between Point and Unlock

The biggest difference comes down to timing. Point gives you up to 30 years to settle, while Unlock requires repayment within 10.

Other key differences to highlight upfront include:

- Unlock allows partial buyouts during the agreement term, while Point requires full payment at once.

- For renovation value, Unlock excludes documented improvements from its share calculation, whereas Point includes them but applies a cap that can limit your payment if appreciation is significant.

- Unlock may permit homeowners to access a higher amount of equity in relation to their mortgage debt, while Point requires maintaining at least 27% equity after funding. However, actual borrowing limits depend on various factors, as not all properties qualify for maximum LTV.

Below is a quick rundown of the key features. I’ll get into the pros and cons of each next.

| Feature | Point | Unlock |

| Term length | Up to 30 years | Up to 10 years |

| Repayment flexibility | One-time buyout anytime (no partial paydowns) | Allows partial buyouts during the term |

| Processing fee | Up to 3.9% of the investment amount subject to a $2,000 minimum. | Up to 4.9% of the total investment amount (e.g., $4,900 on a $100,000 investment) |

| Maximum investment | Up to $600,000 | Up to $500,000 |

| Minimum credit score | Accepts credit scores as low as 500 | Accepts credit scores as low as 500 |

| Max combined LTV | Must maintain at least 27% equity after funding. | Must maintain at least 20% equity after funding. |

| Property Types | Residential real estate including single-family homes, condos, townhomes, and 2–4 unit properties (excluding manufactured homes). Available for owner-occupied, rental, and second homes. | Residential real estate including single-family homes, condos, townhomes, and 2–4 unit properties (excluding manufactured homes). Available for owner-occupied, rental, and second homes. |

| Renovation adjustment: | Not offered, but has a cap on maximum payout. | May exclude documented renovation value from its share calculation. |

| State Availability | AZ, CA, CO, CT, FL, GA, HI, IL, IN, NC, MD, MI, MN, MO, NV, NJ, NY, OH, OR, PA, SC, TN, UT, VA, WA, WI, DC | AZ, CA, FL, HI, ID, IN, KY, MI, MO, MT, NV, NH, NJ, NM, NC, OH, OR, PA, SC, TN, UT, VA, VT, WA, WI, WY. |

| Learn More | Point Review | Unlock Review |

If you’re new to the concept of home equity investments, check out my deep dive on how home equity investments work and their key pros and cons. I won’t cover those basics here—instead, I’ll jump straight into the details of how Point and Unlock structure their deals.

How Point Works

Point offers a Home Equity Investment (HEI) designed to provide cash today in exchange for a share of your home’s future appreciation above a risk adjusted baseline.

Like most HEIs, there’s no monthly payments. Here’s the specific structure and process:

- Application and Underwriting. You start by pre-qualifying online, then move into underwriting, which includes a home appraisal and a review of your credit profile. While Point accepts credit scores as low as 500, your profile can still affect your offer. After underwriting, you’ll receive a formal offer from Point. There are no out-of-pocket costs unless your HEI funds. At that point, fees—including Point’s processing fee (up to 3.9%) and closing costs like the appraisal—are deducted from your funding amount.

- Flexible 30-Year Term. You have up to 30 years to settle with Point. You can exit the agreement anytime by selling your home, refinancing, or using your savings—there’s no prepayment penalty for settling early. If you haven’t exited by year 30, you’ll need to settle at that time.

- How Repayment Works. Upon exit, your repayment amount depends on your home’s value at that moment relative to a “risk-adjusted” baseline. If your home appreciates, you repay Point’s original investment plus an agreed-upon share of the appreciation above this adjusted baseline. If your home depreciates, Point shares in the loss, reducing what you owe. Keep in mind, the way the math works, you may still owe Point more than their investment,if your home declines in value but not at a value below the baseline.

Point Review Video Summary

Prefer watching over reading? In my video review of Point, I explain how home equity investments work and share real-world examples to help you decide if it’s right for you.

Understanding Point’s Risk-Adjusted Baseline

The key to understanding your agreement with Point is how the risk-adjusted baseline works. Instead of using your home’s full appraised value, Point sets a lower starting value to account for risk factors in the housing market as well as the opportunity to share in the downside in the event of a significant decline in property values.

They then take a share of appreciation above that adjusted baseline. This means they don’t benefit from 100% of your home’s value—but the lower baseline also gives them more protection if your home decreases in value.

This structure makes it different from a straightforward trade—like giving up 10% of your home’s value for 15% later. Instead, your actual cost depends on how that baseline is set and how much your home appreciates above it by the time you exit.

To set this baseline, Point applies a flat risk adjustment—usually between 25% and 30%—based on factors like your credit and existing debt. That adjustment lowers the starting value used in the agreement, which in turn affects how much of your home’s future appreciation Point shares in.

Let’s say your home is appraised at $500,000 and Point applies a 27% risk adjustment. That brings the starting value of your home down to $365,000 for the purposes of the agreement.

You receive $50,000 in exchange for agreeing to share 21.4% of any future appreciation above that $365,000 baseline. Fast-forward six years, and your home’s value hasn’t increased—it’s still worth $500,000. In this scenario, if you’re looking to exit, you will owe them $79,000.

That figure includes the original $50,000 investment plus their share of the “baseline-adjusted” growth. Let’s go into some examples to see how this works:

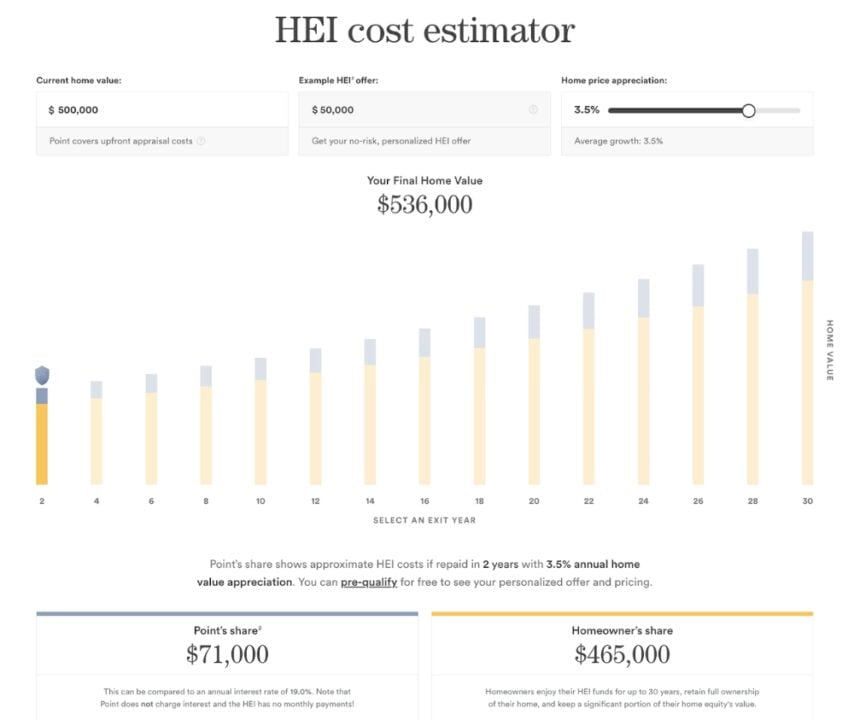

Point Example #1: How Much Point Could Cost in Year 2

Point offers a cost estimator on their website that lets you adjust home appreciation and repayment timelines. In this example, the homeowner takes out a $50,000 HEI on a $500,000 home. After two years of 3.5% annual home price appreciation, they repay Point $71,000.

These numbers come before fees, which would reduce the net cash received at the start and impact the effective annual rate.

| Scenario | Amount |

| Home’s Starting Value | $500,000 |

| Investment from Point | $50,000 |

| Home Value After 2 Years | $536,000 |

| Total Paid Back to Point | $71,000 |

| Homeowner’s Share | $465,000 |

| Effective Annual Rate | 19.0% (approx.)* |

*Point applies a Homeowner Protection Cap, which limits how much they can ultimately collect. That cap varies by homeowner and is given during underwriting. In this case, the repayment is capped around a 19% annualized rate over two years.

This example is helpful because it shows a shorter-term scenario with Point. In this example, the 19% annualized return to Point would not make sense for low-stakes expenses like buying a car or taking a vacation. However, it could be justified if you’re using the funds to:

- Avoid a large retirement account withdrawal, which could trigger fees and taxes.

- Avoid bankruptcy

- Keep a business running

- Pay your mortgage and necessary living costs

In other words, Point, or really any home equity sharing company, isn’t trying to be the cheapest way to borrow. It’s an alternative for homeowners who may not qualify for traditional financing.

Point Example #2: What It Looks Like to Settle After 20 Years

This is where Point’s longer-term structure offers some more stability. In this example, the homeowner again takes out $50,000 on a $500,000 home. But instead of exiting in two years, they wait 20 years.

With average home appreciation of 3.5% annually, their home is now worth $995,000. Point’s share at that point is $185,000, while the homeowner keeps $810,000.

| Scenario | Amount |

| Home’s Starting Value | $500,000 |

| Investment from Point | $50,000 |

| Home Value After 20 Years | $995,000 |

| Total Paid Back to Point | $185,000 |

| Homeowner’s Share | $810,000 |

| Effective Annual Rate | 6.8% (approx.) |

This example shows how Point’s costs can look much more reasonable when you hold the agreement long term. Here, the effective annual rate is about 6.8% (before fees)—a big drop from the 19% short-term example.

Why? The risk-adjusted baseline still applies, but since you’re holding the agreement for 20 years, the appreciation is spread over a longer period—reducing the impact of Point’s share when calculated on an annualized basis.

So, if you plan to stay in your home long term and want to avoid monthly payments, Point can be a more viable option.

For more real-life examples, cost breakdowns, and analysis, check out my full Point Home Equity Review.

How Unlock’s Home Equity Agreement Works

Unlock offers a Home Equity Agreement (HEA), which allows you to access cash today in exchange for a share of your home’s future value—without taking on monthly payments or traditional loan interest.

Unlike Point, which takes a share of appreciation above a risk-adjusted baseline, Unlock acquires a fixed percentage of your home’s total future value.

This makes Unlock’s structure simpler, but not directly comparable. Here’s how their process works.

- Application & Funding. You can get a quick estimate online in just a few minutes.. If you move forward, Unlock reviews your financial history, conducts an appraisal and runs a title report. Credit scores as low as 500 are accepted, and income isn’t required, though your financials impact the terms you may receive. Once underwriting is complete, you’ll receive an offer. Unlock charges a 4.9% origination fee (deducted from the cash payout), along with third-party closing costs like appraisal and escrow fees.

- 10-Year Term with Flexibility. Unlock’s agreement lasts up to 10 years. You can buy them out anytime during this term. But, by the end of that term, you must settle with Unlock. You can do this using savings, a cash-out refinance, a home equity loan or HELOC, by selling your home, or using other sources of funds.

- Partial Buyouts Allowed. Unlock lets you buy back part of their share before the 10-year term ends. There’s a transaction fee for partial buyouts, so it’s more practical to make one or two larger payments rather than small incremental ones. For example, you might repurchase 25% of your equity at year 5 and the remaining portion later.

- Exchange Rate. Unlock determines your HEA cost based on two factors: the percentage of your home’s value you access upfront and the exchange rate assigned during underwriting. The exchange rate—currently ranging from 1.7 to 2.05 —acts as a multiplier based on several factors, such as your financial profile, equity, and property risk. For example, if you take out 10% of your home’s current value and your exchange rate is 2.0, you’ll owe 20% of your home’s future value when the agreement ends. This percentage is fixed at signing and doesn’t change, regardless of how your home appreciates.

- Repayment: When you settle, you owe Unlock their fixed share of your home’s total market value at that time—not just the appreciation—plus the return of their original investment.

- Unlock’s Annualized Cost Limit. Unlock sets an annualized cap on how much your agreement can cost per year, similar to putting a limit on how much “interest” you’d effectively pay. If your home appreciates quickly and your repayment amount grows too fast, this cap kicks in to make sure that your annualized cost does not exceed the cap —typically around 19.9%.

Unlock Example #1: How Much Unlock Could Cost in Year 2

This estimate comes directly from Unlock’s cost estimator. In this scenario, the homeowner receives $54,000 upfront—about 10.8% of their home’s current value—with settlement based on a fixed share of the home’s future value. The home starts at $500,000 and grows 3% annually for two years, ending at $530,450.

| Scenario | Amount |

| Starting Home Value | $500,000 |

| Investment from Unlock | $54,000 |

| Unlock’s Percentage (Share of Future Value) | 15% |

| Home Value After 2 Years | $530,450 |

| Total Paid Back to Unlock | $77,630 |

| Homeowner’s Share | $452,820 |

Let’s assume that the Annualized Cost Limit of 19.9% did not apply. In the absence of the 19.9% cap, Unlock’s share of the ending value of the home would have been $105,983, which translates to an annualized cost of 40%.

As a result of the Annualized Cost Limit, the homeowner settles their agreement with Unlock for $77,630. This example illustrates how, in short-term scenarios, the annualized cost cap can reduce the amount you owe when applicable.

Unlock Example #2: How Much Unlock Could Cost in Year 10

In this scenario, the homeowner receives $54,000 upfront—about 10.8% of their home’s current $500,000 value. Over the 10-year agreement, the home appreciates 3% annually, growing to $671,958. Here’s where Unlock’s exchange rate becomes critical.

While Unlock’s 19.9% annualized cost cap tends to limit repayment amounts in short-term scenarios, it’s the exchange rate that matters most in longer agreements. Currently ranging from 1.70 to 2.05, , the exchange rate multiplies the upfront percentage you receive (here, about 10.8%) to determine the future percentage owed (or 19%). In this example, Unlock’s share of 19% of the home’s value ($127,627 ) equates to an annualized cost of approximately 9.4%.

This means whether you settle in year 2 or year 10, the percentage you owe remains fixed at signing but the settlement amount is subject to the annualized cost limit. The difference is that by year 10 your home has appreciated more significantly—so while the percentage owed stays the same and you’re paying a larger total dollar amount, your actual annualized cost is much lower and no longer subject to the annualized cap.

For more real-life examples, cost breakdowns, and analysis, check out my full Unlock Home Equity Review.

Who Each Option Is Best For?

If you want to avoid settling within 10 years, Point’s 30-year term is an advantage. It’s better suited for homeowners who plan to stay put and want the freedom to settle on their own timeline.

If you think you’ll exit in under 10 years and want the option to partially settle in large chunks along the way, Unlock could be a better fit. Its simpler structure and partial buyout feature may give you more control in the short term.

Keep in mind, this analysis doesn’t factor in your specific offer. With home equity investments, the terms you receive after underwriting can vary significantly between companies based on your credit, equity, and property.

Unlike a traditional HELOC—where interest rates and fees are more standardized—there’s no simple apples-to-apples comparison. One company might offer better terms than the other for your situation, so it’s worth applying to both if you’re seriously considering this route and both fit your timeline.

From there, make sure to review offers carefully and run the numbers based on your goals.

Home Equity Agreements are offered by Unlock Home Equity Solutions, Inc. Terms and conditions apply; not all homeowners will qualify and availability varies by state. In certain states, HEAs may be classified as loans. Unlock Technologies, Inc. is licensed under NMLS ID #2657081.