At a Glance

- Research shows the debt snowball is most effective when someone has several debts, because paying off a small balance first increases follow-through.

- With only two or three debts, the behavioral advantage is less clear.

- You can compare both approaches easily, and this guide shows you how to calculate which one works best for your situation.

When you’re buried in debt and unsure where to start, momentum can make all the difference.

I often recommend the debt snowball method to people who feel stuck. They want to get out of debt, but the next step is not clear. What they need most is a quick win, something small but meaningful that proves progress is possible.

That is where the debt snowball can help.

In this guide, I will walk you through exactly how the method works, when it tends to be most effective based on what I have seen, and when I usually recommend choosing a different approach.

How The Debt Snowball Method Works

In Dave Ramsey’s Baby Steps, the debt snowball comes after saving a $1,000 emergency fund.

The idea is simple. You list your debts from smallest balance to largest, put all extra money toward the smallest one, and pay the minimum on everything else.

When that first debt is gone, you move to the next smallest.

Each payoff gives you a clear sense of progress, which is why people often describe it as a snowball gaining speed as it moves forward.

Here is an example to show how this looks in real life:

| Debt | Amount | Interest Rate |

| Credit Card #1 | $500 | 18.4% |

| Credit Card #2 | $4,500 | 13.2% |

| Auto Loan | $3,200 | 8.5% |

| Student Loan | $25,000 | 6.2% |

Here’s the order you’d pay them off in:

| Debt | Amount | Interest Rate | Order |

| Credit Card #1 | $500 | 18.4% | 1 |

| Credit Card #2 | $4,500 | 13.2% | 3 |

| Auto Loan | $3,200 | 8.5% | 2 |

| Student Loan | $25,000 | 6.2% | 4 |

Upon elimination of the lowest balance, you’d then move on to the next smallest debt:

| Debt | Amount | Interest Rate | Order |

| Credit Card #2 | $4,500 | 13.2% | 2 |

| Auto Loan | $3,200 | 8.5% | 1 |

| Student Loan | $25,000 | 6.2% | 3 |

Debt Snowball vs. Debt Avalanche

The most popular alternative to the debt snowball method is the debt avalanche, which entails paying off your debts in the order of highest interest rate to lowest interest rate (while still making the minimum monthly payments on your other debts).

So, keeping with the previous example, using the debt avalanche your debts would be paid off in the following order:

| Debt | Amount | Interest Rate | Order |

| Credit Card #1 | $500 | 18.4% | 1 |

| Credit Card #2 | $4,500 | 13.2% | 2 |

| Auto Loan | $3,200 | 8.5% | 3 |

| Student Loan | $25,000 | 6.2% | 4 |

The main advantage of the avalanche is that it saves more money on interest and, on paper, gets you out of debt faster.

In this example, using the snowball costs about $309 more in interest and adds an extra two months before you are debt-free.

However, that is not always how it works in real life.

If you want help running the numbers, our science backed Get Out of Debt spreadsheet can help. It lets you list your debts, compare payoff order, and see how long each method would take using the exact same monthly payment. You can download it for free on our Get Out of Debt page.

When the Debt Snowball Method Works Best

There have been a few interesting studies that have compared the two methods.

First, a study from a team at Northwestern University found that the debt snowball method was a better strategy for those with multiple credit card debts.

Similar results were found in a study published in The Journal of Consumer Research were they found:

“People are more motivated to get out of debt not only by concentrating on one account but also by beginning with the smallest.”

This research lines up from what I have seen personally.

The people who benefit the most from the debt snowball are the ones who feel completely overwhelmed by multiple debts.

They may have three or four credit cards, a car loan, student loans, and other balances competing for their attention.

They want to make progress, but they do not know where to start.

When someone is juggling many debts, the snowball gives them a simple first step and a clear, achievable goal.

Paying off one small balance provides a win they can actually feel. That win builds confidence, and confidence builds momentum. Five debts become four, then four become three, and the process starts to feel manageable again.

A perfect mathematical plan only works if someone can stick with it. Many people need visible progress to stay committed. That is why the snowball is so effective for anyone who has felt stuck or discouraged.

When the Debt Snowball Does Not Make Sense

The debt snowball is helpful when you need motivation, but it is not the right fit for every situation.

The math is always going to point to paying off your highest interest rate debt first. In other cases, the smartest move is not to focus on debt payoff at all, especially when you have opportunities like a 401(k) match that offer a stronger return.

Here are the most common situations where I usually do not recommend the snowball.

1. You have a very high interest debt that is much larger than your other balances

Behavior matters, but math still matters too. If you have a credit card balance at a very high rate, it often grows faster than you can chip away at it using the snowball. In that case, you usually want to make it your top priority.

For example, imagine someone has a $12,000 credit card balance at a high rate and a $4,000 car loan at a much lower rate that is almost paid off. The car loan would be first in the snowball.

The credit card interest is costing you far more each month, and paying it down sooner reduces real financial risk.

2. You are choosing between paying off low interest debt or getting a 401(k) match

This is a situation where the math is very clear. If you have access to a 401(k) match, it is usually one of the best guaranteed returns you can earn. For many people, it does not make sense to delay investing in the match in order to pay off a low rate car loan or student loan more quickly.

The Baby Steps framework encourages paying off all debt before investing, but this is one area where the recommendation is worth reconsidering.

The compounding you miss in the early years of investing can add up to a very large amount over decades. As long as you are managing the debt responsibly, capturing the match often provides more long term benefit.

3. You are already disciplined with money and do not need the behavior boost

The debt snowball is most helpful when motivation is the main barrier.

If you already manage your budget well and have room to make meaningful payments toward your debt, you may not need the behavior boost the snowball provides.

In that case, paying your highest interest rate debt first will usually save you more money and shorten the payoff timeline.

There is a lot I respect about Dave Ramsey’s approach, and there are also areas where I disagree. I break down the tips I recommend and the ones I suggest avoiding in my guide to Dave Ramsey’s best and worst advice.

Our Debt Snowball Worksheet

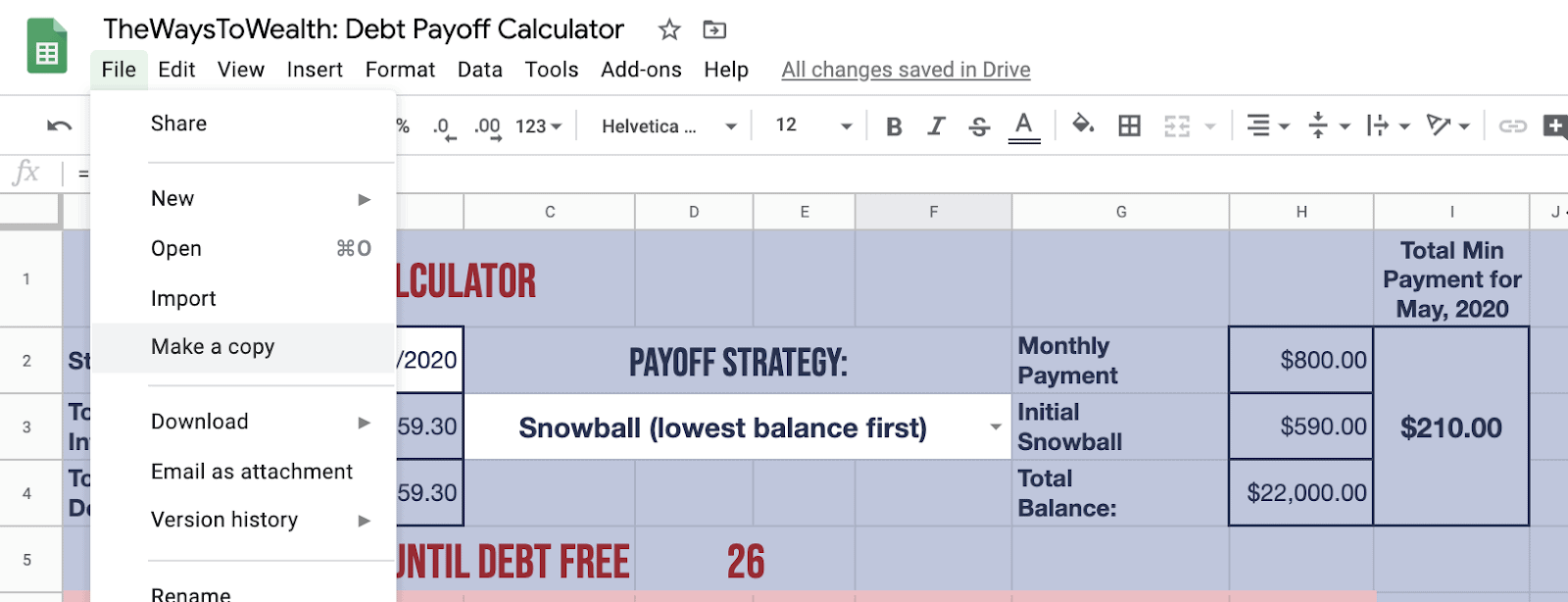

To help you run the numbers for yourself, we created a free debt snowball calculator/worksheet inside of Google Sheets.

The file is locked from editing, so the first thing you’ll need to do is go to File > Make a Copy. This will give you your own private version of the spreadsheet.

Note: Because of some differences in Google Sheets and Microsoft Excel, this spreadsheet doesn’t work in the latter. So you’ll need to be logged into a Google Account (e.g., Gmail) in order to save a copy of the spreadsheet to your Google Drive.

The rest of this post will walk you through the entire debt snowball process, from beginning to debt-free.

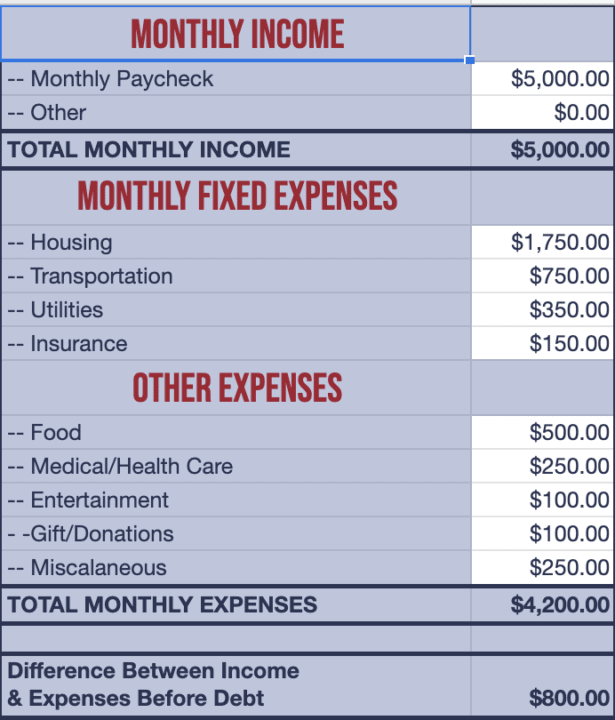

Step 1: Create A Monthly Budget

First things first: you’ll need to know how much money you have available to apply to your debt snowball each month.

To get this figure, you need to create a monthly budget that shows the difference between your income and expenses.

If you’re using the debt payoff spreadsheet, this is located on the first tab:

Related Reading: The best budgeting and personal finance apps.

Step 2: List Your Debts

For some people, the scariest part of the process is figuring out how much you actually owe.

But don’t beat yourself up for carrying a large amount of debt. What’s done is done. At this point, past decisions don’t matter. The only thing that matters now is what you do from here on out.

The first thing you want to do is gather all your loan statements and/or account logins. But don’t stop there. To make sure you’re paying off any and all debts, you want to get a copy of your credit report.

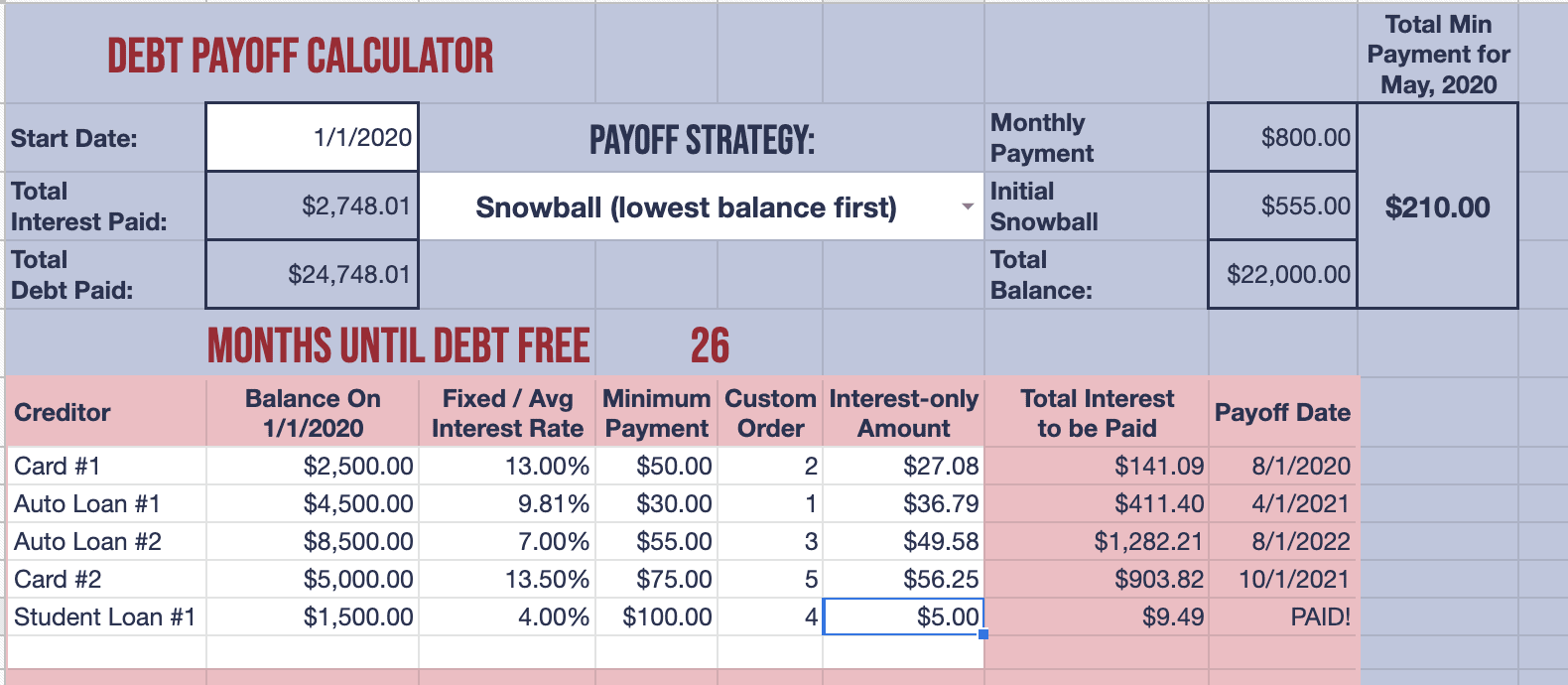

Once all the information is gathered, head over to the second tab on the spreadsheet and complete each column:

Step 3: Make Your Minimum Payments

For every debt besides the one with the lowest balance, you’ll be paying the minimum due.

To save yourself some time each month, I’d automate each minimum payment. This also eliminates the chance for potential late payment fees, which may hurt your credit score.

Step 4: Tackle Your Smallest Debt

Now it’s time to put every penny of extra money toward the debt with the smallest balance — every single month until it’s paid off. Any wiggle room in your budget should be devoted to this cause.

If you completed the spreadsheet, the amount you’ll have to throw at that debt is listed in the top right corner.

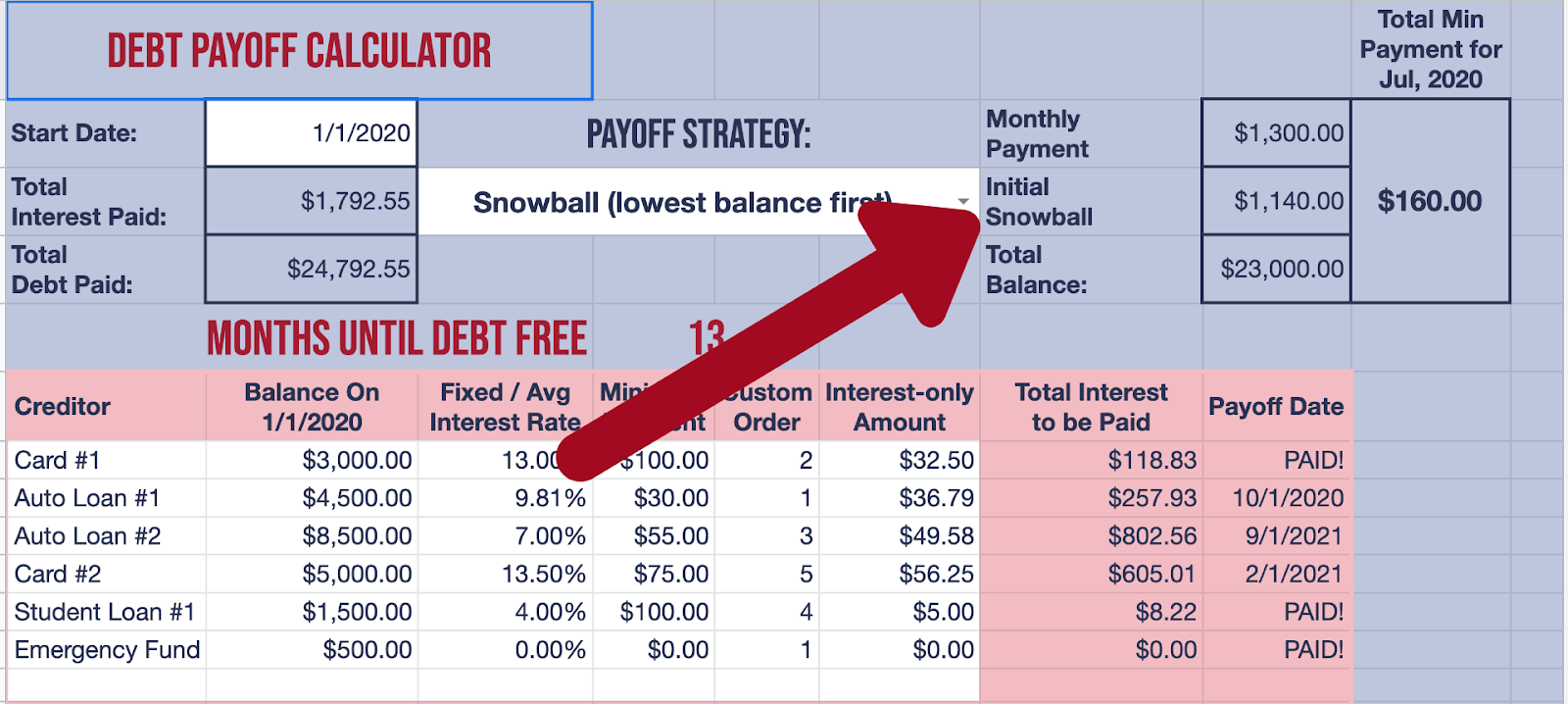

Step 5: Move On To The Next-Smallest Debt

Thanks to all of your hard work, you’ve paid off your first debt. Congratulations!

That excitement and sense of encouragement you’re feeling? That’s momentum!

Now keep using the debt snowball method to tackle your next challenge.

Move on to the next-smallest debt, adding in the payment you were making on the last debt.

For instance, if you were paying $100 on a credit card balance that you just retired, that $100 will now go toward the next debt (in addition to the minimum monthly payment you were already making on it).

Step 6: Rinse And Repeat

Keep using the debt snowball method to knock out all your debts, one by one. As you retire each debt, keep adding what you were paying towards the next debt.

Before long, you’ll find yourself on your last one! Keep plugging away at it until your debts are totally gone.

Debt Snowball FAQ

Dave Ramsey is responsible for branding and popularizing the term “debt snowball,” which is Step #2 in his popular baby steps wealth-building framework. As for the strategy itself, it was around long before Ramsey gave it a name.

Dave Ramsey lists having a baby, losing your job, going through a health crisis, going through a major life change (like a divorce), and bills owed to the IRS as reasons that may cause you to pause your debt snowball.

First things first: you need to run the numbers yourself. You’ll just need to change the dropdown menu on the spreadsheet from “Debt Snowball” to “Debt Avalanche” to see the difference between the two.

Specifically, pay attention to what each will cost you. Is it the difference between a few hundred dollars? If so, I’d stick with the debt snowball method. And this is most often the case.

On the other hand, is it thousands of dollars? If so, I’d start leaning towards the debt avalanche method.

Bottom Line: Start With Wins That Make Sense

Small wins can help you build momentum, but they are not the only factor to consider.

The math will always favor paying your highest interest debt first, especially when you have one or two balances and a clear standout rate. In those cases, targeting the high interest debt can save real money, even if a smaller balance is available.

The picture changes when your list starts to grow. Once someone has three, four, or even more debts, the biggest challenge is often overwhelm. In those situations, the debt snowball gives you a simple place to start and a win you can actually see, which is why it works so well for people who feel stuck.

If you want more help creating a plan that builds on Dave Ramsey’s advice while understanding its pros and cons, you may find these guides helpful:

- Dave Ramsey’s Allocated Spending Plan: Guide and Forms

- Is Dave Ramsey Right About How Much House You Can Afford

- Dave Ramsey Envelope System: The Ultimate Guide

- Dave Ramsey’s Household Budget Percentages