This is a complete step-by-step guide on how to start investing.

For beginners, there are many big decisions to make when you’re starting to invest. At first, it can seem overwhelming. But by the end of this guide, you’ll see that successful investing is not complicated. Better yet, you’ll learn the simple strategy that has consistently beat investing professionals for decades.

Here’s exactly what we’ll cover in this guide:

- What is investing?

- Why should you invest?

- When is the right time to invest?

- Different types of investments

- How to start investing in four steps

- Tips for successful investing

What Is Investing?

Investing is how you allocate existing assets and cash flow for a future desired benefit. Understanding this definition is important because it touches on how you should think about investing from the fundamental level.

First, you have to take inventory of your existing assets — mainly the cash you have available to invest. Plus, you should consider your current cash flow situation, which is the amount of money you’re able to invest going forward based on existing income and expenses.

Second, you have to know why you’re investing, and more specifically, the goals you’re trying to accomplish.

Why Should You Invest?

One of the most important financial decisions you’ll make, if not the most important, is whether you allow compound interest to work for or against you.

Having compound interest work for you over your lifetime is like swimming downstream. Better yet, the longer you swim, the easier and faster you’re able to swim.

Not taking advantage of it is like swimming upstream. The longer you swim upstream, the harder and faster the current works against you.

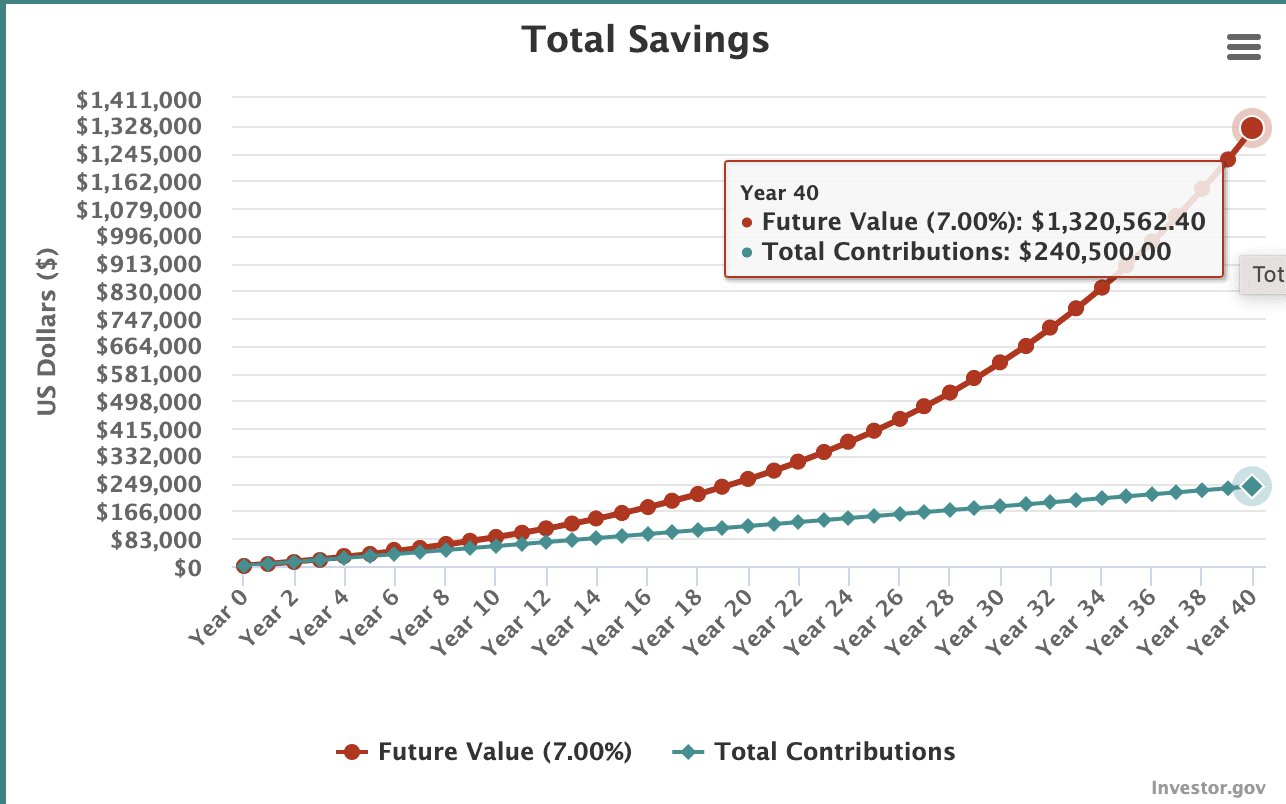

What investing does is it allows you to take advantage of compound interest. Investing $500 a month for 40 years, earning 7% a year (the average rate of return in the stock market), allows you to build a portfolio worth $1,320,562.

On the other hand, what happens when you let compound interest work against you?

Let’s say you have $10,000 of credit card debt at an 18.9% interest rate. You’re then only able to make a 4% monthly minimum payment on the debt. In total, it will take you 13 years and nine months to pay off that debt, and it will cost a total of $16,357.

Related reading: How to start investing as a teenager.

When Is the Right Time to Start Investing?

To reiterate, investing is how you allocate existing assets and cash flow for a future desired benefit. What successful investing looks like is producing the highest return possible for a given level of risk to achieve your goal.

When you look at investing through this lens, everyone is an investor — even if they don’t own a single share of stock. We’re all constantly deciding what the highest and best use of our money is.

When it comes to investing money in stocks, the right time is when your investment will produce the highest return possible for a given level of risk and desired result.

To put this in context, let’s say your goal is to accumulate wealth and you’re wondering whether you should pay off debt or invest. Historically, the stock market has returned about 7% per year after inflation. If you have high-interest debt at 18%, prioritizing paying that off over investing in the stock market allows you to accumulate wealth faster. Plus, the investment to pay off that debt is risk-free.

Looking at the numbers, it makes sense to start investing in the stock market once you’ve paid off your debts with an interest rate greater than 7%.

One unique situation is a 401(k) employer match. It’s here where you can often earn an immediate 50% on your money guaranteed. In this case, the numbers would tell you to maximize your employer match, then use the rest to pay off high-interest debt.

This isn’t a strict rule by any means. There is some wiggle room depending on your goals and financial situation. However, it’s a good break-even point for you to make the decision.

Different Types of Investments

There is an infinite amount of possible investments. Paying off debt over investing is an investment. So is investing in your own education. In each case, you’re sacrificing money today for a future desired benefit.

When it comes specifically to investing in the traditional sense (like for retirement) the four most popular types of investments are:

- Stocks. Also referred to as equities, stocks are a legal claim on part of the assets and earnings of a corporation. Historically, stocks have the highest overall returns of any asset class, but they come with the most risk. (Learn more about how to invest in stocks as a beginner.)

- Bonds. A bond is essentially a loan you make to a company or the government. You then earn interest based on the agreed-upon terms. There is a wide range of bonds available to invest in, but bonds are most often used to reduce risk within a portfolio.

- Cash. In investing terms, cash is how you refer to money market instruments, such as savings or money market accounts. Cash has the lowest performance of any major asset class, but also comes with very little risk. Long-term, cash isn’t a good investment because inflation erodes its value.

- Alternatives. Alternative investments, such as crypto and real estate, have become more popular in recent years. In our current low interest rate environment, more investors are turning towards alternatives and away from bonds and cash. There is a wide range of risks and returns available in the alternative space.

Beyond these categories of investments, there are different ways to invest in them.

- Mutual Funds. Mutual funds are how you can invest in a pool of stocks and bonds without picking each individual one yourself. Mutual funds offer investors easy access to managed investing. There are both passive and actively managed mutual funds. Passive funds aim to replicate the performance of an index, whereas active funds employ a fund manager to pick investments in an attempt to outperform their benchmark.

- Exchange-Traded Funds. ETFs allow you to invest in a pool of assets, such as stocks or bonds, similar to how you would with mutual funds. However, unlike mutual funds, ETFs give investors the ability to trade shares (in the fund itself). ETFs are useful when you’re looking to buy mutual funds through a brokerage account; you’re able to purchase a Vanguard ETF through a brokerage like SoFi, while in order to invest in Vanguard’s Mutual Funds you need an account with Vanguard.

- Robo-Advisors. A robo-advisor is how you can automatically invest in a diversified portfolio of stocks, bonds and cash. They automate this process with algorithms based on your risk tolerance, goals and timeline. Robo-advisors offer investors an easy way to build their own portfolios without hiring a professional financial advisor.

How to Start Investing in Four Steps

Successful investing requires four distinct steps.

Step #1: Know Your Goals

Without a clearly defined investment goal, it’s impossible to have a proper investment strategy.

The most common investing goal is retirement, but there are other goals worth considering.

- Short-term goals (0 to 2 years). Examples include saving for a car or a trip in the short term.

- Medium-term goals (2 to 7 years). Saving for a down payment on a home or your children’s education.

- Long-term goals (7+ years). Retirement and general wealth accumulation — including building generational wealth that can be passed down to your kids and grandkids — are reasons to invest for the long term.

It’s helpful to know the timeframe of your goal because it impacts which assets you should invest in. For example, you wouldn’t want to heavily invest in stocks when your goal is one year away because stock prices fluctuate short-term.

On the other hand, you wouldn’t want to hold a lot of cash if your goal is to save for retirement, which is more than 20+ years away, because inflation decreases that cash’s value.

Step #2: Decide How Much to Invest

With a specific investment goal in mind, your next step is to determine how much money you can invest.

When you have a long-term goal, such as retirement, it’s best to focus on your savings rate rather than saving a specific dollar amount. As a rule of thumb, you want to save at least 15%, and ideally 20%, of your gross annual income for retirement.

Keep in mind, you don’t have to hit that number this month. The goal is to work towards saving 15% to 20% over time.

For short and medium-term goals, you’ll want to give yourself more clarity on how much you actually need. For example, if your goal is to save $24,000 over the next two years for a downpayment on a home, you’ll need to invest $1,000 a month. The idea is to know how much you need, then work backward towards saving that amount on a weekly or monthly basis.

Step #3: Decide What to Invest In (Asset Location)

What you invest in depends on your goals and time horizon. The further away you are from your goal, the more you can invest in stocks because they have historically outperformed bonds, cash and real estate — even though they’re more volatile in the short-term.

Picking individual stocks to invest in is very risky, and the research overwhelmingly shows that individual investors who pick stocks perform far worse than those who invest in passively managed mutual funds and ETFs.

Robo-advisors, such as Betterment, are a good option for the very hands-off investor. With a robo-advisor, you’re able to get an optimized portfolio, based on your goals and risk tolerance, for a very reasonable fee.

For goals less than two years away, it’s best to stick to very safe investments. Yes, savings accounts pay very little, but with your goal right around the corner, it’s not worth the risk of losing a significant sum of money.

For your medium-term goals, it’s possible to invest in a diversified portfolio of stocks, bonds and cash. The closer you are to your goal, the more you’ll want to stick with safer investments like cash.

Step #4: Decide Where to Invest

Asset location is the decision of where to invest. Options include a 401(k), IRA, brokerage account and college savings account (just to name a few).

Retirement accounts like 401(k)s and IRAs (see: Roth vs. Traditional IRA) offer tax benefits, which can help increase your returns over time. The downside is that in order to take money out of these accounts before retirement, there’s often some type of tax and penalty.

If available, it’s a smart decision to max out your employer 401(k) match. This is free money, and really part of your compensation, so you’ll want to take full advantage of it.

Investing for short and medium-term goals should happen outside of a retirement account. With a brokerage account, you can withdraw your money by paying only capital gains tax (there are no penalties).

For retirement investing, my personal preference is to:

- Invest in a 401(k) up to your employer match.

- Max out a Roth IRA, if qualified.

- Invest in a taxable account.

To me, this represents a good balance of taking advantage of the tax benefits of retirement accounts and having the liquidity of a taxable account if shorter-term needs arise.

Four Tips for Successful Investing

There are four well-researched studies that beginner investors should understand.

#1. It’s about time in the market vs. timing the market.

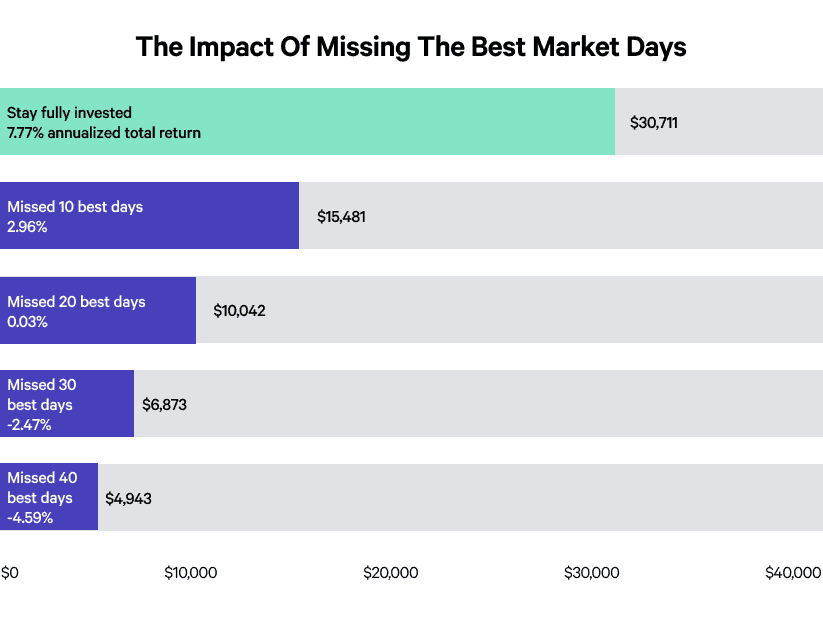

In one study, illustrated in the table below, Putnam Investments evaluated the performance of the S&P 500 over the 15-year period ending on December 31, 2019.

What they found is that if you invested $10,000 and stayed invested each and every day through that 15-year period, you’d have accumulated $30,711 — a 7.77% annualized return.

But when jumping in and out of the market, and thereby missing the 10 best-performing days (out of nearly 3,800 days), your ending balance would have been $15,481. Miss the 40 best performing days and you’d actually have a negative return of 4.59%.

While it would take some awful luck to miss each of the 10 best days, the takeaway is that there are a few crucial days where you must be in the market — and there’s no telling when those days will come. So it’s important to stay invested, as this is the only way to make sure that you don’t miss out on big single-day gains.

#2. Don’t wait to get started

Since time in the market is a crucial factor in success, it’s important to get started investing as early as you can. While we always recommend you take care of any high-interest debt first — after all, that debt sometimes costs you as much as 30% per year — investing even small sums can make a big difference down the line.

We wrote a guide to investing $50 per month in stocks, which will show you realistic ways to put a small amount of funds to good use.

Many people make the mistake of thinking they need to invest larger sums in order to have an impact. But the reality is you don’t even need $50 per month; investing anything on a consistent basis builds the habit and makes it easier to invest more when you have the means.

If you’re dealing with limited income or have had trouble setting aside money to invest, consider a micro-investing strategy, in which small amounts (often your spare change) are automatically moved from your checking account into your portfolio at specific intervals. This is easy, often painless, and you might be surprised by how fast it can start adding up.

Learn about specific options in our list of the best micro-investing apps.

#3. 85% of professionals don’t outperform the S&P 500

Professional investors, who work full-time and have teams working full-time, all in the effort to outperform the market, fail to do so 85% of the time over a 10-year period. After 15 years, 92% of mutual funds failed to outperform the S&P 500.

While professionals as well as individuals tend to get lucky every so often in the short-term, finding a strategy that works long-term is extremely rare.

Putting in more effort and seeing greater results pays off in about every other facet of life, so it’s easy to think this translates to investing. But it’s been proven time and time again that the simpler and more passive investing approach is far superior to the more complex.

#4. Don’t obsess over short-term results

When Fidelity studied individual 401(k) participants’ plans to see which type of investor performed the best, they discovered that the accounts of people who forgot they had an account were the clear winners.

Similar conclusions were found in a famous study published in the Journal of Finance, where accounts that traded the most during a five year period earn 11.4%, while the market returned 17.9% during that same period.

So don’t confuse effort with results. Especially when it comes to long-term investing, checking your balance every week or month doesn’t make you better — it makes you more likely to make a bad decision. Remember, the key is time in the market, not timing the market.

The real secret to successful investing is committing to investing a certain amount of money every month for decades — a practice known as dollar cost averaging — regardless of how the market is performing.

Related: The best portfolio tracking apps (and why tracking your investments closely may not be a great idea…)

Final Thoughts on How to Get Started Investing

Successful investing is about discipline.

- The discipline to keep your expenses lower than your income, so you’re able to invest month-in and month-out.

- The discipline to stick with a strategy long-term, even though you may want to constantly tweak things.

- The discipline to stick with a strategy through both the good times and bad.

If you can follow through with these three things, you’ll see how easy it is to make your money grow. And in doing so, how compound interest can really work in your favor over time.