This step-by-step guide walks you through the exact actions you need to take to pay off your balances and finally get out of debt for good.

Is this process easy? Most people assume the answer is “no,” but you might be surprised.

The steps outlined below are based on the science of behavioral change and are specifically designed to make getting out of debt as easy and painless as possible.

And while many personal finance gurus claim that ridding yourself of debt requires major sacrifices and extreme measures, often all it takes is a willingness to confront the problem honestly and a commitment to making a few small changes to your habits and lifestyle.

But for many people, the challenge is knowing where to start.

That’s why I wrote this guide. It will teach you in simple terms how to make and execute a plan for getting out of debt.

It also contains a custom-built calculator that will show you exactly when you can expect to be debt free.

Ready?

Let’s get started!

Step #1: Calculate Your Debt Payoff Date

In a study called Borrow Less Tomorrow: Behavioral Approaches to Debt Reduction, which was conducted by the Center for Retirement Research at Boston College, researchers created a behavior-based plan to help a group of 465 individuals get out of debt.

The goal of the first phase of that plan was gathering the facts. And while this sounds obvious, it’s not exactly the process most people follow.

Instead, most people hide from their debt.

Why? Because confronting the facts often leads to guilt and regret. It’s easier and less painful to avoid facing the truth head-on.

Unfortunately, debt compounds over time and grows into an even bigger problem the longer you avoid it. So now is the best time to face up to the facts. Because solving your debt problem is never going to be easier than it is today.

The One Fact You Need to Know

Throughout your debt payoff process, you’ll be guided by one fact: the exact number of months until you become debt-free.

This is the one number that takes into account everything, including your current debts, their interest rates, your payoff strategy and your income.

You should know this number at all times.

And, most importantly, it should be something you’re always trying to improve. That means you should recalculate it on a regular basis.

This number is so important that I created a debt payoff calculator for this exact purpose.

How to Use the Debt Payoff Debt Calculator

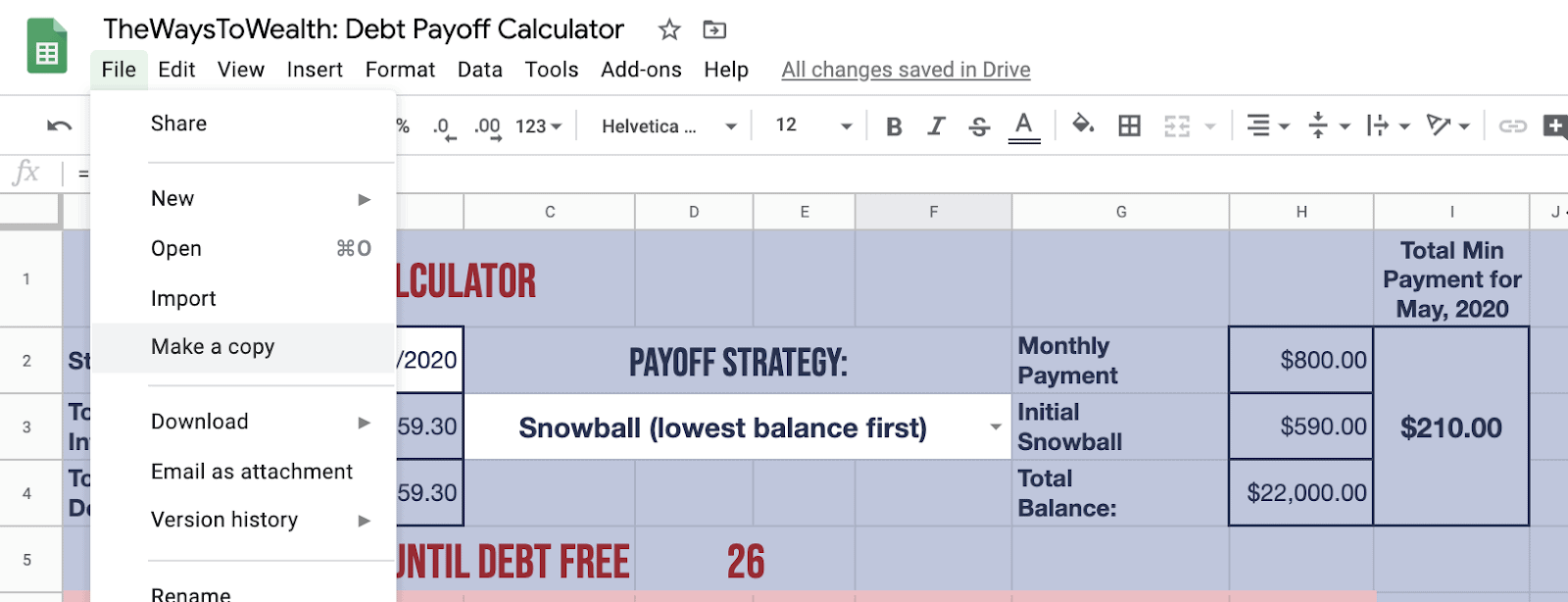

To start, you’ll need to make a copy of the calculator (which is hosted in a Google Spreadsheet) by going to File > Make a copy, as shown in the screenshot below.

Note: You need to be logged into your Google/Gmail account in order to access the “Make a copy” option.

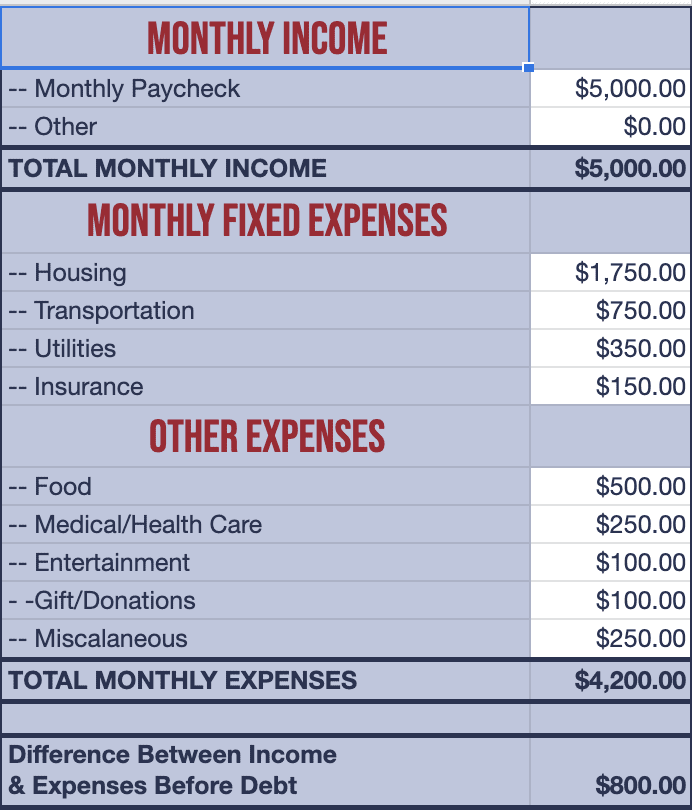

Next, in your own copy, the first step is calculating the difference between your income and expenses before debt. It’s this number that you’ll ideally put towards your debt payments each month.

Notes:

- As for the monthly budget categories, feel free to expand the categories by using Insert > Row above or Insert > Row below in the appropriate place.

- If you have the data in your favorite budgeting app, you can skip the individual categories, making sure to insert your total monthly income and expenses.

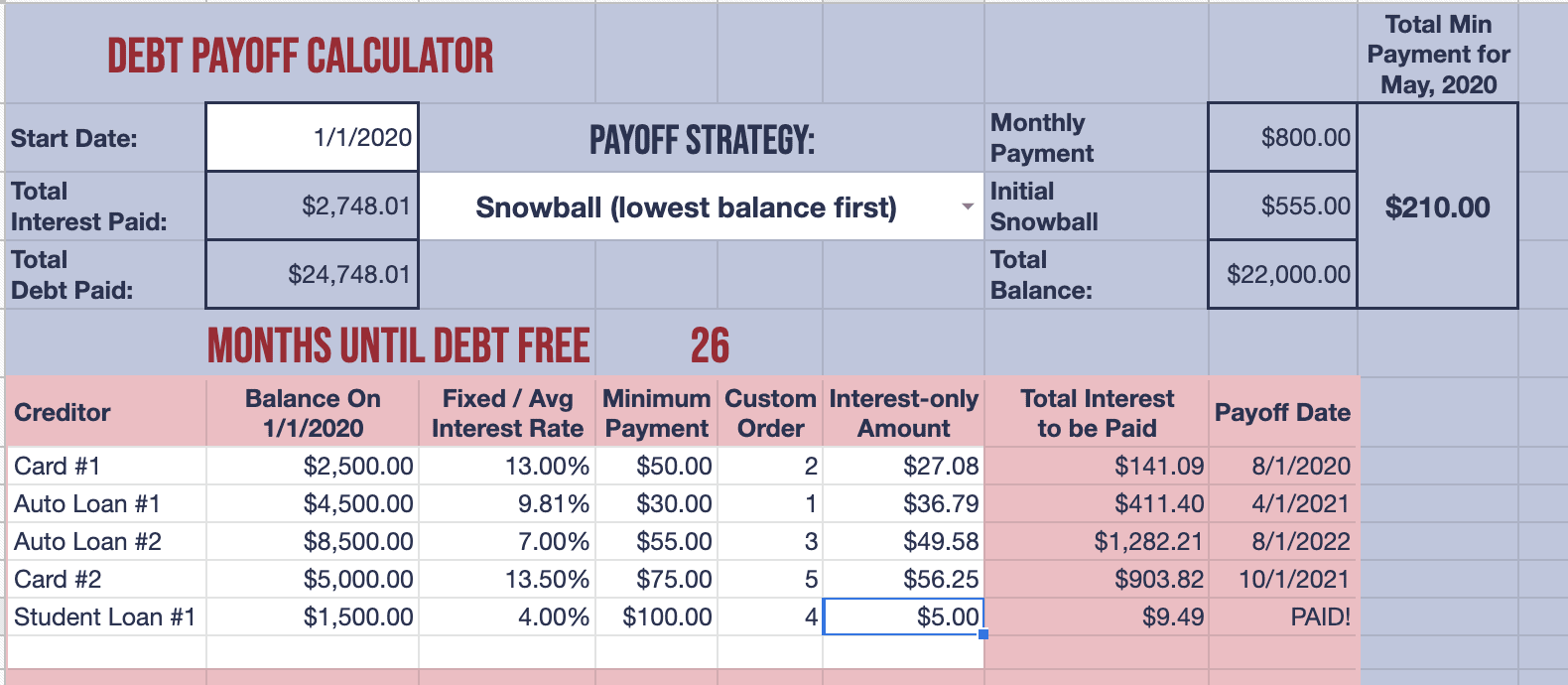

Calculating Principal + Interest

Next, you’ll want to proceed to the “Payoff Calculator” tab in the Google Sheet.

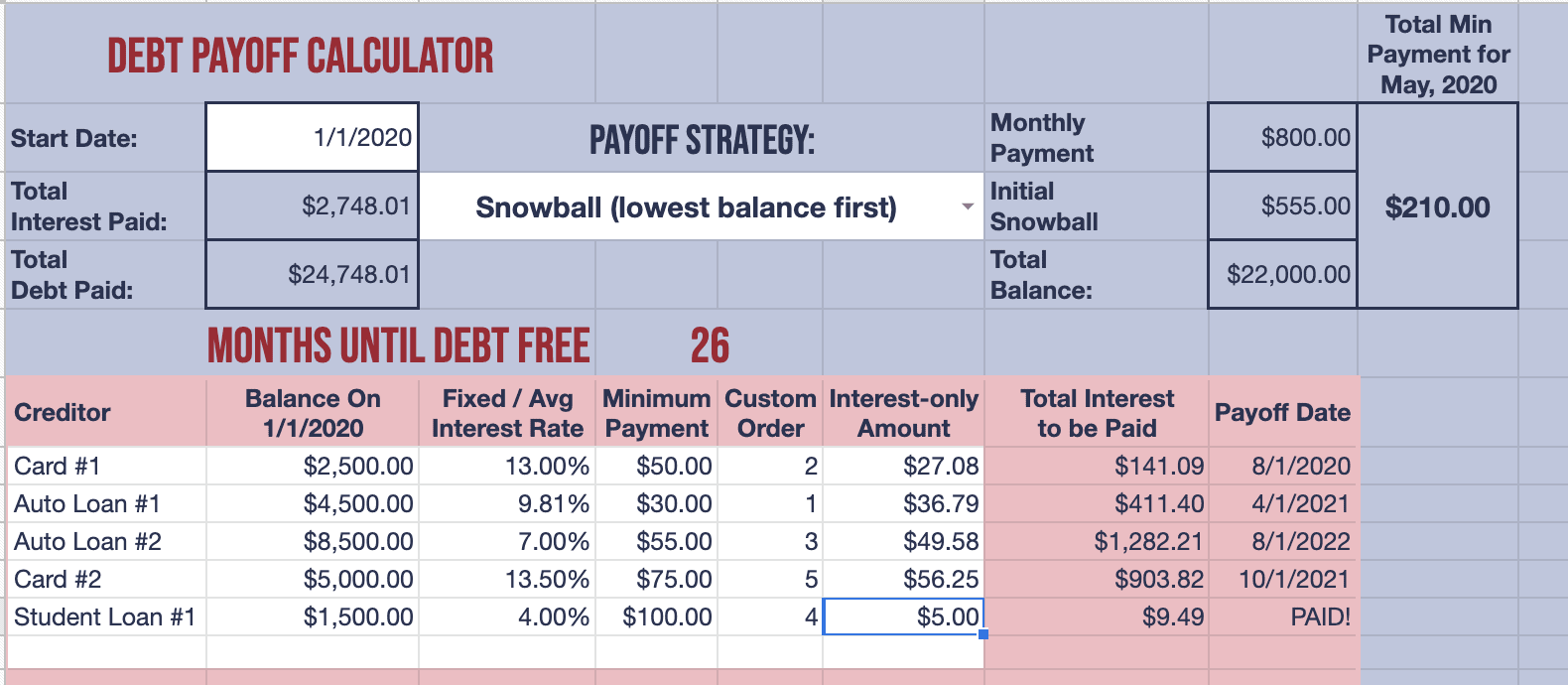

It’s here that you’ll enter your debts, including:

- Creditor. Include all your debts — car loans, credit card bills, student loans, etc. Note that your housing costs (such as your mortgage) get counted as part of your budget, and are therefore entered on the previous tab.

- Balance. Enter how much you owe on the date you start your debt-payoff journey.

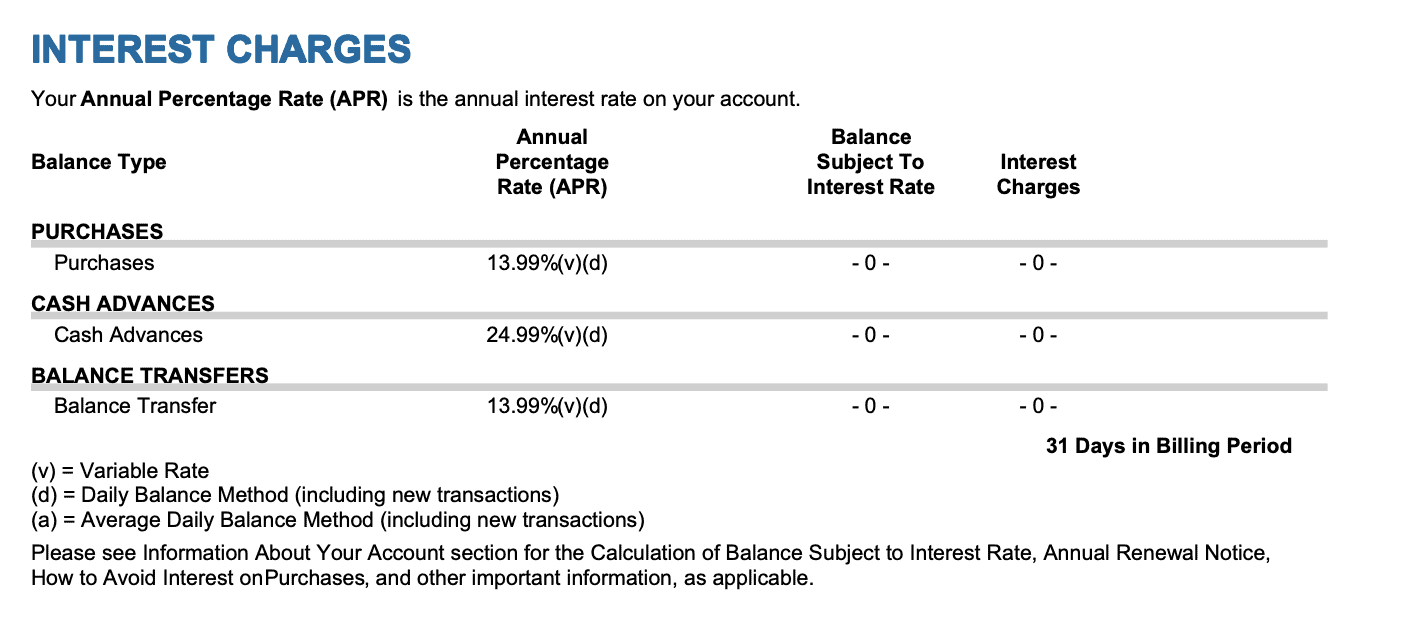

- Fixed / Avg Interest Rate. You’ll want to use your APR (annual percentage rate). For most debts, this will typically be found on the statement itself. For debts with variable interest rates, use today’s rate (not what it will be in the future) and continuously update the spreadsheet when your rates change.

- Minimum Payment. This is important because it determines how much of each month’s payment is going towards your debt’s principal, and how much is going towards interest.

- Custom Order. This optional column allows you to manually determine the order in which you’d like to pay off your debts. Most of the time, you should leave this blank. But it can come in handy in certain situations, like when you want to build an emergency fund.

- Interest-only Amount. After entering your debt information, this column will show you the amount of interest you’re paying based on the debt’s balance and minimum monthly payment.

If you’re not sure of this information, the best place to grab it from is your credit report, which you can get for free using AnnualCreditReport.com. The goal here is to determine, as of today, what your total principal and interest will be.

In addition, you’ll also choose between the debt snowball and avalanche methods (more on that below).

Getting Your Debt Payoff Date

After you insert the information and click on your preferred debt payoff method, you’ll see at the top the number of months it takes you to become debt free.

The number of months until you’re debt-free is the number you’ll want to constantly keep in mind. More importantly, it’s what you’ll constantly want to track — and ideally, watch go down over time.

We’ll get into more detail about how to make this number go down faster later in this article.

Picking Between the Debt Snowball and Debt Avalanche Methods

If you’re unfamiliar with the debt snowball and debt avalanche methods, here’s what you need to know:

- The Debt Snowball. Pay off your debts starting with the smallest balance first.

- The Debt Avalanche. Pay off your debts starting with the highest interest rate first.

The debt avalanche method will save you the most money overall, because you’re eliminating the debts with the highest interest rate first. This is the method the math geeks love, because it makes the most sense from a numbers perspective.

But the debt snowball method is the approach the behavioral science community loves, because it helps you build momentum by achieving small wins upfront. That momentum increases motivation and can help people see their debt payoff plan through to conclusion.

It may not save quite as much money in the long run, but it’s a heck of a lot better than doing nothing.

What does the research say?

A study from Northwestern University found that the debt snowball works best for those with multiple credit card debts. And the results were duplicated in a separate study published in the Journal of Consumer Research.

In short, the behavior side seems to win out. And in most cases, I feel it’s the right way to go.

Of course, everyone has a different situation. So be smart. Run the numbers yourself and do what makes sense for you. If your rational, numbers-based brain is going to constantly question why you’re paying off small balances with low interest rates, opt for the avalanche.

But if you find your debt to be overwhelming and hardly know where to start, the small wins you’ll get with the snowball method might be just what you need to get moving down the right path.

Ultimately, what matters most is not which approach you choose; it’s that you pick one, commit to it, and stick with it until your debt-free day.

Should You Create an Emergency Fund Before Paying Off Your Debt?

The time it takes to build an emergency fund is time that allows your debts to compound. So there’s a high cost to building an emergency fund while you’re burdened with high-interest debt.

At the same time, having no cushion can lead to more debt trouble if something goes wrong in your life, like a sickness, a pay cut or a job loss.

Plus, the lack of a safety net means that minor setbacks, like an unexpected car repair, can balloon into major problems.

Your goal should be to have the minimum effective dose: an emergency fund that contains the smallest amount of money necessary to avoid digging yourself deeper into debt.

Studies from the non-profit group AmericanSaves.org suggest that number is $500. And that makes a lot of sense, because $500 is enough to cover many of the most common unexpected expenses.

And most importantly, it’s an amount you can build up quickly — enabling you to start paying off your debts ASAP.

If you’d like to incorporate the time it takes you to build an emergency fund into your debt payoff date, insert “Emergency Fund” as a creditor in the spreadsheet, as shown below.

Step #2: Create Tight Feedback Loops and Accountability

Once you’ve determined your debt payoff date, you’re ready to move on to Step #2.

And by the way, congratulations are in order. Most people have no idea how much debt they have, let alone the exact month they’re going to pay it off.

In this step, you’re going to take two actions:

- Create feedback loops.

- Hold yourself accountable.

Creating Feedback Loops

Feedback loops are a concept from systems design. They’re useful because they allow you to constantly correct your course based on new information.

One example of a feedback loop is a thermostat. When the temperature in a house goes down to a certain point, the thermostat automatically turns on the heat. Once the temperature in the house rises, the thermostat recognizes this and turns the heat back off.

The system is constantly measuring and adjusting in order to reach the desired output.

In Phase #2 of the previously-mentioned study (Borrow Less Tomorrow: Behavioral Approaches to Debt Reduction), researchers had participants set monthly text and email reminders — i.e., feedback loops — related to their debt payoff goals.

In doing so, participants were reminding themselves to check whether they were on track to meet their goals (and to correct course if needed).

This is exactly what you’re going to do today.

Set a recurring reminder to recalculate your expected debt-free date.

The more often you calculate this number, the more it allows you to recalibrate. As such, I would set a weekly reminder.

As you’ll see below, you can accomplish a lot inside of a week. And, in doing so, you’ll see and be encouraged by the progress you’ve made.

At this point, you have two sources of positive momentum: you’re seeing your debt balances go down and you’re seeing your expected debt payoff date move up.

Hold Yourself Accountable

The third phase of the Boston College study was to find an accountability partner. Participants were advised to tell at least one friend about their debt payoff goal. And furthermore, that person was given instructions about how to hold them accountable if they got off-track (which was through text and email reminders).

If you’re in a relationship, this can be your spouse. Reminders can be as simple as one person calculating the debt payoff date each week, then texting the date to their spouse.

If you’re not in a relationship, have a parent, sibling or close friend hold you accountable.

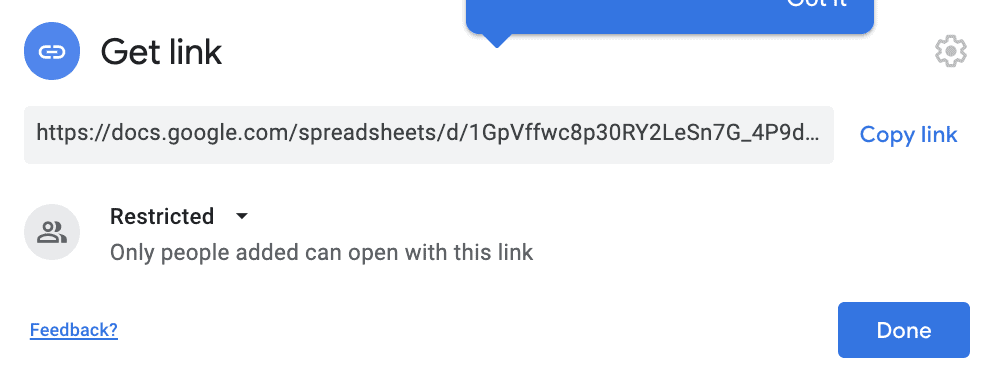

Pro Tip: Share your debt payoff calculator by selecting “Share” in the upper right-hand corner, making sure to select “Restricted” — which means only those whose email you add can get access.

Step #3: Lower Your Monthly Expenses

This is where things get fun. Because when you take the right actions, you can quickly improve your debt payoff date.

And all of a sudden, in one week you’ve decreased your debt-free date by months. And that incredible momentum feels great.

What does the research say about saving money?

Track Your Spending

Tracking your spending is oft-repeated advice for one reason: it works.

One study showed that those who tracked their expenses via a budgeting app saved 15.7% on average.

Fortunately, this has never been easier. There are plenty of great, easy-to-use budgeting apps available today. And many of them are either free or very low cost.

Learn more: Read our ranking of the best budgeting apps.

Reduce Your Monthly Fixed Costs

The easiest expenses to cut are the ones you can shop for and negotiate. Often, a phone call or two can knock hundreds of dollars from your monthly budget — and, subsequently, months off of your debt-free date.

Your options are to negotiate down, find a new provider, or flat-out cancel.

Some of the best bills to cut include:

- Car and home insurance

- Cell phone service

- Cable, TV and internet

Some states even allow you to shop and compare different utility providers.

What you’re looking for here are quick wins. If there’s a way you can save money fast — some relatively easy action that takes less than 24 hours — now is the time to seize that opportunity.

Change Your Environment to Change Your Behavior

You can save a lot of money when you set aside a day to shop for, negotiate, and cut your monthly fixed costs. However, we all have certain discretionary expense categories that give us the most trouble.

These are expenses like entertainment, alcohol, eating out and online shopping — categories where, if we’re not careful, our spending habits will quickly cancel out an entire month of frugal living.

So what’s the best approach when it comes to these types of expenses?

What’s important to recognize is that these purchases are usually habitual. And the thing about habits is that they’re easy to form but near impossible to break.

Dr. B.J. Fogg, Director of Stanford Persuasive Lab, has a quote that’s worth repeating when it comes to habit change:

“There’s just one way to radically change your behavior: radically change your environment.”

What you’re trying to identify here are specific actions you can take today that will prevent bad behavior, while also encouraging good behavior in the future.

As an example, if you were trying to lose weight, one action would be to throw away any unhealthy snacks you have in your pantry.

Want to limit credit card spending? Place your credit cards into a safe. The extra time it takes to take them out will typically make you think twice about a purchase.

Going out to a bar? Bring your ID and cash only.

Can’t stop shopping online? Delete your saved credit cards so that you have to manually input the info every time you want to make a purchase.

Overspending at the grocery store? Use the envelope budgeting method.

Step #4: Make More Money

Cutting costs certainly helps reduce the time it takes to pay off your debt. However, you’ll eventually hit the limit of how much you can save without dramatically impacting your lifestyle.

On the other side of the debt payoff equation is making money. And that’s where you’ll find the most potential for speeding things up.

Your goal is to grow the gap between your income and expenses as large as possible. The larger the gap — and thus the more money that goes towards debt repayment — the faster you’ll get out of debt.

Making money is a skill that takes practice. So if you’ve never made a single dollar outside of your job, diving headfirst into a new business with a lot of startup costs isn’t ideal.

Instead, you need to build your skills. And if making an extra $100 this month would be a stretch, that’s perfectly OK. What’s important is recognizing where you’re at today and putting in place a strategy to help build your money-making skills to a higher level. If that means going from $0 to $50, that’s great.

Thinking long-term is also important here. Yes, $50 might not seem like much — and it may not make much of a dent this month. But the idea is to develop these skills over time.

Perhaps in six months you’ll have gone from $50 per month to $1,000. Perhaps in two years, you’ll have a side hustle that’s making you as much as your job.

If You Wouldn’t Buy It Today… Sell It

The easiest way to start building your money-making skills is by selling items you already own.

As a rule of thumb, you should liquidate anything you own that you wouldn’t buy again today for the price you can sell it for.

For the quickest results, sell stuff locally on sites like Craigslist. For rare, collectible or higher-end items, you may be better off using a site like eBay, which has a global market.

Find a Higher Paying Job

Put in place a strategy to start earning more with your primary source of income. One study showed that employees who stay in their job longer than two years are paid 50% less.

Finding a higher paying job may take three to six months to accomplish. However, the results are worth it. A higher paying job is often the highest-leverage point for paying off debt and building long-term wealth.

As such, maximizing your earning potential is a skill worth developing.

Start a Side Gig

Another high-leverage activity you can and should use to pay off your debts is finding ways to make money outside of your job — i.e., a side hustle.

Not only can the money be put directly towards paying off debt, you’re also building valuable skills.

And it’s these types of skills that can help you:

- Make more money from your full-time job.

- Have a secondary source of income to fall back on in case something happens with your full-time job.

- Develop the skills that can eventually lead you to start a profitable business of your own.

When it comes to that last point, the sky’s the limit. Because a business can be scaled, your earnings are not tied to the number of hours you put in.

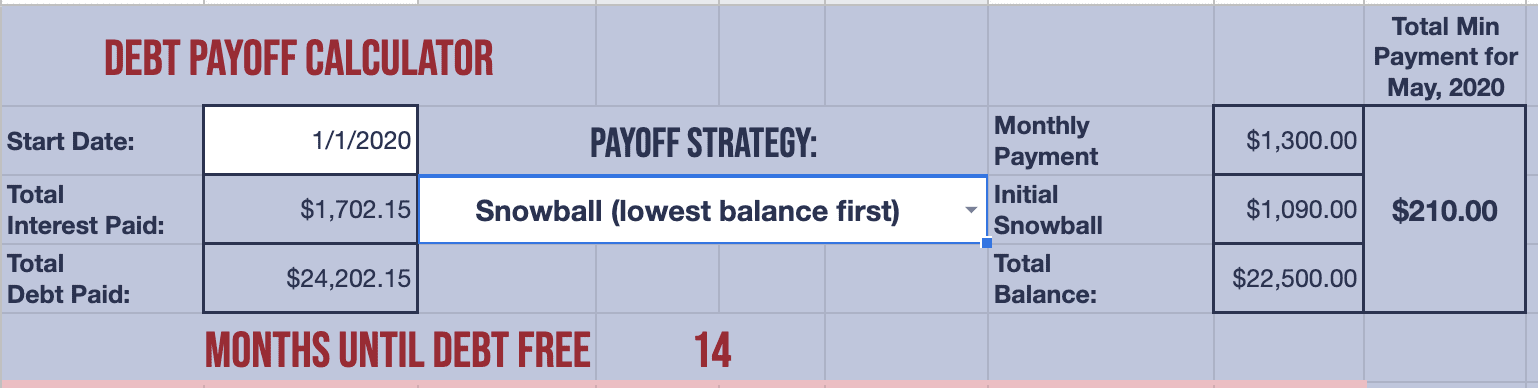

Don’t underestimate the power of earning more money. In the demo spreadsheet, when you increase your income from $5,000 per month to $5,500, you reduce the time it takes to pay down the debt from 27 to 14 months.

Getting Out of Debt FAQ

Here are answers to a few of the most common questions we get from readers about debt payoff strategies. If you’re wondering about something we didn’t touch on in the article, feel free to send us an email or leave a comment below.

The answer to this question depends on many factors, including your credit score, the interest rates on your current credit card debt, the amount of debt you have, and how quickly you’ll be able to pay off the transferred balance.

If you have poor credit, the answer is probably “no,” because you would need to qualify for a balance transfer card with a lower rate than you’re currently paying. On the other hand, if you have good credit and are simply struggling to pay down your balances, a transfer may be a wise option.

As with balance transfer cards, whether or not a loan makes sense depends on a variety of factors and your personal financial situation.

If you’re able to refinance your debt to a lower interest rate than you’re currently paying, a loan may be able to save you money and help you reach your debt-free date faster.

As always, the devil is in the details. If your debt consolidation loan has a lengthy repayment duration or very low minimum payments, it’s possible that you could end up paying more over the lifetime of the loan — even with a lower rate.

Before taking this type of loan, make sure to use our free calculator to calculate your total costs and payoff dates in both scenarios.

Final Thoughts on Getting Out of Debt

For long-term readers, what may come as a surprise is that the same concepts that apply to paying off debt also apply to getting rich.

What’s true is that your ability to accurately measure your finances, set goals, save meaningful money and increase your income are quite useful whether you’re in debt or not.

So, think of your debt payoff journey as a chance to flex that financial muscle and to gain the skills needed to create the type of wealth you’re after in life.

On your google spreadsheet, the total min payment for the month breaks if you change the start date to the current date. Is there a way to fix it?

Hey Curtis,

Can you send a screenshot to my email at rj@thewaysotwealth.com.

I’m not getting the error.

Hi, was this ever resolved? I’m getting the same issue.

Thanks,

Ashley

Hey Ashley,

Can you send a screenshot to my email at rj@thewaysotwealth.com.

I’m not getting this error. Thanks!