Many homeowners want to pay off their mortgage early. The proven ways to do this are straightforward: make extra principal payments, refinance into a shorter term, or recast after a lump sum.

A newer strategy called velocity banking has started to attract attention.

Promoters sometimes claim it can reduce a 30-year mortgage to as little as five to seven years.

As a CFP® who has evaluated mortgage payoff strategies for years, my goal here is to explain how velocity banking actually works, where the math holds up, where it breaks down, and how it compares to simpler, proven alternatives.

Key Takeaways

- The savings come from extra payments, not the HELOC. Velocity banking only works because you’re paying more principal earlier. The HELOC itself doesn’t create savings and often adds cost and risk.

- It only works if conditions stay favorable.The HELOC rate must remain lower than your mortgage rate — and today, HELOC rates are usually higher. Cash flow has to stay strong, and fees can’t eat away the benefit. Even then, if mortgage rates drop below your HELOC rate, you’d likely be better off refinancing your mortgage outright instead of juggling debt between two loans!

- The risks are real. HELOCs have variable rates that can rise quickly, be reduced, or even frozen. Using them adds complexity and exposes you to interest-rate and liquidity risk.

- Simpler strategies are usually better. Making extra principal payments, refinancing to a shorter term, or recasting your loan typically achieve the same payoff speed with less risk and complexity.

- Only a narrow group may benefit. Velocity banking may help a disciplined, high-income homeowner with strong cash flow, a favorable rate gap, and plenty of equity. But those factors must hold steady throughout each HELOC cycle, and much of that is outside your control. You can stop the strategy at any point, but if rates rise or cash flow drops while you still have a HELOC balance, the costs can outweigh any benefit.

- Times have changed. Back in 2021, when many of the viral velocity banking videos were created, interest rates were historically low and many households still had older mortgages with rates around 5 percent. In that environment, a HELOC could temporarily look cheaper, which made velocity banking seem far more appealing than it is today.

Velocity Banking Strategy Explained

The concept is called “velocity banking” because it aims to increase the speed of mortgage payoff.

Velocity banking does this by using a home equity line of credit (HELOC) to make large lump-sum payments toward the mortgage principal. Instead of paying the loan down only through the regular monthly schedule, you shift debt between the mortgage and the HELOC while using your income and expenses to manage the balances.

Here’s how it generally works:

- Step 1: Open a home equity line of credit (HELOC).

- Step 2: Use the HELOC funds to make a lump-sum payment toward your mortgage principal. This replaces a portion of the mortgage debt with HELOC debt.

- Step 3: Deposit your paychecks into the HELOC. Because HELOC interest is usually calculated daily on the outstanding balance, depositing income reduces the balance and lowers interest charges.

- Step 4: Some versions of the strategy use a credit card to cover living expenses during the month. The idea is to take advantage of the card’s grace period, which delays payment until the bill is due and allows more of your income to sit in the HELOC reducing interest. This step is optional and often used to show maximum benefit, but it also increases risk because a single mistake can create high-interest credit card debt.

- Step 5: At the end of the month, you use the HELOC to make your regular monthly mortgage payment. If you’re using a credit card for living expenses, you also pay off the card balance in full from the HELOC at this time.

- Step 6: Repeat the cycle. With positive monthly cash flow, the HELOC balance gradually decreases. Once it reaches zero, you can make another large payment from the HELOC to the mortgage and begin again.

Over time, this cycle is repeated until the mortgage is paid off, leaving only the HELOC balance to clear.

Once that’s paid down, the home is owned free and clear.

To use the strategy, you typically need:

- Enough equity to qualify for a HELOC — most lenders limit the combined loan-to-value ratio to roughly 78% to 82%, depending on credit and underwriting.

- A solid credit score, usually 680 or higher, with many lenders preferring 700 or more.

- Positive monthly cash flow, meaning your income reliably exceeds expenses.

- In some versions, a credit card is used for living expenses to maximize the flow of income into the HELOC.

Having more equity can allow for a larger line of credit, which makes it possible to make bigger lump-sum payments toward the mortgage.

Why Try Velocity Banking?

When you take out a 30-year mortgage, the payments stay the same each month, but the way they’re applied changes over time. In the early years, most of your payment goes toward interest and only a small part reduces the loan balance.

It can take well over a decade before more of your monthly payment goes to principal than interest.

Velocity banking tries to speed this up.

The idea is to move part of your mortgage balance into a HELOC — which uses simple interest calculated daily — and then pay that HELOC down quickly with your income.

By using the HELOC to make large lump-sum payments toward your mortgage, you shrink the mortgage balance faster.

That means future mortgage payments apply more to principal sooner, instead of waiting years for the normal amortization schedule to flip.

The table below shows what happens during the first five years of a $400,000 mortgage at 6% interest. It highlights why progress is slow in the beginning: the interest portion dominates the payment.

| Payment Number | Total Payment | Principal Payment | Interest Payment |

| 1 | $2,398.20 | $398.20 | $2,000.00 |

| 12 (Year 1) | $2,398.20 | $420.66 | $1,977.54 |

| 24 (Year 2) | $2,398.20 | $446.60 | $1,951.60 |

| 36 (Year 3) | $2,398.20 | $474.15 | $1,924.05 |

| 48 (Year 4) | $2,398.20 | $503.39 | $1,894.81 |

| 60 (Year 5) | $2,398.20 | $534.44 | $1,863.76 |

As the loan matures, a larger share of each payment gradually shifts from interest to principal. It takes many years before this becomes significant, as shown in the table below:

| Payment Number | Total Payment | Principal Payment | Interest Payment |

| 120 (Year 10) | $2,398.20 | $720.88 | $1,677.32 |

| 180 (Year 15) | $2,398.20 | $972.36 | $1,425.84 |

| 240 (Year 20) | $2,398.20 | $1,311.57 | $1,086.63 |

| 300 (Year 25) | $2,398.20 | $1,769.11 | $629.09 |

| 360 (Year 30) | $2,398.20 | $2,386.27 | $11.93 |

On paper, velocity banking tries to accelerate this shift by using lump-sum payments from a HELOC to reduce the mortgage balance faster. The quicker the balance goes down, the less you end up paying in interest overall.

Velocity Banking Example

To see how velocity banking works in practice, let’s walk through an example with the following assumptions:

- Original mortgage: $400,000 at 6% for 30 years

- Monthly payment: $2,398.20

- HELOC “chunk” amount: $20,000 at 8% interest

- Home value: $500,000

- Monthly income (after tax): $10,000

- Monthly expenses: $8,000

- Free cash flow: $2,000 per month

Here’s the process:

- Draw from the HELOC. You borrow $20,000 from the HELOC and apply it directly to your mortgage. The mortgage balance drops to $380,000, and the HELOC balance is $20,000.

- Deposit income into the HELOC. Each month you deposit your $10,000 paycheck into the HELOC. That temporarily lowers the balance.

- Cover expenses. You spend $8,000 on living costs. Some people run these through a credit card to maximize the float (see note below), then pay it off in full from the HELOC at month-end. Either way, your HELOC ends the month at $18,000 ($20,000 – $10,000 + $8,000).

- Apply surplus cash flow. Because you consistently have $2,000 left over each month, the HELOC balance shrinks by about $2,000 monthly. After 10 months, the HELOC is back to $0.

- Repeat. At that point you can take another $20,000 HELOC draw, apply it to the mortgage, and restart the cycle.

Meanwhile, you still make your regular $2,398.20 mortgage payment each month, which reduces the balance alongside the “chunk” payments.

Some velocity banking examples show higher savings because they run all monthly expenses through a credit card. This allows income to sit in the HELOC longer and reduces interest slightly. It is true that this lowers interest a little because HELOCs calculate interest daily. However, this benefit is not unique to velocity banking. Anyone can use a credit card float while making extra mortgage payments. The effect also saves only a small amount each month, so it should not be treated as a major advantage of the strategy.

How much does velocity banking save you?

Promoters often say velocity banking can save you hundreds of thousands in mortgage interest.

But that framing is misleading.

The “savings” don’t come from the HELOC itself. They come from applying extra money to your mortgage principal earlier than scheduled.

If you have $2,000 in surplus cash flow every month, the real question is: does velocity banking beat simply applying that $2,000 directly to your mortgage?

Velocity Banking vs. Extra Payments: Side-by-Side Comparison

Assumptions used: $400,000 mortgage at 6% for 30 years. Monthly payment $2,398.20. HELOC chunks of $20,000 at 8%. $2,000 monthly surplus cash flow.

| Strategy | Time to pay off | Total interest paid |

| Standard mortgage (no extra) | 30 years | $463,352.76 |

| Velocity banking (with HELOC) | 10 years | $134,487.76 |

| Extra $2,000/mo directly to mortgage | 10 years 2 months | $134,816.58 |

Assumptions:

No velocity banking example can provide an exact estimate of savings becasue many factors are unknown.

But, for the purposes of this example, the following assumptions were made:

- I assumed fixed rates and consistent monthly cash flow. Of course, HELOCs have variable rates that can rise or fall quickly.

- These are illustrations, not guarantees. The point is to show that velocity banking offers very little advantage once you strip away the marketing spin.

The takeaway: In this example, velocity banking saves only about $328 compared to simply making extra principal payments. That’s essentially a rounding error once you factor in the added risks, fees, and moving parts of using a HELOC. If interest rates fell and you had a large mortgage balance, refinancing would usually be a better option. If HELOC rates rose, the strategy could cost you money. The good news is you’re not locked in forever, you can abandon velocity banking after paying off a HELOC draw and simply go back to making extra payments directly. The downside is that the timing of when you exit matters: if you’re caught with a big HELOC balance when rates spike, the cost of the experiment could be significant.

Why Popular Velocity Banking Videos Get the Math Wrong

A lot of viral videos promise huge savings using velocity banking.

When you look closely at how they build those examples, the numbers often do not hold up.

Here are the most common mistakes I found that cause their results to look much better than what most homeowners can expect in real life.

1. Ignoring how variable HELOC interest rates work

Most videos assume the HELOC rate stays low and steady. HELOCs are variable-rate loans that can rise quickly, especially in changing rate environments.

If the HELOC rate climbs above the mortgage rate, the strategy can flip from small “savings” to “more expensive” very fast. None of this risk is usually factored into their examples.

2. Assuming everyone has large, consistent free cash flow

Most examples use unusually high monthly cash flow in order to pay down each HELOC draw in six to ten months.

In reality, many households do not have that kind of leftover money each month.

Rising home prices, higher insurance costs, inflation in everyday expenses, and other debt obligations like student loans make it harder to maintain the steady surplus that these examples depend on.

Even small changes in cash flow can slow the strategy down significantly.

3. Treating a HELOC draw as “free money”

This is one of the most misleading parts of many velocity banking examples. Some videos compare a HELOC lump-sum payment to doing nothing at all. Of course the numbers look impressive when you compare paying down your mortgage to not making any extra payments. That comparison does not tell you anything useful.

The fair comparison is simple. What would happen if you took the same cash flow you plan to use to pay down the HELOC and instead made regular extra payments directly to your mortgage? When you compare those two options side by side, the results are usually almost identical, and you avoid the extra risk and complexity of carrying a variable-rate HELOC balance. The strategy only looks magical when you compare it to “doing nothing,” which is not how real people manage their mortgages.

4. Using outdated interest rate environments

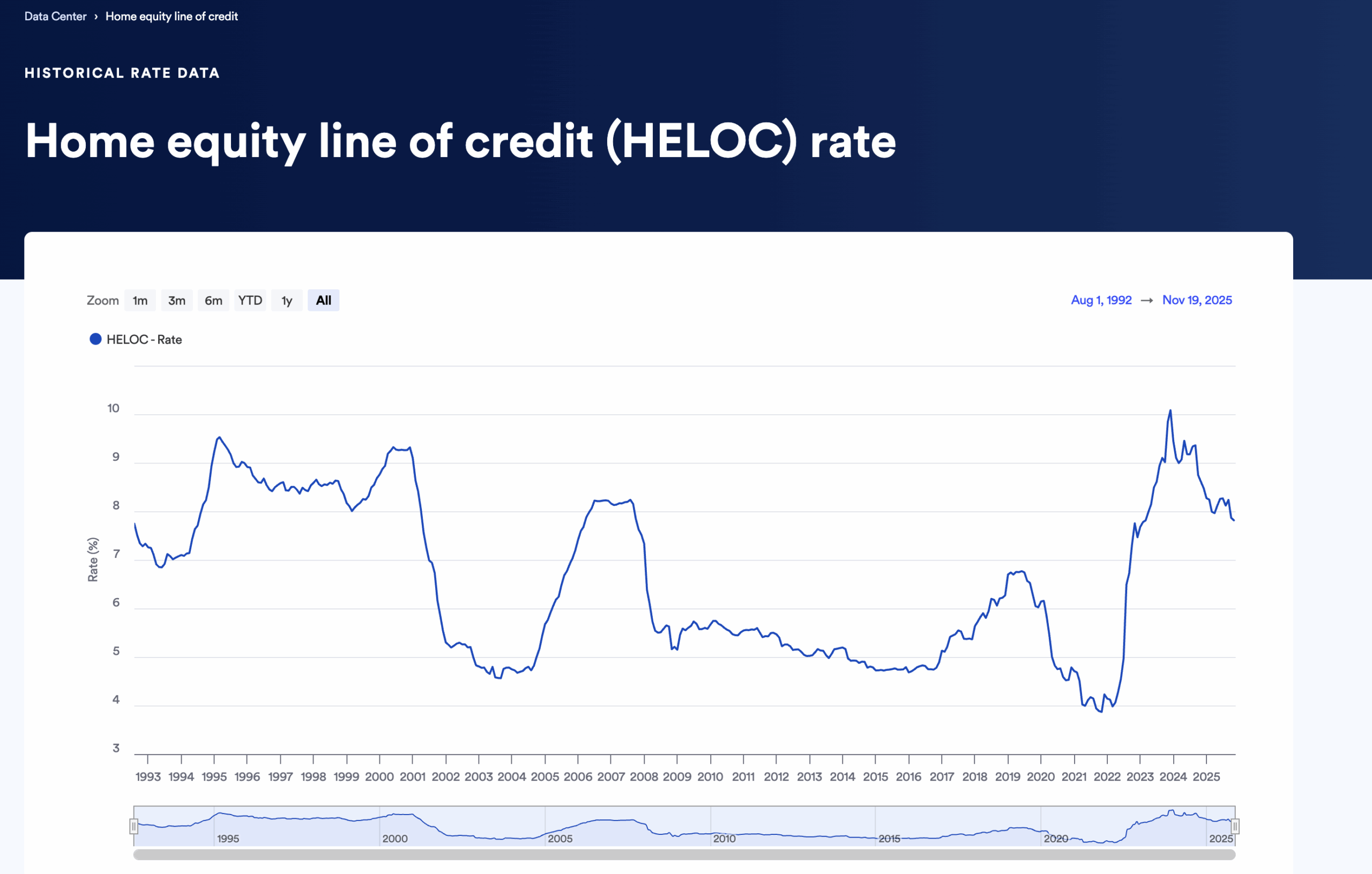

Many of the most popular velocity banking videos come from around 2021. That period was unusual. Mortgage rates had fallen to all-time lows because of the pandemic, yet a lot of homeowners were still carrying older mortgages in the four to six percent range from before the rate crash. At the same time, HELOC rates had not fully caught up and were often cheaper than those older fixed mortgages.

That one window in time created the perfect setup for velocity banking examples. The math looked much better because people were comparing a low-rate HELOC against a higher-rate mortgage they already had.

That is not the environment we live in today.

Fixed mortgage rates are now lower for most existing homeowners because millions of people locked in three to four percent loans. HELOC rates, on the other hand, are significantly higher and adjust with market conditions.

Here’s what HELOC rates have changed overtime according to Bankrate.

In most normal environments, a fixed mortgage is cheaper than a HELOC, and the gap is now larger than ever.

This changes the entire equation!

When your mortgage rate is three percent and your HELOC rate is eight percent, the opportunity cost of aggressively paying down that mortgage becomes much harder to justify.

Will Velocity Banking Actually Work for You?

By this point you’ve seen how velocity banking works and where most examples fall apart. For a small number of households, the math can work under very specific conditions.

These situations are rare, but if you believe you might be one of them, here are the questions that matter most.

Question #1: How much positive cash flow do you have?

If you only have a small amount of excess cash left over each month, velocity banking will not speed up the process very much and it will probably be more hassle (and more expensive) than it’s worth.

Question #2: Is paying off your mortgage ahead of schedule your best long-term financial move?

So far we’ve been looking at this topic from the perspective of attempting to pay off your mortgage as fast as possible. But it’s important to determine if that’s actually in your best interest.

There are a number of reasons to pay off a mortgage. Aside from the financial benefit of being debt-free, eliminating the monthly mortgage payment can help to reduce stress and anxiety related to money.

However, on paper it usually makes more sense to pay your mortgage on schedule and use any extra money to save and invest. The interest rates on mortgages are typically low, and for some people there will also be tax benefits.

Question #3: What is the interest rate of the HELOC?

The interest rate on a HELOC will typically be higher than the rate on a first mortgage. The amortization and calculation of a HELOC will be different than a mortgage, so it’s not comparing apples to apples, but the higher the interest rate on the HELOC, the less likely that velocity banking will be effective for you.

Question #4: Is the HELOC rate fixed?

Most HELOCs have a variable interest rate, which could increase at any time. If you get started with velocity banking and your interest rate goes up, it will throw off your calculations and require more time to pay off the debt.

Question #5: What are the additional costs associated with your HELOC?

According to the Consumer Financial Protection Bureau (CFPB), HELOCs often come with several common fees you’ll want to account for before starting a velocity banking strategy. These may include:

- Conversion fee if you switch a portion of the balance to a fixed rate

- Application fee

- Origination, appraisal, title, or other closing costs

- Annual or membership fee

- Inactivity fee for not using the HELOC

- Early termination or cancellation fee (usually in the first 2–3 years)

Question #6: What are your other sources of emergency funds?

This will not be relevant for everyone, but some people use a HELOC as an emergency fund. If that’s your approach, you’ll need to consider what will happen if your HELOC is maxed out and an emergency arises.

Velocity Banking Alternatives

Here are some other options you can consider if velocity banking is not right for you:

- Make extra payments as you’re able. You can pay extra on your mortgage at any time and it will be used to pay down the principal. If you pay extra each month (or whenever you’re able), it can make a real difference.

- Bi-weekly payments. Another common “trick” for paying off your mortgage early is to make payments every two weeks instead of every month. You’ll make 26 payments throughout the year, equaling 13 months’ worth of payments. That extra payment will go towards the principal and allow you to cut about two or three years off of a 30-year mortgage. It’s nothing drastic, but it’s an easy way to have an impact.

- 15-year mortgage. If you’re just buying a house now (or refinancing), you can opt for a shorter term, like a 15-year mortgage. It will increase your monthly payment, but you’ll save a huge amount of money in interest and a much larger percentage of your monthly payment will start going towards the principal right away.

- Pay on schedule. Of course, another option is to not pay your mortgage off early and use the extra money for other purposes, such as investing.

Velocity Banking FAQs

Yes, it’s possible to implement the strategy by using a credit card and balance transfers instead of using a HELOC. However, it adds a little bit of complexity and it may require you to churn credit cards and move from a card before its 0% introductory rate expires. It also increases the need for discipline to avoid high-interest debt on the credit card.

No, the two concepts are different. Infinite banking involves using life insurance policies that pay dividends with the goal of essentially becoming your own banker by borrowing against the cash value of the policy. Read our critique of infinite banking to learn more.

Dave Ramsey is not a fan of the concept, and more specifically, he’s not a fan of the people and companies trying to sell software or a service that will help you with velocity banking.

“If you want to pay extra payments on your first mortgage, you have to live on less than you make. If you borrow money on the home equity line of credit to pay money down on the first, you broke even, didn’t you? That’s borrowing from Peter to pay Paul,” Ramsey says. “That’s stupid. What they’re saying is that they’re going to assist you in managing your money better, and they’re going to charge you $3,500 for all this gyration. It’s a bunch of crap.” (Source.)

The Bottom Line on Velocity Banking

If your goal is to pay off your mortgage faster, the safest and most reliable approach is to make direct extra principal payments. The math is simple, the risk is low, and the results are predictable.

Velocity banking, on the other hand, only works under narrow conditions and depends on a long list of assumptions. It requires consistent positive cash flow every month, no income disruptions, and a HELOC rate that behaves exactly the way you expect.

Real life rarely works that neatly.

If anything goes wrong, you could end up carrying higher-interest HELOC debt instead of a lower-rate mortgage.

When that risk is included, the small theoretical advantage the strategy sometimes shows becomes far less meaningful.

The bottom line is that the numbers do not support velocity banking for most households. Extra principal payments give you almost the same benefit without the complexity, costs, or risk.

Excellent analysis on the velocity banking. Fair and objective. Thank you Marc.

Your analysis, pros, cons, and alternatives were crisp, to the point, and saved me from listening to a breathless infomercial about the subject.

Thank You,

Steven G

Thanks Steven!

Very good explanation without bias. In everything I read so far, you can see their personal opinion. Thank you!

This was the best article I’ve read in three hours on the pros, cons and explanation of the strategy… now, to decide. I want to pay off high interest rate debt before my mortgage. I’m assuming it works the same way. Pay a chunk of debt. Pay it back by using the HELOC as a checking account until you get it down to a good balance again. Then pay a chunk of debt. hmmm.

Hey Jodi,

My two cents: taking out a HELOC could make sense depending on the amount of credit card debt. Just make sure to account for interest and fees on the HELOC. If it’s not too much debt, I’d just pay it off without the HELOC.

I then wouldn’t mess with velocity banking. It takes years and a 100% repayment schedule to make the strategy even worth considering. Seeing that you’re currently in high-interest debt, my focus would be more along the lines of the baby steps (https://www.thewaystowealth.com/dave-ramseys-baby-steps/). Establish an emergency fund, start funding investing accounts, etc.

This is an Excellent article! It describes the concepts, the requirements for using these concepts and the pros/cons. All other articles I’ve read go straight for the hype and present a happy day scenario without dealing with all the must haves in order to make it work and the Pros/Cons. In addition the author presents alternative ways of accomplishing the same goals. Very thorough!

Thanks William!

Your explanation about Velocity banking, is the best that I read so far!

Thank you!

Wow, very concise appraisal of velocity banking. Probably the best I have read. No personal bias and BS just the facts. I don’t have much more input but wanted to compliment you on a very good article. Thank you.

Really appreciate the kind words. Thanks.

This article is good, but is missing one more option! Taking out a PLOC of say $10,000.00 (Personal Line of Credit) would be a better approach. Applying the principles you discussed and avoiding HELOC’s variable interest rates is a win/win in my book. Also, don’t forget to mention the REAL interest rates people are paying. First, it’s not SIMPLE interest, like you get with a credit card, and secondly, the REAL interest on a mortgage can be found in the “Closing Documents” of that mortgage. For some loans, it can be as high as 80%

Thanks. Math is going to be a bit different, however, as PLOCs are going to have higher interest rates than HELOCs.

A quick search found that the US Bank has a HELOC of as low as 8.95%, while the lowest PLOC going is 12.5%.

Which is still lower than the REAL interest rate on the mortgage right or wrong?

How are you calculating the real interest rate? The term is typically used when discussing impacts of inflation on a loan.

And how is this different from APR, which reflects the true cost of borrowing on an annual basis.

Thank you for clearing my head on this complicated concept for me. I will stick to what I have been doing, paying extra to my principal when I can.

Is there a significant difference between this heloc strategy and simply paying the available cashflow you would use to paydown the heloc towards your mortgage?

Yes, because more of your payment goes toward the principal instead of interest. But, as discussed, this has its risks as well.

Using your example numbers of a $200,000 mortgage balance, a 3.5% interest rate on the mortgage, 30 years remaining on the term, and $1,000 positive cash flow per month.

If you put that $1,000 every month on the principal, you pay it off in 10 years and 7 months. Total interest of $39,310.37 vs. no additional principal of $123,312.18, which crushes your 17K in savings and 12 and change years.

You’re right. I’m just not sure what were the variables in the calculator we used at the time, as it’s no longer available to double check our work. We’ll need to take a deeper dive into this!

I’m sorry what? The example says the $1000 in positive cash flow will pay the 20k HELOC balance off in 20 months. Then you’re supposed to rinse and repeat. What about the HELOC interest you’ve been accumulating?

Thanks, JB, for pointing this out. Sorry, if you read that and stopped in your tracks, because you’re right, that example doesn’t include interest!

That was to just conceptualize the general idea.

We go on to talk below about the variables below that are going to impact the duration to pay off the HELOC and mortgage.

Very good article. Thank you for articulating this method so clearly.

Instead of the chunk payment, you could just pay $1000/month on top of the normal mortgage payment. This isn’t as efficient as the chunk payment, but the difference is small enough that it is worth the ease of execution, cashflow flexibility for unexpected expenses, and preserves the HELOC for other outlier needs.

I found this article after watching a YouTube video on the same topic. Your explanation and breakdown was easier to understand and I like that you also provided the pros and cons. One thing neither of you mentioned, however, is the draw period when only interest-only payments can be made toward the HELOC. In such a scenario, this method is pointless because those 20 payments would go to the interest only, leaving you with the full principal balance once the draw period ends, which can be several years later…Am I wrong in this assumption?

Good question Belle.

During the HELOC draw period, most lenders only require interest-only payments on the amount borrowed. However, you have the option to pay more than the minimum payment, which would include payments towards the principal balance.

In the context of the velocity banking strategy, the whole idea is to use the HELOC to pay down the mortgage principal faster by making large, lump-sum payments. If you only make the minimum interest-only payments during the draw period, you won’t be making any progress on paying down the principal, which defeats the purpose of velocity banking.

Does that make sense?

We have equity, a positive cash flow and credit score of 800. We also have zero credit card debt. We are 13 years into the mortgage and interest and principal are now 50/50. We took a HELOC in 2021 for a new kitchen and owe $65K on it. Is there any value in getting a PLOC to try this velocity banking to knock out the HELOC? We have a $2K/mo positive cash flow.

What are the terms of the HELOC? Interest rates were low in 2021. Is it variable?

But overall, I would advise most against taking out a personal line of credit to pay off a HELOC. Personal lines of credit typically have much higher interest rates than HELOCs.

And I just don’t love juggling around debt to try to squeeze a tiny bit of potential savings, knowing that if things go wrong, you could be stuck with more debt.

You’re doing things right as they are, and if you want to focus on the HELOC, I’d just put all your free cash flow towards it.

Yes, it’s a variable rate. The first $40K was at 3.5%, the rest was at 4.5%.

Is that what the rate is now or what it started at? That’s good.

But even if the rate was much higher, I still feel this strategy adds complexity to your financial situation and doesn’t necessarily guarantee savings or a faster payoff. Assuming the variable rates are much higher, you don’t want to lose the positive cash flow and can’t pay off the HELOC, leaving you with more debt.

I’ve yet to hear any use for Velocity Banking except when I crunch my numbers it seems like a no brainer.

I have an approx $221,000 student loan at a fixed 5.5% and I have 19.6yrs left yrs to pay off. Using an amortization calculator it would take approx 21 months to take the principle 220,000 to approx $210,000; paying approx $20,818 in interest along the way since amortized loans pay interest upfront.

My bank is offering me a 10,000 HELOC at 9.4%. If I apply that today, my loan balance instantly drops to $210,000. My HELOC calculator has me paying approx $1044/mo to payoff the HELOC in approx 10mo.

According to the heloc calc Id pay a total of $427.64 interest over that 10mo.

If I subtract the $427 interest from the heloc from the 20,818 interest from the standard monthly payment on the student loan, that saves me $20,390 in interest getting my principle down to $210,000.

However, If I simply took the same $1044/mo to principle on the original loan, my principle will be down to $210000 in only approx 7 months, but Im still paying a total of $6955 of interest over the 7 months.

Now this saves me 13,863 ($20818 – $6955) of interest compared to just making the standard monthly payment, but It seems Im still saving significantly saving by going the HELOC route. $20390 saving on interest w/ heloc – $13863 saving on interest w/extra principle payment = $6527 more by going the HELOC route plus I now have the full $10000 to repeat. Am I missing something? Thank You for your time

Hey Scott,

Your numbers check out. So, not missing anything.

But, what’s important to remember is that initially, using a HELOC to pay down your student loan will reduce the interest significantly due to the large lump-sum payment toward the principal.

However, as you continue to use this strategy, the benefits diminish.

Each new HELOC draw will offer less savings.

Eventually, applying any extra funds directly to the principal becomes more cost-effective, bypassing the HELOC.

Here’s what I’m seeing in terms of savings using velocity banking through the entire loan in your example:

Total Interest Paid: $85,089.69 (Including student loan and HELOC interest).

Time: 150 months

What do you get when you enter your student loan information in a pre-payment calculator?

I think the main point people are missing about Velocity Banking is the ability to have liquidity if something major comes up. If you put all your free cash flow into a loan, you can’t access it again. If it is in your PLOC/HELOC, you can still use it in an emergency situation. In a sense, that is your savings account as well. If you put all your free cash into a loan, you won’t have savings. If you do choose to have savings, then you are limiting how much money is used to reduce interest and bring the HELOC amount down. Also, since everything is paid from your HELOC/PLOC, when you put your income into the line, it counts as a payment for that line, meaning you won’t need an extra payment for it on top of your mortgage payment. Two birds, one stone concept—just my two cents.

I see where you’re coming from with the focus on liquidity. It’s true that having access to funds in an emergency can be reassuring, and Velocity Banking offers that through a HELOC. However, I’d caution against viewing a HELOC as a replacement for a traditional savings account. The main risk here is that you’re still dealing with debt—debt that can have variable interest rates and potentially be reduced or frozen by the lender during tough times.

While it’s tempting to use Velocity Banking to pay down your mortgage faster, it’s important to remember that this strategy requires meticulous financial discipline and hinges on several assumptions, like consistent positive cash flow and stable interest rates. And, even then, the numbers don’t always work. And, if any of those variables shift, the strategy can quickly become more costly and stressful than beneficial.

I’ve been using Velocity Banking successfully for years, and it’s allowed me to pay off multiple debts totaling more than six-figures far faster than any traditional amortization schedule ever could.

The article here is solid theory and raises valid points, but it misses the practical setup that makes VB a true wealth accelerator in real life. Here’s exactly how it works when executed properly:

The key setup most discussions overlook:

1. Link your HELOC directly to your checking account as overdraft protection (zero fees for transfers when structured this way).

2. Auto-pay every bill: – mortgage, utilities, insurance, everything – from checking.

3. As soon as your paycheck, bonuses, side income, or tax refunds hit, immediately route every surplus dollar straight to the HELOC principal.

That’s the core. You’re paying simple interest on a daily declining balance instead of decades of amortized interest.

Real results from doing this:

Paid off a $30K wedding in under a year.

Eliminated two separate vehicle loans totaling $40K, each in under a year.

Currently paying off a $75K home remodel (with fully tax deductible interest) in less than 18 months.

With traditional loans, I’d still be paying thousands in extra interest today. Instead, I paid simple interest for a short period on a shrinking balance and moved on. My next vehicle? I’ll fund it straight from the HELOC (essentially cash) and avoid amortization entirely.

The “variable rate risk” concern is real on paper, but in practice, when you’re aggressively paying down principal every month, rate fluctuations have minimal impact. The total interest paid ends up being a fraction of what amortized loans cost over time.

This only works if you have:

Positive monthly cash flow (the more surplus, the faster it goes).

Discipline to live below your means, even when the credit line looks tempting.

It’s not for everyone, and it’s definitely not reckless spending disguised as strategy. But when done right, it’s incredibly powerful.

Once my current remodel is paid off, every extra dollar is going straight toward my mortgage principal. I fully expect to own my home outright using VB in under 2 years, even though I still have 15 years left on the original 30 year loan.

Velocity Banking isn’t a gimmick when you understand the mechanics and have the discipline to execute. It’s a legitimate way to turn your income into a debt-elimination machine and build real financial flexibility.

Highly recommend testing the concept yourself before dismissing it, the numbers speak for themselves once you live it.

I think the biggest factor in what you are doing is how aggressively you are paying the balance down, and that alone changes the math in your favor. Large, consistent principal reductions will accelerate payoff under almost any structure.

My core concern, and the reason the article takes a cautious stance, is that most people do not have the level of surplus cash flow you are describing. In practice, I often see people trying to apply velocity banking with much smaller amounts, such as $1,000, $2,000, or $5,000 at a time, rather than making large, rapid paydowns. In those scenarios, the benefits shrink quickly while the risks stay the same.

When someone has strong income, steady surplus cash flow, and the discipline to pay down large chunks consistently, the strategy can work as you described. In that sense, I think your results are real and valid. I also think they reflect an exception rather than the typical outcome.

Most of the people considering velocity banking are looking for a system that works broadly, not one that requires unusually high excess cash flow to succeed. That is where I think the strategy often gets oversold.

Greatly appreciate your article and echo many of the comments regarding pros/cons and clarity of thought. I’m sure you realize just how much argument there is out there on each side and how frustrated folks seem to get with each other on this issue.

Often, when reading about this strategy/velocity banking, the discussion tends to center around the HELOC in what I presume to be the traditional “2nd” place, behind the mortgage. In that case, especially in the circumstances you mentioned where rates are equal (or in today’s case, higher for the HELOC vs. the mortgage), it can certainly become a “borrowing from Peter to pay Paul” scenario.

A question I have pertains to the 1st lien HELOC. I understand at a fundamental level that this would be different, but would you mind sharing your thoughts on how that might look specifically?

If someone is very disciplined, has excess cash flow, is willing to “paycheck park,” and actively manages the average daily balance (while carefully reviewing rates and terms ahead of time to understand how long rates last or whether part can be fixed), would the risks be any greater or worse with the HELOC in that first position?

And lastly, how would this look structurally and mathematically? If you’re not opening a “second” vehicle, what is actually occurring? Is someone simply being given an equity line of credit and then taking a lump sum against itself?

For whatever reason, it seems easier to visualize the movement of funds in the traditional 2nd lien HELOC plus mortgage setup than it does in the 1st lien situation. Thanks!

Risk-wise, you’re still dealing with a line of credit that’s typically variable-rate and can be reduced or frozen, so the same core risks (rate risk, liquidity risk, and added complexity) still apply. If you want, share how yours is set up (do you still have a traditional first mortgage, or is the HELOC the only lien?) and I can be more specific.

Thanks. I don’t have one, and was just curious how the first lien HELOC worked systematically. In the scenario with the traditional HELOC, you essentially have the movement of funds from the HELOC draw to the traditional mortgage principal. In the first lien HELOC scenario, I assume the draw from the line of credit/equity is simply placed right back into the account. And then of course, if conducting the velocity banking aspect one treats it as the checking account and dumps all of their income in at the beginning of the month, waits to pay bills and the main HELOC (“mortgage”) payment at the end of the month, etc. I suppose I was just wanting to clarify what difference it really made being a first lien position vs opening a traditional 2nd position/behind the mortgage HELOC. If there isn’t any additional acceleration factors, then for the goal of crushing the mortgage debt, one might as well just do the same thing with their excess cash flow by staying in their traditional mortgage and sending that excess to the lender in principal only payments. (In summary of course – certainly there are all the other factors one can consider that you pointed out already above, such as the two-way street/liquidity of the HELOC vs tying up all of your payments into the traditional mortgage payoff, etc. etc.).

Hopefully I’m making sense – ultimately just was curious if there was something unique about choosing the first lien position (essentially making the HELOC replace the mortgage) over the traditional HELOC/2nd position structure. Thanks again!

You’re making sense. (:

The key point is that there is no special acceleration feature created by the first-lien position itself. The payoff still comes from applying surplus cash flow to principal earlier. If someone has strong and steady excess cash flow, they can often get a similar result by keeping a traditional fixed-rate mortgage and making extra principal payments. The first-lien structure mainly changes cash-flow management and liquidity. It does not change the underlying math.