At a Glance

- If you’re under 18, you’ll need your parent’s help getting started investing. If you’re over 18, you can open an investment account on your own (we cover both below).

- As a teenager, you have the ability to leverage a massive advantage called compound returns. If you understand and utilize this concept now, you can become quite rich over your lifetime.

- Many teenagers mistake investing as a way to get rich quick. But good investing is more about earning decent returns over a very long period of time. That’s when the magic of compounding really kicks in.

My grandpa helped me get started investing at the age of 19, and as you’ll see in this article, I’m incredibly grateful for everything he taught me.

Not only did his help influence my decision to become a CERTIFIED FINANCIAL PLANNER™, but it’s also been extremely rewarding from a financial standpoint.

In this guide to investing as a teenager, I’ll share some of my grandpa’s most powerful lessons. Plus, I’ll give you straightforward instructions so you can begin investing the right way, with the right mindset.

First and foremost, understand one important rule: it’s never too early to start investing.

In fact, starting early gives you a huge advantage. It even makes becoming a multimillionaire over the course of your life a realistic and achievable goal.

Note for parents: While this post is aimed at teens, you’ll find tips and resources throughout to help guide your child’s investing journey. If you’re looking for platforms that combine spending, saving, and investing for younger users, be sure to check out our best banking and investing apps for kids and teens guide.

What Happens To Every Dollar You Invest Today

Say you invest $500 every year from the ages of 16 through 19 — a total of $2,000 over the course of four years.

And let’s say that you’re able to earn a 7% return on your investment, which is the average annual return produced by the stock market. So, it’s available for anyone to invest.

Here’s what that $2,000 investment would be when you’re older:

| Your Age | Value |

| 65 | $49,889 |

| 70 | $69,971 |

| 75 | $98,138 |

| 80 | $137,644 |

Not too bad, right?

Let’s have a little more fun.

Say you’re able to earn a bit more money in your 20s, and that from the age of 20 to 29, you’re able to invest $2,000 each year for ten years, a total of $20,000.

Combined with the $500 per year you invested from the ages of 16 through 19, here’s what your investment would grow to at that same 7% annual rate of return.

| Your Age | Value |

| 65 | $365,565 |

| 70 | $512,724 |

| 75 | $719,122 |

| 80 | $1,008,606 |

Alright, so you’re a millionaire. Although it’s going to take a while.

Now, let’s have a lot of fun. Say that from the ages of 30 through 65, you’re able to save $5,000 per year.

Combined with your earlier investments, here’s how much money you’ll have:

| Your Age | Value |

| 65 | $1,105,132 |

| 70 | $1,550,005 |

| 75 | $2,173,962 |

| 80 | $3,049,095 |

As I hope you’re beginning to see, this is where the so-called magic of compound returns really begins to kick in. Setting aside just a small amount of money year in and year out can add up to millions of dollars over your lifetime.

Even if you just save a little, like $100 a month, consistently over your lifetime, you can become a millionaire. And if you are able to save more once your income grows in your 20s and 30s, becoming a multimillionaire is completely realistic. The big advantage is that you are starting so young, so it does not take nearly as much as you might think.

The Power of Compound Returns

You’ve probably heard the name Warren Buffett. If not, he’s widely regarded as one of the greatest investors in history.

He’s also one of the richest people in the world today. And he’s also 95 years old in 2025 (remember that last fact).

What factor is most responsible for Warren Buffett’s success?

Well, he’s picked good investments for sure.

Over time, he’s earned around 20% per year on his investments. In our example above, we earned just 7% per year.

Ideas worth knowing: The average annual return for the S&P 500 index, which measures the stock performance of the top 500 companies in the United States, is about 10%. In the example above, I used 7% because of what’s known as inflation. Inflation occurs because prices tend to rise over time, so a dollar today is more valuable than it will be 50 years from now. Another way to look at this is by thinking about “purchasing power,” or how much “stuff” $1 can buy at any given time. The average inflation rate is about 3% per year.

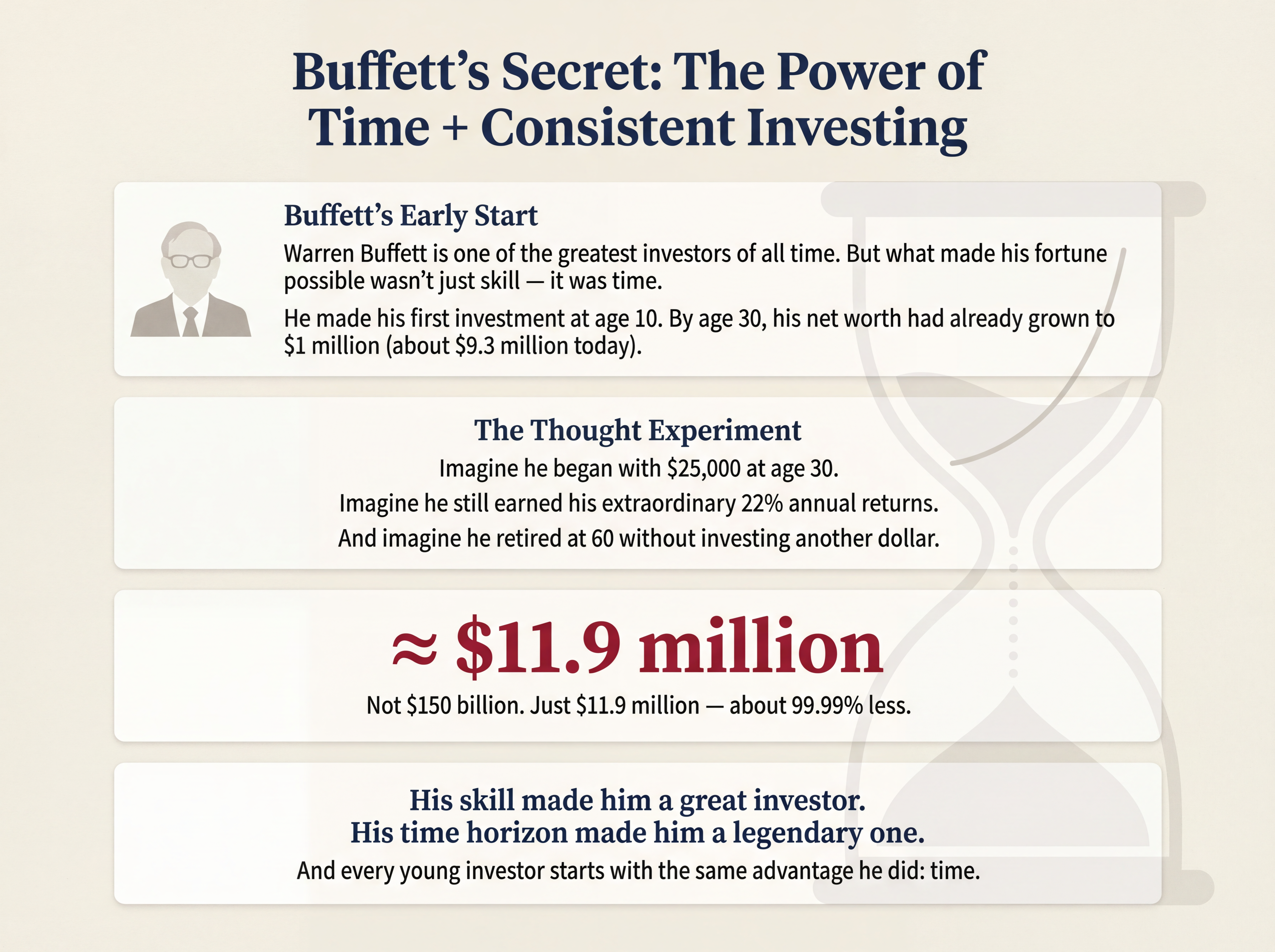

What has made Warren Buffett one of the richest people on the planet is this: time.

Buffett made his first investment at the age of 10. That gave him, as of 2025, 85 years for his investments to grow through the power of compound returns.

What would Buffett’s net worth be today without this early head start?

As this 2020 article explains (his net worth today is now estimated at over $150 billion).

By the time he was 30, he had a net worth of $1 million, or $9.3 million adjusted for inflation.

But what if he was a more normal person, spending his teens and 20s exploring the world and finding his passion — and, by age 30, his net worth was, say, $25,000?

And let’s say he still went on to earn the extraordinary annual investment returns he’s been able to generate — 22% annually — but quit investing and retired at 60 to play golf and spend time with his grandchildren?

What would a rough estimate of his net worth be today?

Not $81 billion.

$11.9 million (99.9% less than his actual net worth).

There’s more to the story: You might be wondering how exactly Warren Buffett had a net worth of a million dollars by age 30.

Buffett held many jobs, and started a lot of businesses at a very young age. For example, he had newspaper routes, sold used golf balls, had a gum-ball machine business, and bought a pinball machine and placed it in a barbershop (splitting the profits with the owner).

Most importantly, he saved as much of this money as he could, and invested early and often.

The power of a solid income, combined with a high savings rate, is how Buffett got his first million at such a young age — and is by far the most realistic way to get rich.

As a teen, you also have the massive advantage of time being on your side.

Now, let’s learn how to take advantage of it.

The Investing Laws Teenagers Need To Know

Before you start investing as a teen, there are a few simple laws you need to understand.

If You’re Over The Age Of 18

You’re legally allowed to open an investment account on your own at the age of 18.

However, know that some brokers, which are companies where you invest your money like Vanguard and ETrade, have higher minimum age requirements in some states.

If You’re Under The Age Of 18

You’ll need your parents to help establish an investment brokerage account if you’re under the age of 18.

The most common type of account your parents can open, to let you start investing, is a custodial account.

With a custodial account — which is also sometimes called a UTMA account — your parents set up the account, and then once you turn 18 or 21 (it differs depending on the state you live in) the account becomes yours.

Parents, by law, administer the account until you reach the specified age. So they have total control over the account. As such, you’ll need to work with them to establish guidelines for how to use it (like what to invest in).

Any money contributed to a custodial account — whether it comes from the adult or the teen — is considered a gift into the account. In 2025, the maximum amount one can give without incurring a gift tax penalty is $19,000 (or $38,000 for married couples who file a joint tax return).

Note for parents: Money contributed to a custodial account does impact eligibility for financial aid. See: Do funds in the custodial account affect eligibility for financial aid of the beneficiary? Also, see, Trump Account vs 529 vs UTMA: Which Account Should You Use?

Why You Want To Invest In A Roth IRA

The little tip you’ll learn next has the power to double the amount of money you get to keep throughout your lifetime.

As a teen, one thing you haven’t had much experience with is taxes.

But if you’ve ever worked a part-time job with an actual paycheck, then you know that the amount you make per hour doesn’t reflect how much money you actually get.

For example, if you earn $15 an hour and work 10 hours, that doesn’t mean your paycheck will be $150. It will probably look more like $120 after you pay taxes, which are usually taken out of your check automatically.

Unfortunately, there are taxes in investing, too.

But what’s important to know is that there are ways to minimize your taxes so that you get to keep more of your money.

The best way to pay less in taxes and keep more of your money over your lifetime is with an account called a Roth IRA.

Key Fact: An IRA, or “individual retirement account,” works almost exactly like a traditional brokerage account. When you have an IRA, you can invest in stocks, bonds, mutual funds and almost any other investment option you can think of. But as we’ll discuss below, IRAs come with some valuable benefits compared to other types of accounts.

A Roth IRA allows you to invest after-tax dollars into a special type of investment account. Then, as long as you keep that money in your account until the age of 59 ½, the money isn’t taxed.

You’d think everyone would want to take advantage of this unique opportunity. But surprisingly, quite a few people don’t.

Note for parents: A Roth IRA is preferable over a traditional IRA for teens, because unless your child is earning a high income, their tax rate is very low.

How big of a difference does this make? Well, let’s see what happens to a $2,000 investment over the course of 60 years, based on data from BankRate.com.

| Marginal Tax Rate | Total Contributions | Value | |

| Taxable Account | 25% | 120,000 | $823,716 |

| Roth IRA | 0% | 120,000 | $1,740,934 |

That’s right: a Roth IRA has the power to more than double your money!

The one thing about a Roth IRA is that in order to utilize this type of account, you’ll need to show earned income under your name when your parents file their taxes (which is income from any type of job or business you run).

The amount you contribute to an IRA can’t exceed the amount of earned income you make. That means if you only earn $2,500 this year, you can only contribute $2,500.

Related: The best online jobs for teens.

The Best Investments for Teens

Most people just jump into investing without a plan, and without the important knowledge discussed above. But now that you’re equipped with this valuable knowledge, you’re ready to actually make an investment.

The entire subject of investing is a complicated one. You could even go to college for the next 10 years of your life and study different ways to invest your money.

In this guide, we’re going to focus on three of the simplest and best ways to invest your money and start taking advantage of the power of compound returns.

Index Funds For Teens

Instead of owning stock in one company, index funds allow you to purchase stock in a wide range of companies.

For example, one of the most popular indexes is the S&P 500. Buying an index fund that owns all the stocks in the S&P 500 allows you to own a small percentage of the largest 500 companies in the United States.

That means you’ll own shares in companies like Apple, Facebook, Google and Amazon but also lesser-known companies in industries you might not have considered, like energy, banking and transportation, just by buying an index.

This is known as a passive (or what some might call a “lazy”) investment strategy, because you’re letting the index fund decide what stocks you should invest in.

Here’s the thing: this is one place where being “lazy” is actually a big advantage.

In fact, 85% of professional investors couldn’t beat the performance of index funds over the last 10 years.

Investing in passive index funds is even the advice Warren Buffett says to follow.

In my view, for most people, the best thing is to do is owning the S&P 500 index fund.

Recommended Broker: If you’re over 18, consider opening an account with Betterment. Betterment is a robo-advisor, so they actually manage a group of diversified index funds for you. That means all you need to worry about is saving as much money as you can. They also allow you to invest in a Roth IRA.

If you’re under 18, you can go with Charles Schwab. While I love Vanguard for investing in index funds, they have a higher minimum account balance of $3,000.

Charles Schwab has a $0 minimum, and allows you to invest in ETFs and mutual funds.

What to invest in: If you’re investing with Betterment, you can go with their 100% stock portfolio. This portfolio gives you a diversified set of index funds and offers the largest potential for gain.

If you’re investing with Charles Schwab, you can invest in a very broad-based index fund that covers the entire S&P 500, such as the Vanguard S&P 500 ETF (VOO), or the Vanguard Total World Stock Index Fund (VTSMX). This gives you the opportunity to own shares of stock in the largest U.S. companies, but you’ll also own shares of companies in other countries as well.

For a complete step-by-step process, see: How to Start Investing Without Feeling Overwhelmed.

The Best Way For Teens To Invest In Stocks

Stocks are fun to invest in. Pick the right one and you can watch your investment soar. Yet this is a lot easier said than done — take it from me, a guy who bought Tesla shares for $26 and sold them way too soon…

In fact, a wide body of research shows that most people who pick individual stocks over index funds earn less money over time.

But, then again, this is one of the lessons a lot of people, myself included, need to learn the hard way. And, learning it on a small scale early in life is a lot better than losing a lot of money later in life.

One idea would be to split the amount you invest into your IRA. For example, for every $100 you invest, $50 goes towards index funds and $50 goes towards your individual stock portfolio.

Final Thoughts On Investing As A Teen

The payoff to learning to invest early is massive. It can give you a huge head start in life. And, as you’ll come to learn, a lot more freedom and flexibility of your time.

After all, having a significant investment account provides a level of financial security that can allow you to make decisions based more on what makes you happiest, and less on what will bring in the absolute most money.

If you’re interested in investing, it’s also not a bad idea to learn more about personal finance and bolster your financial literacy. Understanding the basics of money management can allow you to actually invest more of your money over your lifetime.

So, it’s not about making a few stock trades that can help you make money, but about understanding how to manage your money as a way to improve your life.

This is where reading a few good books on the topic, and having this knowledge early, will give you an incredible advantage in life.