Monte Carlo simulations are one of the best tools in any financial toolkit.

In my 20s, they sparked optimism: “If I keep maxing out my IRA and contributing to a 401(k), I’ll have this much saved.” By my 30s, they provided reassurance: “Life is expensive, but if I stick to this savings plan, I should be fine.”

Now in my 40s, my focus has shifted to: “After two decades of saving, retirement is getting closer — does my plan still hold up?”

Most retirement calculators assume a steady 7% to 10% annual return. Monte Carlo simulations, on the other hand, run thousands of scenarios to show a range of outcomes that mirror the unpredictability of real markets.

This approach provides a probability of success rather than a static projection, accounting for risks like inflation or the impact of retiring before a downturn — think 1999 or 2007.

While no tool is perfect — after all, Monte Carlo simulations can’t fully account for human behavior — they excel at providing a historical perspective from which to stress-test portfolios.

Here are the best free Monte Carlo retirement simulation calculators I’ve found, along with notes on who each tool is best for.

Click the links below for a deeper dive on each.

- Empower. Best for retirement planning, with real-time data from linked accounts (valuable for both savers and retirees).

- cFIREsim. Best for advanced users who want detailed control over withdrawal strategies and historical performance.

- FIRECalc. Best for quickly stress-testing basic U.S. index-based retirement portfolios against historical market conditions.

- Rich, Broke, or Dead Calculator. Best for retirees to visualize mortality risk alongside financial outcomes.

- FICalc. Best for analyzing variable percentage withdrawal strategies.

- Engaging Data’s Retirement Calculator. Best for estimating how savings rate and retirement spending impact the time needed to retire.

#1. Empower

Best for using actual financial data from linked accounts to give personalized retirement insights and scenario planning.

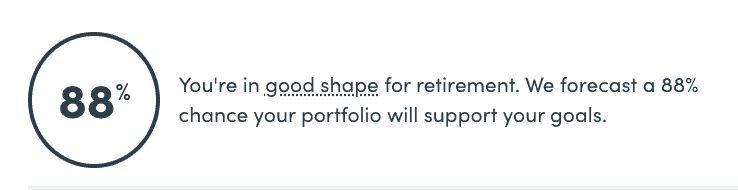

I’ve been using Empower since 2017 (when it was called Personal Capital). I use the tool twice or so per year to check whether my savings rate, investments and expenses are aligned with my goals (which, in my 40s, is a few decades away).

With Empower, after linking your accounts, you’ll see the percentage likelihood of whether your portfolio can support your retirement goals.

You can change inputs like monthly spending and Social Security, and add part-time income to see how this impacts your projections.

Key features of Empower include:

- Runs 5,000 simulations to estimate the likelihood of your portfolio supporting your retirement.

- The tool syncs directly with your accounts to pull real-time income, expenses and investment data, offering precise results.

- You can test variables like savings rate changes, part-time retirement income and spending shifts.

The tool emphasizes Modern Portfolio Theory, helping users optimize their portfolios for the highest returns with minimal risk. While the tools are free, they are part of Empower’s broader offering, which includes private wealth management services.

The tool’s design is the best I’ve seen. It’s highly intuitive, even for those without a strong background in investing.

Our full Empower review offers a deeper dive into its features.

#2. cFIREsim

Best for intermediate to advanced users who want detailed control over withdrawal strategies.

cFIREsim is a highly customizable tool popular in the FIRE (Financial Independence, Retire Early) community. It uses historical stock, bond, gold, interest rate and inflation data from 1871 to the present to simulate how a retirement portfolio would have fared.

It feels like using a spreadsheet, running detailed calculations based on user-provided inputs to assess the success rate of a retirement portfolio. It’s entirely web-based and requires no sign-up.

Key features include:

- You can enter specific spending levels, portfolio size and retirement length to get a success rate (e.g., “96.67% success — Failed 4 of 119 cycles”) that shows how often the portfolio sustains spending across historical scenarios.

- Adjustments include pre-retirement savings, pensions, mortgage payoffs, one-time expenses and college costs.

- Generates well-designed graphs and tables that show portfolio growth, spending patterns and average outcomes.

While its interface initially feels overwhelming, cFIREsim stands out thanks to its precise, data-driven approach and customization options. Notable features include the ability to model portfolio rebalancing and multiple Social Security income streams with custom start years.

This isn’t the tool for a quick snapshot or rough estimate. Instead, it’s designed for those who come prepared with detailed numbers and want a highly accurate analysis based on their specific inputs. If you’re willing to invest the time, cFIREsim is powerful.

#3. FIRECalc

Best for quickly stress-testing basic U.S. index-based retirement portfolios against historical market conditions.

I first encountered FIRECalc around 15 years ago. It’s one of the original free historical simulation tools. While the interface hasn’t changed much, the historical data is updated through April 2024.

Key features include:

- Enter spending, portfolio size, and expected retirement length to see how long your money will last.

- Enter variables like pensions, Social Security and fluctuating spending.

- Adjust spending levels, portfolio size, retirement duration and asset allocation.

FIRECalc is best for a quick back-test on basic retirement portfolios composed of U.S. index funds.

It’s limited to U.S. market data, making it unsuitable for modeling international stocks or other assets like REITs. This limitation also makes it not work for modern, diversified portfolio compositions typically offered by robo-advisors.

Another significant limitation is its handling of taxes. FIRECalc doesn’t account for assets in tax-advantaged accounts like Roth or traditional IRAs.

Overall, FIRECalc effectively estimates how long your money will last with minimal input.

#4. Rich, Broke, or Dead Calculator

Best for retirees to visualize mortality risk alongside financial outcomes.

The Rich, Broke, or Dead Calculator compares the likelihood of running out of money to the chance of passing away during retirement. You input your numbers to determine whether you will end up… well, rich, broke, or dead.

Key features include:

- Known for its “Wedge of Death” graphic, the tool highlights how death often outweighs the risk of running out of money, especially in later years.

- Uses stock, bond and cash return data from 1871 to 2024.

- Adjust asset allocation, spending levels, and additional income sources, such as Social Security or pensions, with start and end dates.

The Rich, Broke, or Dead Calculator excels at visually displaying the success rates of your existing retirement portfolio. This is particularly useful for those evaluating whether an additional year of work could significantly improve their retirement outcomes.

For example, the calculator can show that working one more year might only increase your success rate by 5%, but adding a part-time income in a few years could boost it by 7%. This makes it easy to evaluate trade-offs and explore alternative strategies.

#5. FICalc

Best for analyzing variable percentage withdrawal strategies.

FICalc focuses on withdrawal strategies, showing how different approaches affect retirement savings. Its modern, user-friendly design works on both desktop and mobile.

Key features include:

- The most withdrawal strategy options of any calculator I’ve tested, including the endowment strategy and glide path support.

- Easily adjust portfolio allocation, spending levels, and retirement duration.

- Provides success rates, charts, and the ability to drill down into specific simulations.

While the tool has strengths, it lacks options for more diverse portfolios, such as international or small-cap stocks.

The most significant limitation — understandably tricky to incorporate into a calculator — is its inability to account for tax-advantaged accounts. Tax implications are a huge factor for anyone focusing on withdrawal rates. So, what looks optimal in the calculator may not be the best strategy once taxes are factored in.

#6. Engaging Data’s Retirement Calculator

Best for estimating how savings rate and retirement spending impact the time needed to retire.

Engaging Data’s FIRE calculator focuses on answering the critical pre-retirement question: “When can I retire?”

Unlike tools that assess whether your savings will last through retirement, this calculator helps estimate how long it will take to reach your retirement target based on your current savings rate, spending and investment strategy.

It provides a detailed timeline for achieving financial independence using fixed returns, historical data and Monte Carlo simulations. This allows you to explore how savings, income or asset allocation changes affect your retirement date.

It’s excellent for evaluating opportunity costs — like how a higher-paying job or a lower cost of living today could shift your retirement timeline, helping you retire sooner or later.