In this review of Empower (which used to be called Personal Capital), we’ll explore the platform’s offering on the consumer side, including its comprehensive financial dashboard and wealth management service.

Whether you’re a novice investor looking for a way to track your investments or an experienced investor considering moving your assets to Empower, this review provides an in-depth analysis.

What Is Empower?

Before acquiring Personal Capital in 2020, Empower was most well-known for offering retirement services to corporations. While a large company, it was not a household name for most individual investors.

By acquiring Personal Capital, Empower expanded its service offerings to include individual wealth management and financial planning tools.

Plus, integrating these tools into its existing services has allowed Empower to offer a more comprehensive suite of financial management services to its existing clients.

In 2023, Empower officially dropped the Personal Capital brand name.

Empower’s three main consumer offerings include the following.

Product #1: Free Financial Dashboard

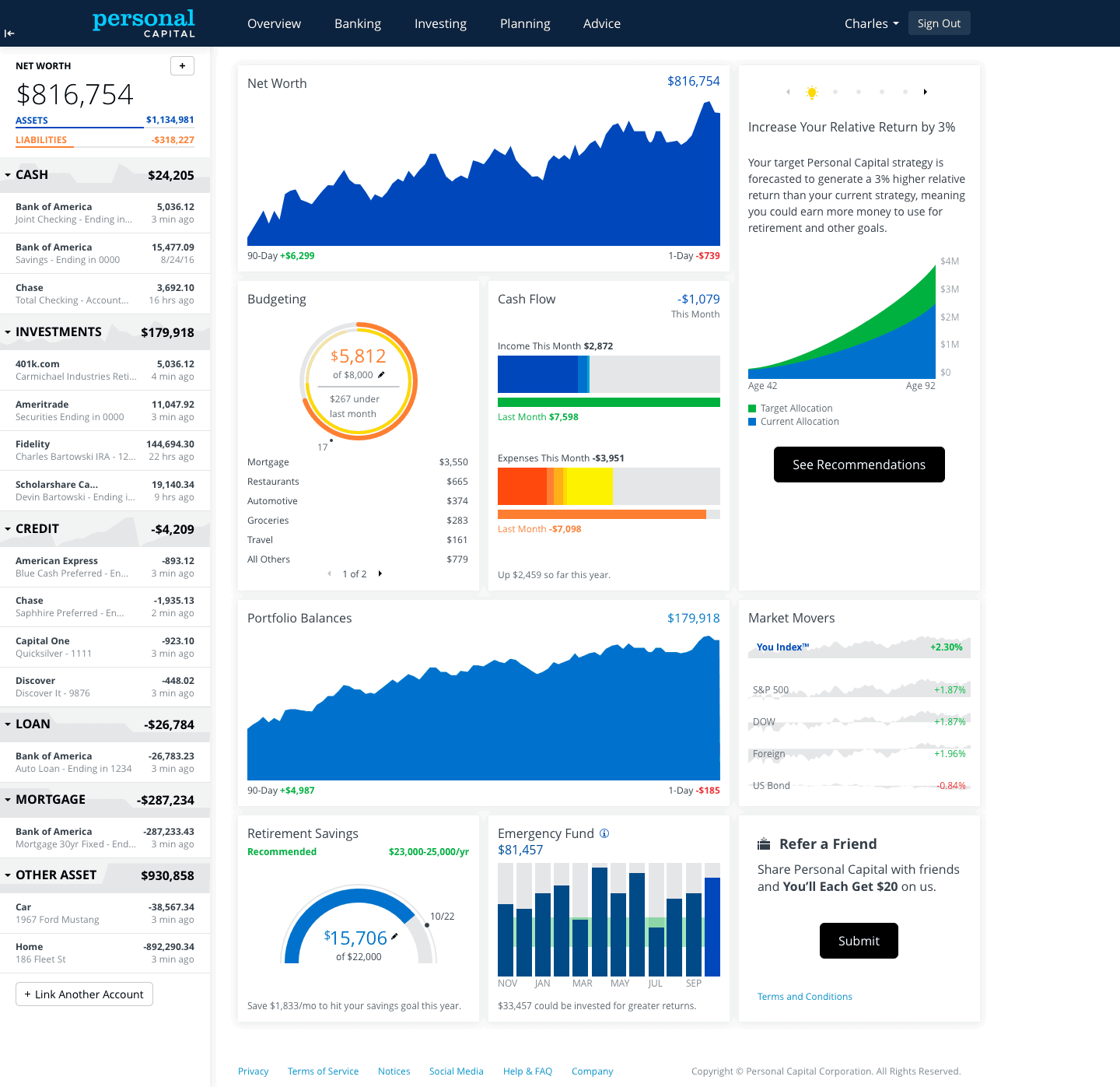

The first of these products is a free financial dashboard that lets you link your accounts so you can manage your money and track your investment portfolio in one online location.

You gain access to this dashboard immediately upon signing up for an Empower account. Its tools cover budgeting, cash flows, education planning, investments, retirement savings and more. We’ll dive into these tools in detail later in the article.

Here’s an example (from the company’s press kit) of what the dashboard looks like:

Product #2: Cash Management Account

Empower’s other free product is a high-yield “cash management” account (aptly named Empower Personal Cash) that offers up to $2 million in FDIC insurance coverage (more than what a single bank can offer).

There’s currently no debit card with the account; it’s simply for holding cash. Empower has stated that a debit card is in the works, which will make this a combination of a checking and high-yield savings account.

Product #3: Wealth Management Services

Lastly, Empower offers a tiered wealth management service that you can access with a minimum account balance of $100,000. Wealth management is the only Empower service that requires you to deposit funds on the platform — the financial dashboard and Empower Personal Cash are free and available to anyone.

Empower’s Free Financial Tools

Empower’s free financial tools are designed to help you make better decisions with your money. You can still use and benefit from Empower’s free financial dashboard even if you don’t have $100,000 in investments to move to the platform.

These tools cover nearly every aspect of your finances, but they emphasize your investments — with a particular focus on helping you make sure you have enough money for retirement.

All of these tools are contained within a single dashboard. You can link your checking, savings, investment, loan, credit card and mortgage accounts (among others), allowing you to view your entire financial life in one place.

Empower supports over 12,000 financial institutions. If you can’t find yours, you can link it manually or request that Empower add it to their database.

You can even link other assets, including

- Your home. Empower uses Zillow’s Zestimate valuation model to calculate your home’s value. This is an estimate, not an appraisal, but it can still help you understand what your home might be worth.

- Vehicles. Empower asks for your car’s current make, model, year and value. Cars are an asset, so you’ll want to link them to your account.

- Jewelry. You can link your jewelry by manually inputting a description and its value. By doing so, Empower can see a more accurate picture of your net worth, which in turn aids it in providing you insight and recommendations.

- Art. Any art that you own is also part of your net worth. As with jewelry, you must know its value to link it.

What’s in the Dashboard

These are the free tools you’ll find in the Empower dashboard.

Bills

The “Bills” section displays information on all upcoming credit card, loan, and mortgage bills for your linked accounts. It tells you each bill’s due date, as well as the date of your most recent payment. For each credit card, you can see your statement balance, total balance, and minimum payment.

This is an excellent tool for managing multiple debts at once. Instead of checking due dates or statement balances by logging into each loan or credit card’s website, you can view this information in one location. As someone who carries their fair share of travel rewards credit cards (usually around six to 10 at any given time), this feature is extremely helpful.

Plus, Empower links each bill to its respective website for added convenience.

Budgeting

Empower heavily emphasizes investment advice, but its budgeting tool works well if you want a quick, informative look into your monthly spending habits.

It breaks your expenses out by category, which can help you identify areas where you need to trim your spending. It also sets a default monthly budget using this spending data. While you can’t yet set budgets for each category, you can adjust your monthly budget as you please.

Visuals are used to enhance your understanding of your spending. On the left side of this screen is a graphical illustration of the amount of your budget you’ve spent. To the right is a bar graph containing your total spending per day or month.

Below these two graphs is a list of the current month’s transactions. You can see which account you used to complete each transaction, and this can further aid you in finding specific areas in which you’re spending too much.

I’ve tested dozens of budgeting apps, and Empower is one of the better ones — though not the absolute best. While there are no ads or product offers, its user interface is a bit more cluttered than something like Rocket Money (see my Rocket Money review), which means it’s not the easiest option if you need to keep a close eye on every penny.

In my opinion, it’s best when used as a cash flow analysis tool that gives you greater insight into what you spend versus what you earn.

Cash Flow

The Cash Flow Analyzer displays most of the same information as the budgeting tool, but from a cash flow perspective. It charts your cash flows over time and shows a “this time last month” comparison. You can view your overall cash flows, or you can look just at income (cash inflows) or expenses (cash outflows) by category.

Tracking your cash flows is essential because net worth doesn’t tell the whole story. You could own a valuable illiquid asset (such as a home) and have a positive net worth. Yet, you’ll be stuck living paycheck-to-paycheck if you spend every penny you earn.

Education Planner

Whether you’re saving for your child’s education or planning to go back to school yourself, the Education Planner will be of great use to you.

The Education Planner does not have its own section — instead, it’s a part of the Retirement Planner tool (which is discussed below).

Using this tool, you can create scenarios to determine if you’re currently on track to be able to afford college tuition in the future. Empower gives you dollar figures for average in-state, out-of-state, and private institution tuition.

You can add a specific college for more accurate planning.

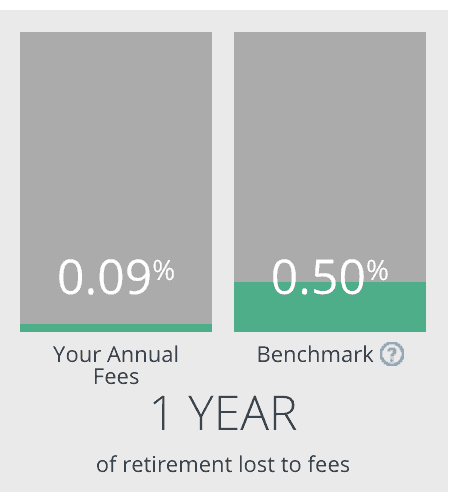

Fee Analyzer

Despite your best efforts to save for retirement, fees could be robbing you of some of your savings.

Empower’s Fee Analyzer details how much you could be losing to fees, both visually and numerically. Using information from your linked investment accounts, the Fee Analyzer displays a graph that illustrates in red how much money you’re paying.

If the graph isn’t enough, the Fee Analyzer also tells you how many years of retirement income you’ll lose to fees over your career.

With this information, you can adjust where your retirement savings are going and potentially shave several years or more off your time in the workforce.

Worth noting is that it’s common to have quite a few old 401(k)s floating around. Most 401(k)s have outrageous fees — often 20 times the cost of investing the account on your own!

By checking the dashboard’s 401(k) fee analyzer, I see that I’m paying only 0.09% in annual fees. The benchmark is 0.50%.

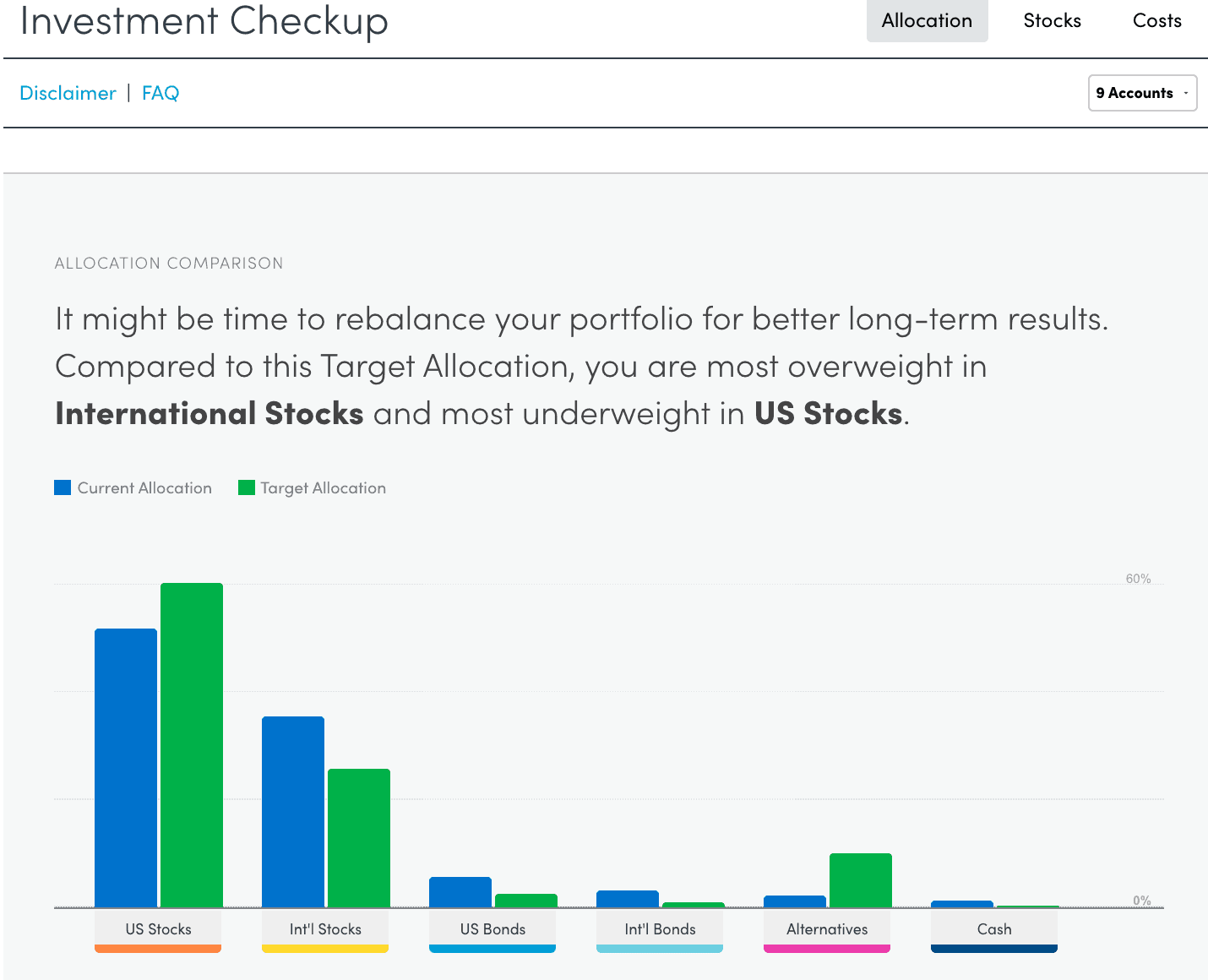

Investment Checkup

A famous study from the 1980s, “Determinants of Portfolio Performance,” concluded that asset allocation accounts for 95.6% of an investor’s return. In other words, it’s the single biggest factor by a wide margin.

I find that improper asset allocation is quite common among all age groups. Millennials tend to be afraid of the market and therefore avoid it altogether, with one study showing that less than 50% of people ages 23 to 38 held stock. Meanwhile, Gen Xers often lack a clearly defined target, while those closer to retirement often have unnecessary levels of risk in their portfolio.

Empower’s Investment Checkup tool is designed to help you avoid those common pitfalls. After signing up, linking your accounts and providing a little bit of information about your goals, the Target Allocation feature (as shown in the screenshot below) gives you an easy-to-read graph that highlights your current allocation compared to a potentially more ideal balance, allowing you to see which would provide the greatest expected return — taking into consideration your needs, desires and ability to take risk.

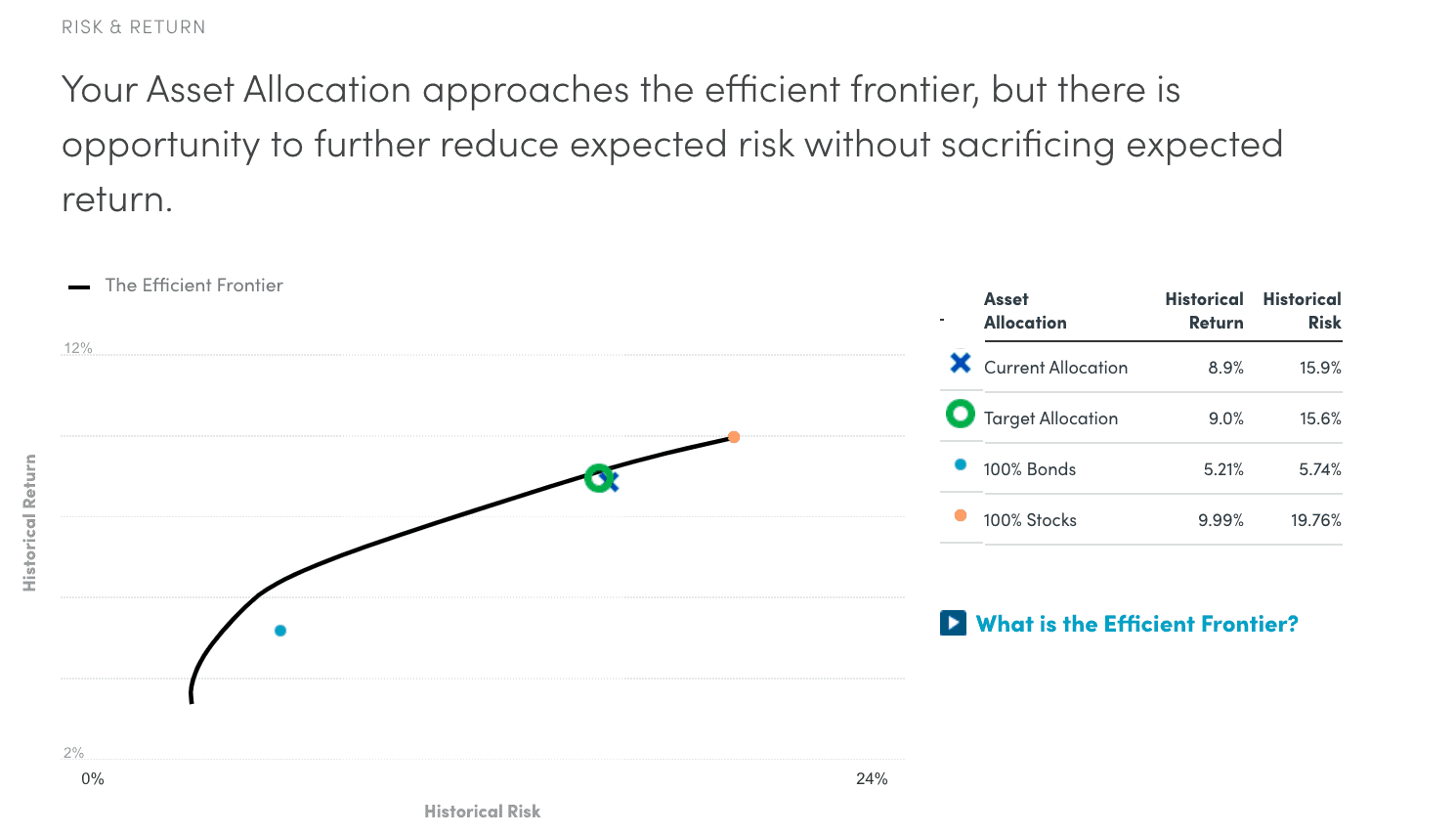

Another valuable benefit of the Investment Checkup tool is the ability to see where your current allocation falls on the Efficient Frontier, which represents the set of allocations that offer the highest expected return at a given level of risk.

Investment Checkup also shows you a side-by-side comparison of your current portfolio versus its recommendation in terms of historical performance, projected retirement savings and risk/return.

You can then adjust the target allocation from its initial recommendation depending on whether you want a more conservative or aggressive investing approach.

Investment Checkup is one of the most helpful features in the dashboard, providing you with free insight into how much you can grow your wealth by optimizing your portfolio’s allocation.

And frankly, Empower’s asset allocation algorithms are quite good. If you know nothing about investing and follow their recommendations, you’ll still be in a good position relative to the majority of other investors.

The Investment Checkup section also shows you other valuable information, including the exact dollar amount you’d need to rebalance your portfolio in order to optimize return and minimize risk, and future projections of your current portfolio based on expected annual returns.

Net Worth

The Net Worth tracker compiles information from your linked accounts, as well as any assets you’ve added manually. The best part is you can monitor your net worth over time. That’s valuable because seeing your net worth inch upwards can motivate you to continue working hard on your finances.

You should always have an idea of your net worth because it shows you long-term trends in your financial health. Tracking your net worth over time can indicate whether or not you’re moving in the right direction.

Portfolio Tracker

In the Portfolio Tracker, you can view several pieces of information regarding your investments:

- Holdings: contains information regarding the quantity and share prices of your holdings.

- Portfolio: displays changes in your portfolio balances.

- Performance: tracks the historical performance of your portfolio.

- Allocation: uses boxes to visually display the weights of each asset class held within your portfolio.

- U.S. sectors: contains a graph of your equity holdings in U.S. sectors.

One unique feature of the portfolio tracker, called the You Index, compares your portfolio against the broader market as if your portfolio was a market index. The You Index charts the performance of your cash, stock, ETFs and mutual fund holdings against the DOW and S&P 500, as well as indices for foreign equities and U.S. Bonds.

In the screenshot below, you can see how my portfolio performed in 2019.

By clicking on each tab, you can then compare how your portfolio performed compared to certain indices. For example, here’s how I measured up against the S&P 500. (You can also compare against the Dow, foreign markets, and the U.S. bond market.)

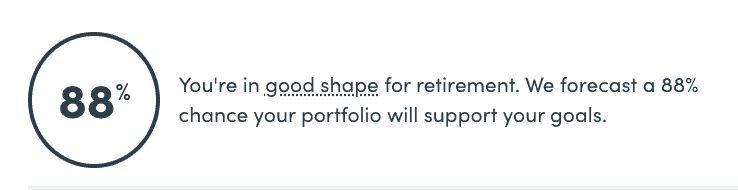

Retirement Planner

Planning for retirement is no easy feat, but Empower’s free planning tool can help you see if you’re on track.

You can create several “what-if” scenarios based on income and expense events to determine if your retirement goals are feasible.

Income scenarios include:

- Annuity income.

- Inheritances.

- Pension income.

- Rental income.

- Sales of property

- Social Security income.

- Work during retirement.

- Other income.

Expense scenarios include:

- Charitable giving.

- Dependent support.

- Education.

- Healthcare.

- Home purchase/upgrade.

- Renovations.

- Vacations.

- Vehicle purchases.

- Weddings.

- Other expenses.

Once you create a few scenarios, you can compare them back-to-back to aid you in making important life decisions.

For example, let’s say you and your spouse are planning on having kids. You can add Dependent Support and Education spending goals to your current plan to see if you’ll be able to support a child and their future educational expenses.

With the ability to plan for several scenarios and analyze them side-by-side, you can create retirement contingency plans to prepare for whatever life throws at you.

The Retirement Planner doesn’t stop at saving for retirement, though; a new Smart Withdrawal Tool uses several pieces of your tax information to create a retirement withdrawal strategy that minimizes taxes and penalties.

Running out of money in retirement is a big worry for many people, but maximizing your tax benefits and avoiding early withdrawal penalties can make your retirement money go further.

Savings Planner

Unable to decide between saving and paying off debt? The Savings Planner guides your decision-making by pulling in information regarding your retirement savings, cash and current debt.

An important component of the Savings Planner is the Emergency Fund section, as it compares your cash amounts against your monthly budget from the Budgeting tool and recommends a dollar figure for a three to six month emergency fund.

There’s also the Debt Paydown section, which displays each of your debts and their respective interest rates. That way, you can determine if you should target one of your debts next or shift over to saving and investment.

Lastly, the Savings Planner summarizes your current progress by comparing your planned savings for the year with the amount you must save to hit your retirement savings goals.

Empower Personal Cash

Like other online advising/wealth management services, Empower offers a cash management account that combines the strengths of a savings account with some of the conveniences of a checking account.

Tracking their APY over the years, I’ve always found Empower to have among the higher interest rates available.

Empower Personal Cash also charges no fees, requires no minimum balance, and insures your deposits up to $2 million.

The cash account is a nice feature for users of the company’s wealth management services (more on those below), as it represents one less account you need to maintain and has one of the better interest rates for this type of service. However, there is no debit card associated with the account.

Wealth Management Services

Empower’s services sit between a typical robo-advisor and a full-service investment advisory firm.

The platform offers digital investment management services through its robo-advisor platform, which uses algorithms and computer programs to create and manage client investment portfolios.

However, they also offer personalized investment advice from human financial advisors who can provide tailored recommendations based on clients’ unique financial situations and goals.

Three Tiers of Service

Empower offers three tiers of wealth management services.

Tier #1: Investment Services

Their first tier — which is simply called Investment Services — requires clients to have between $100,000 and $200,000 in assets.

Investment Services clients can invest in Empower’s tax-efficient ETF portfolio and request reviews. Clients at this tier have unlimited access to financial planning and retirement help from a team of financial advisors.

Tier #2: Wealth Management

Wealth Management is the next tier, requiring an account balance between $200,000 and $1 million. Empower assigns two dedicated financial advisors to each Wealth Management client. Also, clients at this tier can talk to specialists in other areas of finance, such as real estate, tax, insurance, and stock options.

As for investments, Wealth Management clients can customize their portfolios with a mix of ETFs and individual stocks.

Tier #3: Private Client

At the top of Empower’s tier system is Private Client. If you accumulate at least $1 million in your accounts, you unlock some of Empower’s most exclusive services, including:

- Priority access to Empower’s specialists and investment committee.

- Individual bond and private equity investments.

- Collaboration with an estate attorney and CPA for estate and tax wealth planning.

- Estate, tax, and legacy portfolio construction.

- Lower fees starting at $3 million in investments.

Dynamic Portfolio Allocation

Empower uses all six major liquid and investable asset classes to focus on long-term returns.

- U.S. stocks: growth focus.

- International stocks: growth focus, but also diversifies the portfolio from U.S. stock holdings.

- U.S. bonds: adds stability, income, and diversification to the portfolio.

- International bonds: similar benefits to U.S. bonds.

- Alternatives: diversifies the portfolio and can hedge against inflation, but these assets are highly volatile.

- Cash: adds portfolio liquidity and capital preservation.

The company uses Modern Portfolio Theory and several other tools to determine the optimal allocation of each asset for your portfolio. As your life goes on, they recommend changes in allocation so you can always keep your portfolio in line with your goals and needs.

Intelligent Rebalancing

Rebalancing is the act of buying and selling portfolio holdings to bring the weights of each asset back to their targets. Continuous rebalancing (when the market presents opportunities) can keep you on track to your investment goals and can help you maintain your preferred levels of risk. Additionally, rebalancing can prevent you from making mistakes out of emotion.

Empower’s software checks daily for rebalancing opportunities. Instead of using hard triggers that automatically rebalance a portfolio, their software relies on exception reports to evaluate whether a rebalancing action should be taken before following through.

Smart Weighting

Empower believes that capitalization-weighted indexes like the S&P 500 add unnecessary risk and can increase costs over time because they too heavily favor larger companies while under-representing smaller stocks.

To improve your returns with less risk, Empower’s investment methodology, Smart Weighting, weights three factors equally:

- Economic sector.

- Style.

- Size.

Weighting these factors equally is meant to improve your portfolio’s diversification and protect you against declines in any particular market.

Tax Optimization

Empower emphasizes tax-advantaged investing. They build their portfolios using both individual stocks and tax-efficient ETFs instead of mutual funds.

By including stocks in their portfolios, Empower clients can take advantage of tax-loss harvesting — the tactic of selling securities at a loss to earn a tax deduction or to offset capital gains.

However, Empower’s tax optimization tactics go beyond tax-loss harvesting; they also strategically place investments in accounts where they’d receive the most tax benefits.

To illustrate, let’s say you owned a bond and a dividend-paying stock. Bond income is taxed at ordinary income rates, while most dividends are considered “qualified dividends” and are taxed at favorable capital gains rates.

Empower would attempt to move the bond into an IRA first, as doing so would allow you to defer the higher taxes on your bond income and thus reduce your taxable income in the present.

Empower’s Costs and Fees

Empower does not charge account service or trailing fees, does not charge commissions on your trades, and does not advertise third-party products. All the financial planning and intelligence tools described in this article are free to use — Empower makes its money solely from its wealth management platform.

These are their fees at the time of publication:

| Account Balance | Advisory Fee |

| First $1 million | 0.89% |

| First $3 million | 0.79% |

| Next $2 million | 0.69% |

| Next $5 million | 0.59% |

| Over $10 million | 0.49% |

Empower vs. Facet Wealth

Empower and Facet Wealth are two financial management platforms that sit between traditional robo-advisors and full-service client management firms. Both platforms offer a robo-advisor-like experience, with more personal financial advice and human support.

One significant difference between the two platforms is their fee structure. Facet Wealth offers fee-only financial planning services, meaning clients pay a flat fee for financial advice rather than a percentage of their assets under management.

The cost ranges from $2,000 to $8,000 per year, depending on how complicated the plan is. Additionally, there is a monthly administrative fee of $8 to $15. There are no account minimums.

On the other hand, Empower uses assets under the management approach, where clients pay a percentage of their portfolio’s value for investment management and financial planning services.

Both platforms offer personalized financial advice and support from human advisors, which sets them apart from traditional robo-advisors. However, Facet Wealth places all clients with a dedicated financial advisor who will work with them to achieve their financial goals. Empower, on the other hand, begins to offer dedicated advice for accounts starting at $200,000. If under that amount, you’ll have a team of advisors.

Frequently Asked Questions About Empower

Robo-advisors rely primarily on algorithms to provide investment advice. Although Empower’s free dashboard uses robo-advisor algorithms to some degree (such as optimizing your asset allocation for minimum risk), investment clients can access financial advisory services from human advisors.

Empower uses AES-256 encryption with multi-layer management, along with rotating, user-specific keys and salts. Qualys SSL Labs, an award-winning security diagnostics company, gave Personal Capital’s website encryption an A+.

In addition, no one at Empower can access your credentials for any linked accounts. Credentials are stored with software company Yodlee and are only ever sent to your financial institutions.

Empower makes money solely by charging advisory fees on its wealth management clients’ accounts. It does not generate any revenue from the financial tools. Those are free to use all the time. Empower does not earn referral fees by recommending financial products to you.

Empower Review: Summary and Final Thoughts

If you look back at Empower’s services, their structure makes a lot of sense.

The free financial dashboard can stand in as a financial advisor when you don’t have a lot of money, thanks to its comprehensive set of tools and guidance.

If you fall into that group, there are three primary benefits of the platform.

- Real data. Empower’s Retirement Planner doesn’t work on assumptions — it uses real data from the retirement accounts you link to calculate whether you’re on track to meet your desired timeline.

- Customizable. How will college or a new home impact your retirement? What about an expected boost in income? Empower allows you to see the impact that a wide range of events would have on your goals.

- Discover hidden fees. They’re called hidden fees for a reason. Empower’s Fee Analyzer uncovers the investment fees you’re paying across all your financial accounts.

As you accumulate money over your life and career, you build wealth by investing. These investments can grow in size and complexity to the point where you will need someone else to handle them. That’s when it may make sense to sign up for Empower’s wealth management services, so you can take advantage of its more advanced offerings.

As your investments grow and you advance up each tier, Empower gives you the additional features you need to manage your wealth.

These services come at a relatively high cost, which is offset in part by an excellent array of valuable products.

I would recommend the company’s paid services to the following groups:

- People who have, in the past, tended to make quick, irrational decisions with their investments (which they’ve later regretted).

- People who are not really interested in learning about investing and tax strategy, and are thus seeking a more hands-off approach.

- People who want a real person to bounce ideas off.

If you’re looking for a way to manage your entire financial life in one place and receive investment guidance, Empower is an excellent platform.

I have used Empower/Personal Capital for the past 7 years and have been very pleased with reporting. This year as part of their upgraded program they asked for my complete Social Security Number to continue. This took my by surprise and I have not used it since.