The Chase Trifecta is a straightforward strategy I often recommend to beginners who are looking to get the most value from the Chase Ultimate Rewards points program. This approach is designed to optimize both the number of points you can earn and the value of your points.

Understanding the Chase Trifecta

It’s called the Trifecta because it relies on a combination of three different credit cards offered by Chase.

To understand why the strategy is so powerful, you must understand two key aspects of the Chase Ultimate Reward points ecosystem:

- Only three Chase cards offer transferable points to airline and hotel partners in addition to an increased point value when booking through the Chase Travel Portal: the Chase Sapphire Reserve, Chase Sapphire Preferred, and Ink Business Preferred.

- Chase allows you to move points between credit card accounts.

Without a card like the Chase Sapphire Reserve, Chase Sapphire Preferred or Ink Business Preferred, options for using Chase Ultimate Rewards points are limited, often resulting in lower-value redemptions such as gift cards or statement credits at a 1 cent per point valuation.

However, the fact that you can move points between accounts can increase the value of points earned on any Chase cards that earn Chase Ultimate Reward points.

For example, you can transfer points from a no-annual-fee card like the Chase Freedom Flex to your Chase Sapphire Reserve card and unlock higher redemption values and more flexible reward options.

The links directing to Chase cards on this page are my personal referral links, earning me a bonus when you sign up through them.

Why the Chase Trifecta Works

The Chase Trifecta strategy is designed to optimize the value of your Chase Ultimate Rewards points, particularly when redeeming them through the Chase travel portal and holding a premium card.

For instance, the Chase Sapphire Preferred and Ink Business Preferred cards boost the value of your points by 25% when redeemed through the travel portal. This means that instead of the standard 1 cent per point value, your points are worth 1.25 cents each.

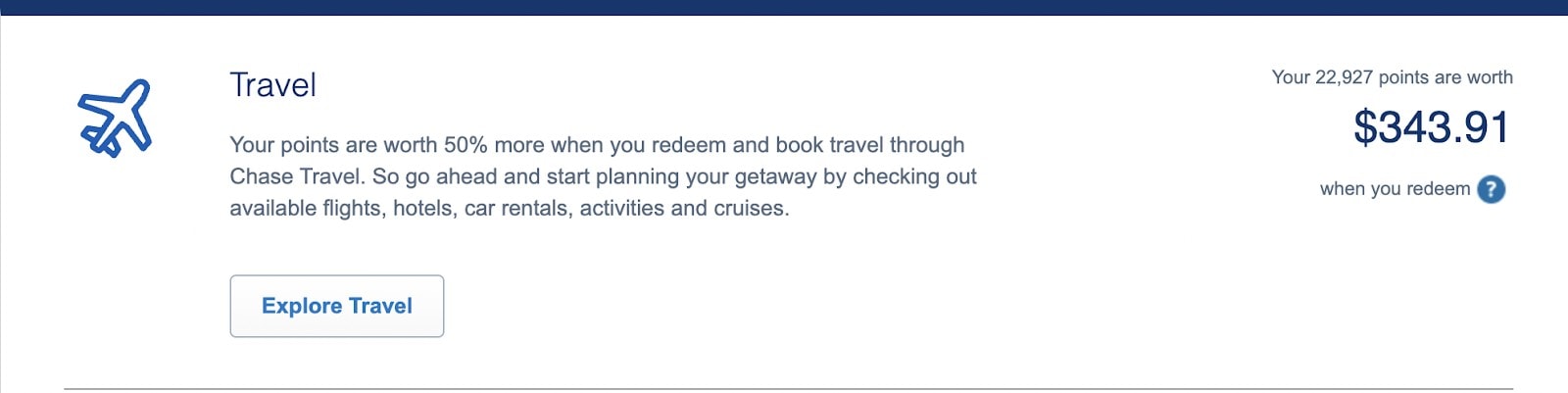

The value increases even more if you have the Chase Sapphire Reserve card. With this card, your points are worth 50% more when redeemed through the travel portal, translating to a value of 1.5 cents per point.

The real magic happens when combining the earning potential of cards like the Chase Freedom Flex, which offers five Chase Ultimate Rewards points per dollar spent in rotating bonus categories.

Transferring points earned on the Freedom Flex to a premium card like the Chase Sapphire Reserve increases your points’ value to 1.5 cents each, effectively boosting your return on spending to an impressive 7.5% (5% x 1.5).

While earning this value on your spending is impressive, you can get even more value by utilizing the transfer partners of Chase.

Suppose you were to book a hotel that normally costs $600 for 20,000 CUR points.

In that case, your points would be worth 3 cents each. And if you earned those points spending within a 5% bonus category using your Chase Freedom Flex, your effective return on spend is an astonishing 15% (5% x 3).

Furthermore, you can earn multiple signup bonuses when you sign up for multiple Chase cards.

Learn how to maximize the value of your Chase Ultimate Rewards for travel in our guides to booking airfare with points and redeeming points for hotels.

Be Aware of Chase’s 5/24 Rule

The Chase Trifecta can be a powerful credit card strategy for earning rewards and maximizing your spending, but it’s important to be aware of the Chase 5/24 rule.

This rule states that if you have opened five or more credit cards from any issuer in the past 24 months, you will not be approved for a new Chase credit card.

So, you’ll need to take a more patient and deliberate approach to build your Chase Trifecta over time. This may mean spacing out your applications over a longer period of time or prioritizing the cards that offer the most benefits and fit your spending habits.

See our article on travel hacking responsibly for more information regarding spacing out credit card applications and protecting your credit score.

What Cards Make Up the Chase Trifecta

Since the term was first coined, Chase has expanded its line of credit card offerings, which means there are now several variations of the Trifecta.

The original version is still valid and involves three cards:

- Chase Sapphire Preferred or Chase Sapphire Reserve.

- Chase Freedom Flex (previously called Chase Freedom).

- Chase Freedom Unlimited.

You have more options today to design the right Trifecta for you. But the key to making the strategy work is having at least one card that earns transferable points. These cards are often referred to as premium Chase Cards.

Your options here for personal cards are the Chase Sapphire Preferred or Chase Sapphire Reserve. However, you can use the Chase Ink Business Preferred if you operate a business.

| Card Name | Bonus Category | Annual Fee |

| Chase Sapphire Preferred | 2x points on travel and dining, 5x points on Lyft rides. | $95 |

| Chase Sapphire Reserve | 3x points on travel (after earning $300 travel credit) and dining, 10x points on Lyft rides. | $550 |

| Chase Ink Business Preferred | 3x points on travel, shipping, internet, cable, phone services, and advertising (up to $150,000 per year). | $95 |

Once you have a premium card, you can mix and match other Chase credit cards to suit your needs. Here’s a list of some of the options:

| Card Name | Bonus Categories | Annual Fee |

| Chase Freedom Flex | Rotating quarterly bonus categories, plus earning 5 points for every dollar spent on travel purchased through Chase Ultimate Rewards, 3 points per dollar spent at restaurants, and 3 points per dollar spent at drugstores. | $0 |

| Chase Freedom Unlimited | Unlimited 1.5 points per dollar spent on all purchases. | $0 |

| Chase Ink Business Cash | Earn 5x points on the initial $25,000 spent at office supply stores and on internet, cable and phone services annually. Get 2x points for the first $25,000 spent at gas stations and restaurants each year. | $0 |

| Chase Ink Business Unlimited | Unlimited 1.5 points per dollar spent on all purchases. | $0 |

What About the Chase Quadfecta?

The appeal of Chase’s credit card lineup lies in the ability to add as many cards as desired, subject to the credit limit Chase is willing to extend. With more cards added to your wallet, a wider array of bonus spending categories becomes available, along with more opportunities to earn signup bonuses.

In my case, I have five Chase credit cards that I use in my own tailored strategy, which includes a combination of both business and personal cards. Continuing with the horse racing theme, this could be termed a pentafecta, while a combination of four cards would be a superfecta.

One notable benefit of Chase is combining Chase Ultimate Rewards points with another person in the same household. This allows couples holding cards earning Chase Ultimate Rewards to pool their points together. Consequently, only one household member needs a premium card, helping to save on annual fees and creating additional opportunities for welcome bonuses.

What Can You Do With Chase Ultimate Rewards?

One of the best aspects of the Chase Trifecta is that it can help you unlock a world of travel rewards, allowing you to explore new destinations and experiences for less.

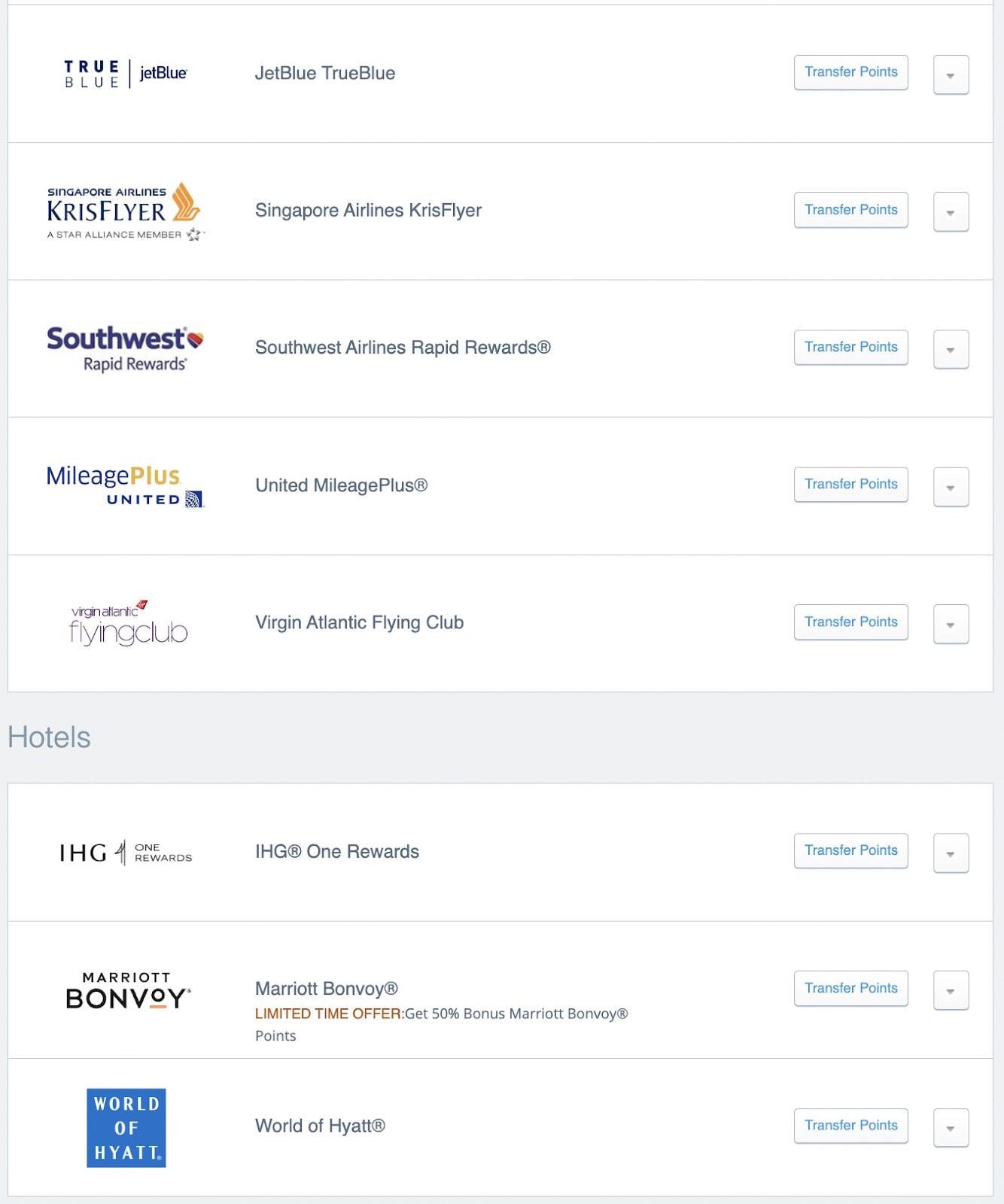

With the rewards points you earn through your Chase credit cards, you can book flights, hotels, rental cars, and more through the Chase travel portal, or you can transfer your points to Chase’s airline and hotel partners.

Using your points to book travel through the Chase travel portal can often be a good way to get value for your rewards since you can redeem your points at a higher rate when you book through Chase.

For example, if you have the Chase Sapphire Preferred, your rewards points are worth 1.25 cents each when redeemed for travel through Chase. With the Chase Sapphire Reserve, your points are worth 1.5 cents each.

If you want to maximize the value of your Chase Ultimate Rewards points, one great option is to transfer your points to Chase’s hotel partners, such as Hyatt.

Hyatt is a popular choice thanks to its extensive network of luxury properties worldwide and generous loyalty program.

When you transfer your Chase Ultimate Rewards points to Hyatt, you can redeem them for free stays at some of the world’s most luxurious hotels and resorts, often at a much lower rate than you would pay if you booked directly through Hyatt or another travel provider.

As a personal example, I just booked two rooms for a six-night stay at the Andaz Costa Rica Resort at Peninsula, a five-star resort in peak season, which would cost over $12,000 paying cash for a total of 23,000 points per room per night (a total of 276,00 Chase Ultimate Rewards points).

This means that I could utilize my Chase Ultimate Rewards points at a value of 4.34 cents per point. Furthermore, the 5 points per dollar I earned on my Chase Freedom Flex spending had a value that was 4.34 times their actual value, meaning that I was actually getting over 21% back in value on purchases made within that quarter’s bonus categories.

Earning 276,000 points can take some time and effort. In my case, these points were earned through a combination of a limited-time 90,000 bonus offer on the Chase Business Ink Preferred card, as well as spending in bonus categories on both personal and business cards, where my expenses are higher than the average household. In other words, earning that many points within a year for a beginner with low to average household expenses would be difficult.

Chase Trifecta FAQs

When choosing the right Chase Trifecta cards for you, consider your spending habits and financial goals. Look at each card’s bonus categories and compare them to your spending patterns. For instance, the Chase Sapphire Reserve’s 3x points on dining may be a good fit if you eat out frequently. Also, envision how you plan to use the card. The Sapphire Preferred can make more sense if you want to minimize the annual fee and just take advantage of transferring to partners. In contrast, the Sapphire Reserve can make up for the annual fee with the $300 travel credit and the ability to redeem at 1.5 versus 1.25 if you want to redeem for travel through the portal.

While there are several other popular Chase credit cards to consider, it’s important to note that Chase will only extend you so much credit, so it’s best to get the Chase Trifecta in place first before considering these cards. Some other popular Chase cards to consider include the United Explorer Card and the Marriott Bonvoy Boundless Credit Card, both of which offer exclusive perks and rewards points for travel. These earn points directly with the specific airline or hotel instead of through Chase.

The Chase Freedom card has been retired and replaced by the Chase Freedom Flex card. This means that new applicants can only apply for the Chase Freedom Flex. The new card offers similar bonus categories to the original card, including 5% cash-back on rotating quarterly bonus categories and a range of other benefits, such as 3% cash-back on dining and drugstore purchases, 5% cash-back on travel booked through the Chase Ultimate Rewards portal, and more.

Start Earning More Travel Rewards Today With the Chase Trifecta

Chase Trifecta is an effective credit card strategy for maximizing rewards and achieving travel goals.

By leveraging Chase’s Ultimate Rewards program, individuals can earn bonus points and cash-back on various spending categories. Additionally, combining personal and business credit cards, pooling points with household members, and earning sign-up bonuses can help maximize rewards even further.